Participants in the renewable energy industry should be aware of antitrust and competition rules because renewable energy is no longer a nascent field. In 2025, the United States is projected to generate 25% of its electricity from renewable sources,1 slightly ahead of projections that the EU will generate 24.5% of its electricity from renewables.2 The International Energy Agency projects that the ”massive global growth of renewables” will result in these sources meeting 50% of global demand by 2030.3 With the industry’s increasing size and success, antitrust issues are likely to multiply. As just one example of the antitrust issues that dealmakers face, a total deal value of $126.4 million—no longer unusual in this space—will trigger a mandatory “HSR” merger control filing in the U.S. (unless a deal is otherwise exempt), and many non-U.S. jurisdictions have similar merger control regimes and thresholds. Industry participants therefore need to learn the rules, and be prepared.

While renewable energy business practices and transactions have many similarities to those of traditional energy sources, there are some key differences both in the nature of the business activity and the mix of investors. And since the growth of renewables has attracted many new sources of capital, including direct investing from public pensions, fixed income investors, and non-U.S. funds, participants may not be familiar with the antitrust rules of the road in the energy space. This article serves as a primer.

Our goal in this article is to provide a quick survey of antitrust issues faced by renewable energy companies, involving both deal and non-deal conduct. Since the issues are extremely varied and are not necessarily interrelated, this article presents them as a list, grouped first into issues involving transactions, and second into issues involving non-deal conduct. While we cover many of the most common issues, a primer such as this is not intended to address all of the nuanced issues renewable investors may face from antitrust authorities or in the courts. We encourage industry participants to seek qualified antitrust counsel.

HSR Act and Transactional Antitrust Issues for Renewable Energy

What Merger/Deal Harm Do Authorities Seek To Prevent?

HSR Act Filings and the “Merger Control” Process

“Merger Control” Traps: Issues That Can Cause An Unexpected HSR Act Filing

“Clean Teams” and “Gun Jumping”

Key HSR Act Exemptions

Swaps of Assets, Generation, and Transmission Capacity

Interlocking directorate

FERC, ERCOT, and Other Regulatory and Organizations’ Review

What about CFIUS?

Conduct-Related Antitrust Issues for Renewable Energy

The Basics: Sherman Act Section 1 and Section 2

Per se infractions

Information Sharing

Trade Associations

Swaps for Hedging

Buyer or Seller Cooperatives

Government Interaction Immunity: Noerr-Pennington and Parker

“Filed Rate Doctrine” Immunity and FERC Rates

Blockchain as an Information Sharing Risk

DOJ and FTC Business Reviews

Conclusion

HSR Act and Transactional Antitrust Issues for Renewable Energy

What Merger/Deal Harm Do Authorities Seek To Prevent?

Most deals are not challenged under the antitrust laws. For deals filed under the antitrust merger notification laws (discussed in the next section), fewer than 3% of all deals and 4% of energy deals receive a formal antitrust investigation, and only about half that number are blocked or subjected to substantial remedies, such as divestitures. Nevertheless, a renewables dealmaker should consider whether the deal will be cleared quickly or whether it might face a long antitrust investigation. To assess harm, authorities in the United States use the Merger Guidelines,4 which focus on how much a deal increases concentration in a properly defined market, and whether there exists “merger specific harm.” “Harm” in this context means negative impact on price, quantity, or quality, and “merger specific” means caused by the merger, and only by the merger. Harm that already exists before the merger, or would happen regardless of the merger, is not merger specific and is not properly the subject of merger investigations. Typically, the FTC and DOJ enforcers as a rule do not use merger review as an opportunity to hold up dealmakers in service of political or industrial policy goals—they pride themselves on addressing economic harm, alone.

The agencies’ guidelines explain that a properly defined market (sometimes referred to as an “antitrust market” for these purposes) has both a “product” and “geographic” component, meaning what a company sells (or buys) and over what distance it is able to sell it. Less well known is that the “product” market can be narrowed substantially by the preference of customers, a factor that may be highly important to the renewables industry. For example, situations may exist where customers have a specific demand for renewable energy, in which case those customers will not consider fossil fuel energy to be an acceptable substitute even though at a physics level the electrons in the transmission line are indistinguishable. In this case, a market may be defined as narrowly as “green energy,” meaning that an authority could assert harm from a renewables merger even though plenty of competition from fossil fuel energy exists. To avoid being surprised by narrow market definitions that could increase the chances of a long merger investigation, renewables investors should consider carefully any unique customer preferences that may apply.

More broadly, antitrust authorities most commonly assert three categories of harm: unilateral price effects (ability of the merged entity to raise price by itself); coordinated price effects (ability of the merged entity to raise price in concert or in parallel with rivals, due to a reduction in overall marketplace competition as the result of the merger); and vertical foreclosure (ability of the merged firm to burden or exclude rivals, to the ultimate detriment of customers, because rivals no longer have access to key products or services that the merged firm will control). In addition, the tendency of a merger to eliminate a “maverick”—a company that is disruptive as to price or technology—can be a particularly damning allegation. Since renewable energy often involves innovators and mavericks, dealmakers should be keen to demonstrate that a merger will improve, not curb, the competitive spirit of the businesses involved.

The potential for harm can be mitigated, and sometimes eliminated, by the presence of long-term contracts that lock in favorable prices and other terms for customers. Thus, the antitrust risk profiles may differ sharply between, on the one hand, a renewables facility that has a dedicated offtaker at a fixed price for a substantial majority of the project’s expected life, and on the other hand, a facility that is subject to merchant risk.

HSR Act Filings and the “Merger Control” Process

In much of the world, including the United States and Europe, mergers, acquisitions, joint ventures and other business combinations above a certain size are subject to merger control regimes in which an antitrust authority must review the deal before it can close. In the United States, the main merger control laws are Section 7 of the Clayton Act5 and the Hart-Scott-Rodino Antitrust Improvements Act (HSR Act),6 which, together with their implementing regulations,7 require most deals above $126.4 million in value to be notified to the Federal Trade Commission (FTC) and the Department of Justice’s Antitrust Division (DOJ), and to undergo a 30-day waiting period before a deal can close8 (unless a deal is otherwise exempt, as we discuss below). The $126.4 million threshold, as well as several other thresholds that apply to fees and other aspects of the HSR Act process, adjusts annually based on the size of the U.S. economy.9 The European Union (EU), Canada, Mexico, the UK, and many other jurisdictions also require notification for deals above specified value, sales, or other thresholds. Each jurisdiction applies substantial “gun jumping” fines for companies that close a deal without notification and clearance, or that prematurely integrate their businesses before obtaining clearance. As a result, renewables dealmakers should consult antitrust counsel as a regular part of their legal preparations.

In addition to the $126.4 million value threshold, a transaction of between $126.4 million and up to $505.8 million must be above the “size of person” threshold before it must be reported under the HSR Act.10 The size of person test is satisfied when one party (including any entities it controls) has annual net sales or total assets of $252.9 million or more and the other party has annual net sales or total assets of $25.3 million or more. Transactions valued at more than $505.8 million are reportable regardless of the size of person test. (Again, these thresholds adjust annually.) Early-stage businesses and recently formed investment funds may be below such thresholds, so always check whether a size of person issue exists when evaluating reportability.

Note that both the FTC and the DOJ have investigators who make energy transactions in general, and sometimes renewables transactions in particular, a key part of their work. At the FTC, these investigators are in the Mergers 2 division (which also handles coal) and Mergers 3 division (which also handles oil and gas). At the DOJ, these investigators are in the Transportation, Energy and Agriculture section and the Networks and Technology section, which handle what their names imply. The FTC and DOJ share authority over renewable energy.

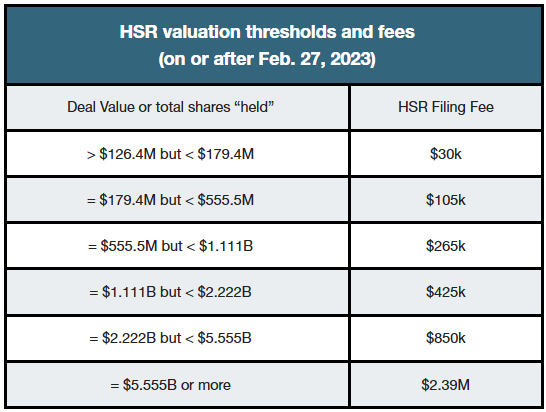

For 2025, the HSR Act value thresholds and filing fees are shown in the table below.

“Merger Control” Traps: Issues That Can Cause An Unexpected HSR Act Filing

There are several HSR Act traps that can require a filing where parties might not expect it. Five common ones that arise in the renewables context (although they are not unique to renewables) are joint venture (JV) and non-corporate changes in control; the treatment of shares “held” as the result of a transaction involving incremental acquisitions; multiple assets purchased over time from the same seller; the assumption or payoff of debt; and purchase price adjustments. It is often wise, therefore, for contracts involving such rights to address the potential for an HSR filing.

Non-corporate entity control, including for JVs, is defined under the HSR rules to exist when a party possesses 50% (not 51% or more) of economic rights, as measured by the right to profits during operation or the right to assets upon dissolution, in addition to certain other tests.11 “Non-corporate” entities are defined as anything other than a corporation. General partnerships, limited partnerships, and limited liability companies (LLCs), all of which are common JV forms, are treated as non-corporate entities under the rules. Renewables investors using such business forms may find that two (or sometimes more than two) separate investors may be deemed to “control” a JV, and thus may have a filing when a JV is formed (assuming that value thresholds are exceeded). Even more confusing, a small increase in economic rights during the operation of a JV—for example, from a 49% to a 50% interest—can thrust a JV partner into a new “control” position under the rules, and can, under some scenarios, trigger a filing obligation where none was required before.

The “held” and “incremental acquisition” issues refer to the fact that the HSR rules judge deal value by all shares and other interests in the counterparty that are owned or controlled upon close of the deal, not merely by the value acquired in the most recent transaction. If a party acquires shares incrementally over time, then even a small incremental acquisition may put that party over an HSR Act threshold and require a filing. For example, if investor Party A wishes to acquire $2 million in shares of a power company Party B, but already owns $125 million in shares of Party B, then the combination of newly acquired and previously acquired shares would exceed $126.4 million, and the parties must make an HSR Act filing.12 In the FTC’s description, the relevant number for purposes of the filing threshold is “the value of all the shares held by the Acquiring Person, not just the incremental shares most recently purchased.”13

Acquisition of multiple assets from the same person over a 180-day period (or the signing of an agreement to do so) may trigger a filing even though each asset individually would be below the HSR Act thresholds if considered on its own. The FTC has a helpful page on when and how to aggregate acquisitions.14 But note that acquisitions of goods or realty that are transferred in the ordinary course of business are not covered by this rule, since they are exempted by statute.15 Serial acquisition of wind turbines by an energy producer probably would qualify as ordinary-course purchasing, but an acquisition of a separate, currently operating wind farm probably would not.

Assumption of debt must be included in the calculation to determine if the value of the deal exceeds the HSR Act thresholds in some types of transactions, particularly those involving asset acquisitions.16 A detailed summary of the nuances within the assumptions of debt rules is beyond the scope of this article, but if liabilities are being assumed, consult counsel about whether they should be included in the valuation.

Purchase price adjustments are common features of some renewables deals, especially in situations where the economic prospects of a project are difficult to value. If a transaction involves significant post-closing adjustments, milestones, earnouts, or other contingent payments, the valuation of a transaction is likely to be designated under the HSR rules as “not determined,” in which case the acquiring party must make a formal fair market valuation (FMV) to determine the total value of interests that are to be acquired or held.17 This may cause a deal that appears to be “nonreportable” (meaning, not subject to an HSR filing), if measured only by its up-front price, to instead require reporting based on the additional value of the adjustments. This also may cause an already-reportable deal to be in a higher-than-expected category of HSR threshold, and thus require a higher HSR filing fee.

“Clean Teams” and “Gun Jumping”

If a transaction is HSR-reportable, it is unlawful for the parties to close the deal or transfer de facto control to the buyer before the waiting period has expired or the authorities have otherwise signaled their intention to take no further action (known as receiving HSR clearance). Closing or establishing control before clearance is known as “gun jumping” (jumping the gun on the waiting period), and is subject to substantial fines even where a deal has no competition problems. The parties are not permitted to begin integrating their business during the waiting period; however, they may plan for such integration, even to the point, if certain precautions are observed, of discussing the deal with customers.

The FTC has provided guidance on avoiding gun jumping.18 One element of the FTC’s recommendations is that, if the transacting parties do or may compete, they should establish some form of “clean team” procedure to avoid the unnecessary sharing of competitive sensitive information, the possession of which could lead to a de facto transfer of control or otherwise disrupt the ordinary course of the parties’ competition. According to the FTC, “[c]lean teams should not include any personnel responsible for competitive planning, pricing, or strategy.”19 Not every deal will require a clean team, but it is a good practice to consult counsel about the need for a clean team whenever competitively sensitive information may be in play during deal evaluation, due diligence, or integration planning.

Key HSR Act Exemptions

While renewables transactions are increasingly subject to merger control filings due to their size, industry participants should know that multiple exemptions exist that may prevent the need for a filing. The following general HSR filing exemptions have proven to be particularly common in renewable energy transactions.20

The “new facilities” rule,21 sometimes called the “greenfield” rule, exempts acquisition of a “new facility,” meaning a structure that has not produced income and was either constructed by the seller for sale or held at all times by the seller solely for resale. The new facility may include realty, equipment, or other assets incidental to the ownership of the new facility. For a renewable energy facility, these other assets may include permits, power take-off contracts, and other ordinary-course items.22 Note that this and other exemptions essentially trump the “traps” mentioned above in that they apply regardless of the size and number of transactions. For example, a common renewables transaction structure is that a private equity fund buys operating assets and gets exclusivity to buy a developer’s pipeline of new facilities under development, with the purchase of those facilities happening at mechanical completion. The purchase of an operating facility would trigger an HSR Act filing if its value exceeds $126.4 million, but the subsequent purchases of new facilities would be exempt, regardless of the size of those purchases and regardless of the fact that the transactions otherwise would have been subjected to the aggregation rules discussed above.

The “used facilities” rule23 exempts an acquisition if the facility is acquired from a lessor that has held title to the facility for financing purposes in the ordinary course of the lessor’s business, by a lessee that has had sole and continuous possession and use of the facility since it was first built as a new facility. Again, the used facility may include realty, equipment or other assets associated with the operation of the facility.

The “unproductive real property” rule24 exempts acquisition of real property, including raw land, structures or other improvements (but excluding some types of equipment), natural resources and assets incidental to the ownership of the real property, that has not generated total revenues in excess of $5 million during the thirty-six (36) months preceding the acquisition.

The “look through to assets” rule25 allows an acquirer to “look through” a corporate or non-corporate form, and exempts the acquisition of an entity if acquisition of the entity’s assets, instead of the entity itself, would have been exempt. For example, if an acquisition target holds a new solar power project that qualifies for the “new facilities” exemption discussed above (and the target entity does not otherwise hold non-exempt assets with a fair market value in excess of the HSR transaction size threshold), then the acquisition of the target entity would not require a filing under the HSR Act.

Acquisitions of minority interests in partnerships and LLCs are exempt from HSR Act requirements.26 This is useful for renewable energy, where assets often are held in non-corporate entities, such as partnerships or LLCs. The HSR filing requirements only apply to acquisitions of partnership interests and LLC membership interests if the acquiring person obtains 50% or more of the interests, and the interests held by the acquiring person exceed the current transaction size threshold.

The restructuring rule27 applies when an acquisition of non-corporate interests or voting securities occurs only as a result of the conversion of a corporation or unincorporated entity into a new entity, or as a result of a stock split or other restructuring of ownership. If no new assets will be contributed to the new entity as a result of the conversion, and either (a) as a result of the transaction, the acquiring person does not increase its percentage of holdings in the new entity relative to its percentage of holdings in the original entity, or (b) the acquiring person already controlled the original entity, then the restructuring is exempt. Thus, for example, there would be no HSR filing where a solar energy firm converts from an LLC to a C-corporation (a so-called “Up-C” transaction) and goes public, if this causes the LLC’s owners to take shares in the C-corporation that are in the same proportion (or lesser) as their interests in the LLC.

The institutional investor rule28 states that acquisition of shares is exempt if made directly by an institutional investor, in the ordinary course of business, solely for the purpose of investment, and as a result of the acquisition, the investor would hold 15% or less of the outstanding voting securities of the issuer. “Institutional investor” is a defined term that includes many common investors in renewables, such as banks, finance companies, and pension trusts.

The financing rule29 provides that an acquisition of non-corporate interests that confers technical control of a new or existing unincorporated entity is exempt if the acquiring person is contributing only cash to the unincorporated entity, for the purpose of providing financing, and the terms of the financing agreement are such that the acquiring person will no longer control the entity after it realizes its preferred return. It is common in the renewables industry for control of a project to begin in the hands of a financing institution but then “flip” to an operator, after a specified return for the financing institution is reached. These generally can be designed lawfully, so that there is no HSR filing for the financing institution.

Swaps of Assets, Generation, and Transmission Capacity

The most common form of swaps in renewables transactions is probably a swap used as a hedge, whether of generation capacity or transmission capacity. Such transactions are used to lock in rates, providing some protection against fluctuation of prices in the energy markets. These are generally exempt from HSR Act filing because they qualify as pure financial instruments or ordinary course transactions subject to merger control exemptions (see discussion above). Swaps of title to land, permits, and operable assets, however, should be assumed to be non-exempt, unless further discussed with counsel.

Asset swaps may occur, for example, if real estate acquisitions result in a “jigsaw puzzle” patchwork of sites and renewable energy capacity that is not efficient. A solution to such a “puzzle” is for Party A and Party B to trade to each other, on a permanent basis, certain “puzzle pieces” to consolidate their portfolios and make a more efficient whole. Asset swaps also help conserve cash and may have tax benefits. The fact that no money changes hands does not exempt them from HSR coverage: the HSR Act and its non-U.S. equivalents apply to asset acquisitions of any kind, not just cash sales, and they usually judge value by any means of exchange. When assets are swapped for assets (or shares for shares, shares for assets, or any combination thereof), value is exchanged and the deal must be evaluated under the HSR Act rules. Since a cash price does not change hands, an asset swap likely will be treated under the rules as having a “not determined” price, in which case each side (because each is an acquiring party of the other’s assets) must perform an FMV calculation to assess whether its asset acquisition triggers an HSR filing.

Interlocking directorates

Interlocking directorates occur when the same person is an officer or serves on the board of directors for two different corporations that compete. When the “person” is a business entity, that entity is said to be in an interlocked position if it has an officer or director at two competing corporations, even if the representatives are separate persons. For example, if an investment partnership has Partner A on Corporation X’s board, and Partner B on Corporation Y’s board, and X and Y compete, then an interlock exists. Under Section 8 of the Clayton Act,30 interlocking directorates are prohibited unless the parties can show that their competitive sales are de minimis by one of several measures, such as that the competitive sales of either corporation are less than $5,138,000 (as adjusted annually).31 There is no reasonableness or balancing test in this rule: if the interlock exists and none of the de minimis points can be asserted in the parties’ favor, the prohibition automatically applies, and the interlocking personnel must vacate their positions in one of the corporations. In situations where the interlock is thrust upon a person, that person has one year in which to vacate. Note that this rule only applies, however, to interlocks at the director or officer level. A person or entity can still own and vote shares in both corporations—this law does not require divestiture of ownership interests. To challenge mere ownership, antitrust authorities would need to file a lawsuit under the general antitrust laws and prove likelihood of harm, a more daunting proposition than invoking the automatic prohibition of Section 8.

By its terms, the interlock statute applies only to corporations. Its application to other business forms, such as partnerships and LLCs, has not been fully tested in the agencies or the courts. The FTC under President Biden took the position that interlocks by non-corporate entities should be subject to the same requirements, under the general rules against unfair competition established by Section 5 of the Federal Trade Commission Act.32 The FTC’s position under President Trump has not been clarified as of mid-2025.

FERC, ERCOT, and Other Regulatory and Organizations’ Review

Other industry regulators and organizations also may perform reviews that are based, in part, on the competitive impacts of a transaction. These primarily include reviews by the Federal Energy Regulatory Commission (FERC) and the Public Utility Commission of Texas (PUCT), which have authority over competitive wholesale electricity markets. Others such as the Electric Reliability Council of Texas (ERCOT), PJM Interconnection and other regional transmission organizations (RTOs), and the California Independent System Operator (California ISO) and other ISOs have input into competitive dynamics in many different ways. Requirements by federal and state regulators, if they are specific and mandatory, can trump the more general requirements of the antitrust laws (see discussion below of the Noerr-Pennington and Parker antitrust immunities) but directives by localities and private organizations do not. The antitrust authorities closely coordinate with all such government and private bodies and will take into consideration their views on competitive impacts; however, the antitrust authorities ultimately make their own separate conclusions, and have been known to disagree with industry bodies.

What about CFIUS?

The Committee on Foreign Investment in the United States (CFIUS) is an interagency committee authorized to review certain transactions involving foreign investment in the United States for national security concerns. When CFIUS identifies such concerns, it can take action to mitigate the risk to U.S. national security or recommend to the President of the United States that the transaction be blocked or unwound. While the CFIUS process is separate from the antitrust process, it has some similarities to antitrust merger control, including a notification system, filing fee (for some filings), and specified timelines for review. Like the HSR process, the CFIUS process is confidential unless the parties choose to disclose it. A CFIUS filing is mandatory for some deals and voluntary for others. (The option for a voluntary filing is a difference from the HSR process. There is no voluntary filing option for HSR.)

CFIUS has jurisdiction to review any transaction that could result in control, direct or indirect, of a U.S. business by a foreign person. It has jurisdiction to review certain non-controlling investments by foreign persons in U.S. businesses engaged in activities involving critical technologies, critical infrastructure, or sensitive personal data (called “TID U.S. businesses”). CFIUS also has jurisdiction to review transactions based on the proximity of real estate to certain military facilities.

Of note for the renewable energy sector, “critical infrastructure” activities include, inter alia, owning or operating (1) facilities for the generation, transmission, distribution, or storage of electric energy comprising the bulk-power system; (2) any electric storage resource physically connected to the bulk-power system; or (3) any facility that provides electric power generation, transmission, distribution, or storage directly to or located on certain military installations. Given the often rural or ex-urban location of both renewable energy sites and military facilities, proximity to military facilities is often a key CFIUS consideration in renewable energy investments.

Renewables investors should note that private equity and investment groups increasingly include international members; for example, pension funds of several governments are active investors in renewable energy. Thus, CFIUS issues commonly arise in this space. If an investor or JV partner has foreign persons anywhere in its ownership structure, parties are well advised to consult CFIUS counsel for a review of whether a CFIUS filing should be made.

Additionally, Australia, the UK, the EU, and many other jurisdictions increasingly have foreign investment review regimes similar to CFIUS; the rules vary widely.

Conduct-Related Antitrust Issues for Renewable Energy

The Basics: Sherman Act Section 1 and Section 2

The principal federal antitrust statute governing non-merger conduct is the Sherman Act, which covers conduct involving non-merger agreements33 (Section 1) and a single firm acting alone34 (Section 2). Except in the case of per se (automatic) infractions, which are discussed below, both sections use reasonableness tests, although the tests differ.

The reasonableness test under Section 1 is called the “rule of reason.” It has several well defined steps, usually identified as: the plaintiff must show an agreement between the defendants; the defendants must have “market power” in a well-defined market; the agreement must create a restraint that tends to have anticompetitive impact in the market; if such a restraint exists, the burden shifts to the defendants to show that the restraint is reasonably related (some courts say, reasonably necessary) to achieving a legitimate business justification; and if the justification exists, the burden shifts back to the plaintiff to show that the justification is mere pretext, or otherwise that, on balance, the conduct is unreasonable. In practice, a tie generally goes to the defense.

The reasonableness test under Section 2 is less well defined (in fact, it is the subject of much legal and academic debate) but one of the most common formulations is the “no economic sense” test: a plaintiff must show that the conduct of a defendant single firm harms competition as a whole, and the conduct must make no economic sense to the defendant, except for its tendency to benefit the defendant by reducing competition. DOJ has stated this test as: a plaintiff must demonstrate that an alleged monopolist sacrificed short-term profits solely because of its anticompetitive, exclusionary effect. Generally, Section 2 offenses must involve exclusionary conduct, meaning the tendency to exclude competitors from a market (either entirely, or from expanding) and thus allow the defendant to raise price or reduce quantity or quality of goods and services, in the long run.

“Monopoly power” and “antitrust harm” are key concepts, necessary for almost all antitrust claims. Monopoly power is a fact-dependent inquiry. It measures the presence—usually, via annual sales—of all firms to the relevant agreement under Section 1, or of the single firm acting alone under Section 2. Courts often find that a market share over 70%, if combined with significant barriers to entry, establishes a prima facie case of monopoly power. Courts rarely conclude that monopoly power exists where the market share is less than 50%. Antitrust harm means harm that is caused directly by anticompetitive conduct, and that would not exist otherwise; antitrust law is generally careful not to mistake hard bargaining and rough-and-tumble competition for anticompetitive acts. A famous maxim is that antitrust laws are for “the protection of competition, not competitors”;35 a plaintiff must show injury not only to itself, but also to competition as a whole.

Plaintiffs who prove violations of the Sherman Act, whether civil or criminal, may obtain treble damages and attorneys fees. Criminal violations of the Sherman Act also may be punished by monetary fines of up to $100 million for corporations (or twice the gross gain or loss, if there is a larger impact on U.S. commerce), up to $1 million for individuals, and up to 10 years imprisonment for individuals.

Per se infractions

Certain types of agreements between competitors are considered to be per se (automatic) violations of antitrust law and are deemed illegal immediately—without any opportunity to justify them under the reasonableness tests discussed above—once the conduct has been established. This is not a comprehensive list but examples include:

Price fixing is an agreement between competitors to raise, fix, hold firm, establish minimums, or any other activity to otherwise maintain their prices. Price fixing agreements can include limits on supply to increase price, eliminating or reducing discounts, and fixing credit terms.

Bid rigging occurs where an entity (such as a local government) has solicited competing bids, but competitors have agreed in advance who will win the bid or upon a means of determining who will win the bid.

Market allocation occurs where competitors divide markets among themselves, which can take the form of allocating geographic locations, customers, types of products, or the like.

Boycotts occur when two or more competitors agree to exclude a third competitior, for reasons unrelated to efficiency. When a boycott is motivated by anticompetitive goals, it is automatically illegal.

When combined with concealment or other indicia of cartel intent or guilty mind, the first three of these—price fixing, bid rigging, and market allocation—may be prosecuted criminally. Boycotts generally are not prosecuted criminally but can lead to significant civil damage claims.

Information Sharing

It is natural for renewables companies to share information on best practices, technology, and many other topics. Antitrust authorities, however, express concern regarding the sharing of “competitively sensitive information” (CSI). CSI is any information of Competitor A that is not public or well-known, which, if learned by Competitor B, could increase the ability of A or B to anticipate the price, quality, or quantity/production strategy of each other, particularly if it would make them more likely to engage in parallel conduct or otherwise reduce the intensity of their competition (e.g., compete less vigorously on price). The FTC and DOJ historically have recognized a “safety zone” for the sharing of CSI. The agencies recently withdrew these policy statements,36 but they remain consistent with enforcement precedent. Accordingly, antitrust risk related to the sharing of CSI likely is diminished if:

- the exchange is managed by a third party, such as a trade association;

- the information provided by participants is more than three months old; and

- at least five participants provide the data underlying each statistic shared, no single provider’s data contributes more than 25% of the “weight” of any statistic shared, and the shared statistics are sufficiently aggregated that no participant can discern the data of any other participant.37

An exchange of information that falls outside the safety zone may still be lawful but, in the FTC’s view, “only if, taking account of likely anticompetitive effects and any procompetitive justifications, the exchange promotes competition.”38

Since most exchanges of CSI likely are not as formal as this safety zone would require, exchanging companies should document their justifications and limit sharing to persons who have a reasonable need for the information. The authorities look more favorably upon exchanges if sharing is limited to non-operational personnel (e.g., not sales managers who directly compete with each other) and is supervised by antitrust counsel.

Trade Associations

Trade associations provide many important and procompetitive functions for renewables but when working within trade associations, renewables firms are likely to face the information sharing issues discussed immediately above, and the government petitioning issues discussed below. In addition, when trade association meetings bring competitors together in the same room—as they often do—there is a possibility of explicit or tacit collusion. To prevent misconduct or (almost as importantly) the appearance thereof, some practices to observe are: ask each trade association to establish a written antitrust policy (even a short one is better than none at all); create agendas that are reviewed by counsel beforehand, and to stick to the agendas; and avoid discussion of competitively sensitive information as to price (including costs), quality, and quantity of members’ input. A company’s attendees should review standards of appropriate conduct before attending a trade association meeting and, if any questionable behavior takes place in their presence, should report back immediately to the company’s counsel for follow up action.

Swaps for Hedging

A hedging swap involves exchanging a floating market price for a fixed price over a specified time period, so that one of the parties locks in a particular price and the other bears the risks and rewards of volatility. Electricity customers use swaps to lock in their energy costs, while producers use swaps to lock in their cash flow. Swaps are very common in the electricity industry, including involving renewables, and generally they are considered to be efficiency-enhancing or at least benign. Antitrust problems may arise, however, if a network of swaps allows competing producers (or in theory, competing customers) to learn of and coordinate or parallel each other’s pricing. The DOJ brought a lawsuit on this misuse-of-swaps theory in 2010 involving traditional electricity generation39 and competition authorities have expressed interest in policing the renewable energy space as well.

Buyer or Seller Cooperatives

Buyer and seller cooperatives have a long history in the energy industry. They can confer a number of benefits, such as reducing transaction costs in marketing and contracting. By increasing scale, a cooperative can help its members smooth out peaks and dips in production and demand cycles, a boon in particular for solar and wind firms whose production may vary rapidly according to weather. Antitrust authorities recognize these benefits but also identify some antitrust risks, and have issued guidance, including safe harbors.

If a buyer cooperative (also known as a group purchasing organization) “provide[s] some integration of purchasing functions to achieve efficiencies,”40 and cannot collectively exercise market power, it is likely to be seen as lawful. Antitrust authorities have established a share-based safe harbor: absent extraordinary circumstances, they will not challenge such a buyer cooperative where (1) purchases account for less than 35% of the total sales of the purchased product or service in the relevant market, and (2) the cost of the products and services purchased jointly accounts for less than 20% of the total revenues from all products or services sold by each competing participant in the joint purchasing arrangement.41 Buyer cooperatives that exceed these thresholds are not automatically illegal, so long as they provide the “integration of purchasing functions” mentioned above; however, automatic illegality may apply if those features are absent and the cooperative appears to be a mere “buyer cartel” involving a “naked” agreement on purchasing prices. The FTC and DOJ have stated that “[a]n agreement among purchasers that simply fixes the price that each purchaser will pay or offer to pay for a product or service is not a legitimate joint purchasing arrangement and is a per se [automatic] antitrust violation.”42

Seller cooperatives must follow similar rules to those of buyer cooperatives but the market share thresholds are not as generous as those for buyers. For many years, a safe harbor existed: absent extraordinary circumstances, the authorities would not challenge a seller cooperative when the market shares of the cooperative and its participants collectively account for no more than 20% of each relevant market in which competition may be affected.43 This safe harbor did not apply to agreements “that are per se illegal, or that would be challenged without a detailed market analysis” (for example, if sellers were to conceal aspects of their collaboration in cartel fashion), or to competitor collaborations to which a merger analysis is applied.44 The Biden Administration antitrust enforcers withdrew this guidance one month before the Trump Administration began, over the dissents of the two Republican FTC Commissioners at the time.45 Trump Administration enforcers subsequently suggested that they would not formally reinstate the guidance but would generally follow it as if it had not been withdrawn.

Government Interaction Immunity: Noerr-Pennington and Parker

Renewables firms often seek government action to remove barriers to green energy production or to actively promote the industry. Land use permits, transmission permits, payments in lieu of taxes (PILOTS), and tax credits are a few examples. Two types of antitrust immunity may apply to requests for government action. Both are very powerful immunities because they are based in the First Amendment to the U.S. Constitution. They are also very narrow: a company must stay within their bounds to receive protection.

Noerr-Pennington petitioning immunity46 provides protection from antitrust lawsuits for parties who petition a government for benefits. The petitioned-to governments may be federal, state, or local, and the benefits may be in the form of laws, regulations, or even direct payments. If anticompetitive effects result from the government action, but those effects are caused solely by the government action itself, then the private petitioners cannot be held responsible for those effects. Collaboration between private firms that is a necessary part of the petitioning is likewise immune. Thus, a joint lobbying effort by wind power producers to open federal land for construction of turbines, or even to raise regulated power tariffs, would be immune. But those same wind power producers would not be protected if they use their meetings to fix prices privately, independently of the government action.

Parker state action immunity47 applies to federal and state governments and their officials when they exercise legislatively-granted authority. It also applies to private entities acting at the clear direction and under “active supervision” of a federal or state government; this can, for example, apply to a state board for the establishment of solar energy standards, which is a state entity but is partially or completely composed of private industry employees. No such immunity applies if private actors use the pretense of state direction but are not actively supervised by federal or state actors. “Active supervision” has proven difficult to define in the abstract and is the subject of much recent controversy involving state regulatory boards. Private persons wishing to invoke state action immunity are advised to seek assessment by qualified antitrust counsel. Note: state action immunity cannot be conferred by local and municipal governments, unless those governments too are clearly acting at the direction of their state.

“Filed Rate Doctrine” Immunity and FERC Rates

The “filed rate doctrine” is an immunity rule, created by the U.S. Supreme Court, that bars recovery of antitrust damages based on a claim that rates are unlawful, if those rates are validly filed with, and not disapproved by, a regulatory agency with appropriate jurisdiction. The doctrine was announced originally in the context of railroad shipping rates but has been applied equally to energy rates filed with the Federal Energy Regulatory Commission and other agencies.48 This immunity does not prevent damages based on claims that producers engaged in price fixing cartels or other price manipulation, or for refusal to supply, and it does not prevent a plaintiff from petitioning the relevant agency to alter the rates. The doctrine merely prevents damages based on the allegation that the rates, by themselves, are unlawful or anticompetitively high.

Blockchain as an Information Sharing Risk

Blockchain technology has applications in the renewable energy sector, including tracking and authenticating the sale of renewable energy certificates and carbon credits (similar to the way blockchain currency is used) and more efficiently tracking energy transactions across a large number of sources (i.e., generation and storage at multiple solar and wind farms and residential locations).49 Antitrust issues may arise due to a fundamental aspect of blockchain technology: the members of a blockchain have access to a virtual ledger (embedded list) containing details for all transactions made on that blockchain. This ledger could, in theory, allow renewable energy firms to access transaction details of competitors, which could lead to claims of illegal coordination. Blockchain remains a nascent technology and its use cases, and the potential antitrust risk that may result, are still being explored. Renewable energy companies considering employing blockchain in their business—or considering joining an existing blockchain consortium that includes competing firms—should consult qualified antitrust counsel to determine what antitrust risks, if any, are present.

DOJ and FTC Business Reviews

Finally, although renewables firms should consult antitrust counsel about the foregoing topics, there may be times when it remains unclear how antitrust authorities will react to a business plan. In these circumstances, renewables firms (singly or together) may approach the FTC or DOJ for a business review. At the FTC, this is called seeking an Advisory Opinion, and is generally used to clarify the FTC’s interpretation of the FTC’s own rules and decisions or of its interpretation of laws that the FTC enforces.50 At DOJ, this is called seeking a Business Review Letter, and is used for seeking DOJ’s reaction to conduct that is within DOJ’s jurisdiction and is only in the planning stages (the conduct must not have begun commercially).51 The FTC process is generally faster (roughly one month), and used for simpler questions; the DOJ process, slower (usually three months or more), and used for more complex facts. These are unusual requests—the DOJ issues on average fewer than five business reviews per year—but key guidance for several technology industries has emerged from business reviews, so renewables firms should give the process serious consideration, if the need arises.

Conclusion

As the renewable energy industry continues its growth, it will increasingly face the same antitrust issues as do other key energy sectors, and those issues will arise not only in the United States but also throughout the world. This survey article provides a sample of what the issues may be. Of course, the complex nature of the industry and the law means that no article can cover the issues comprehensively. Deal makers in the renewable energy industry should consider making antitrust a standard part of their evaluation processes, and should involve experienced antitrust counsel at an early stage of any deal involving substantial values that may trigger a merger control filing, or any deal involving potential competitive overlaps.

1Short-Term Energy Outlook (July 8, 2025), U.S. Energy Info. Admin, https://www.eia.gov/outlooks/steo/.

2Share of energy consumption from renewable sources in Europe, European Environment Agency (Jan. 16, 2025), https://www.eea.europa.eu/en/analysis/indicators/share-of-energy-consumption-from.

3Massive global growth of renewables to 2030 is set to match entire power capacity of major economies today, moving world closer to tripling goal, International Energy Agency (Oct. 9, 2024), https://www.iea.org/news/massive-global-growth-of-renewables-to-2030-is-set-to-match-entire-power-capacity-of-major-economies-today-moving-world-closer-to-tripling-goal.

4Dep’t of Justice & Fed. Trade Comm’n, Merger Guidelines (Dec. 18, 2023), available at https://www.ftc.gov/system/files/ftc_gov/pdf/2023_merger_guidelines_final_12.18.2023.pdf.

515 U.S.C. § 18 (2018).

615 U.S.C. § 18A (2018).

716 C.F.R. §§ 801.1–803.90 (2019).

8This can be shortened to about ten days if the deal is “early terminated” due to clearly having no anticompetitive impact, or 15 days in the case of qualifying tender offers or bankruptcy transactions.

9Premerger Notification Office, HSR threshold adjustments and reportability for 2023, FTC Blogs (Feb. 16, 2023), https://www.ftc.gov/enforcement/competition-matters/2023/02/hsr-threshold-adjustments-reportability-2023.

10See Fed. Trade Comm’n, Steps for Determining Whether an HSR Filing is Required, https://www.ftc.gov/enforcement/premerger-notification-program/hsr-resources/steps-determining-whether-hsr-filing (last visited July 15, 2025). The transaction also must satisfy the “commerce” test, meaning that “either party is engaged in commerce or in any activity affecting commerce,” but this is virtually always met.

1116 C.F.R. § 801.1(b) (2019).

12In almost all HSR Act filings, each of the acquiring and acquired parties must file its own separate HSR form. An HSR notification is not considered to be complete, and the waiting period does not begin to run, until each party’s filing is submitted and the required filing fee has been paid.

13Fed. Trade Comm’n, Valuation of Transactions Reportable under The Hart-Scott-Rodino Act, https://www.ftc.gov/enforcement/premerger-notification-program/hsr-resources/valuation-transactions-reportable-under (last visited July 15, 2025).

14Fed. Trade Comm’n, When to Aggregate under the HSR Act, https://www.ftc.gov/enforcement/premerger-notification-program/hsr-resources/when-aggregate-under-hsr-act (last visited Oct. 30, 2023).

1515 U.S.C. § 18A(c)(1) (2018).

16Fed. Trade Comm’n, Valuation of Transactions Reportable under The Hart-Scott-Rodino Act, https://www.ftc.gov/enforcement/premerger-notification-program/hsr-resources/valuation-transactions-reportable-under (last visited July 15, 2025).

17Id.

18See Holly Vedova, Keitha Clopper & Clarke Edwards, Bureau of Competition, Avoiding antitrust pitfalls during pre-merger negotiations and due diligence, FTC Blogs (May 20, 2018), https://www.ftc.gov/news-events/blogs/competition-matters/2018/03/avoiding-antitrust-pitfalls-during-pre-merger.

19Id.

20Note that merger control exemptions are highly specific to particular jurisdictions. If a deal is potentially subject, for example, to merger control laws in both the United States and Canada, do not assume that an HSR filing exemption under United States law also applies to Canada’s Competition Act or in other jurisdictions.

2116 C.F.R. § 802.2(a) (2019).

22See, e.g., Fed. Trade Comm’n, 1704004 Informal Interpretation (Apr. 21, 2017), https://www.ftc.gov/enforcement/premerger-notification-program/informal-interpretations/1704004 (acquisition of newly constructed solar power facilities).

2316 C.F.R. § 802.2(b) (2019).

2416 C.F.R. § 802.2(c) (2019)

2516 C.F.R. § 802.4 (2019).

26See 16 C.F.R. § 801.10(d) (2019) (determining valuation of “an acquisition of non-corporate interests that confers control of either an existing or a newly-formed unincorporated entity”).

2716 C.F.R. § 802.10 (2019).

2816 C.F.R. § 802.64 (2012).

2916 C.F.R. § 802.65 (2019).

3015 U.S.C. § 19 (2018).

31See 15 U.S.C. § 19(a)(2)(A) (2018); Revised Jurisdictional Thresholds for Section 8 of the Clayton Act, 90 Fed. Reg. 7697 (Jan. 22, 2025).

3215 U.S.C. § 45.

33Also known in the law as “concerted action.”

34Single-firm anticompetitive conduct is known in the law as a “monopolization” offense, a term which can be confusing to lay audiences because almost all antitrust offenses involve monopoly in one sense or another

35Brown Shoe Co. v. United States, 370 U.S. 294, 320 (1962).

36See Press Release, Federal Trade Commission Withdraws Health Care Enforcement Policy Statements, Fed. Trade Comm’n (July 14, 2023), https://www.ftc.gov/news-events/news/press-releases/2023/07/federal-trade-commission-withdraws-health-care-enforcement-policy-statements; Press Release, Justice Department Withdraws Outdated Enforcement Policy Statements, Dep’t. of Justice (Feb. 3, 2023), https://www.justice.gov/opa/pr/justice-department-withdraws-outdated-enforcement-policy-statements.

37Michael Bloom, Information exchange: be reasonable, FTC Blogs (Dec. 11, 2014), https://www.ftc.gov/news-events/blogs/competition-matters/2014/12/information-exchange-be-reasonable.

38Id.

39See Dep’t. of Justice, United States v. KeySpan Corp., available at https://www.justice.gov/atr/case/us-v-keyspan-corp (last visited July 15, 2025).

40This formulation was stated first in the context of health care purchasing cooperatives. See Dep’t. of Justice & Fed. Trade Comm’n, Statements of Antitrust Enforcement Policy in Health Care (August 1996), at n.17, available at https://www.justice.gov/atr/page/file/1197731/download. It has since become understood as an industry-agnostic approach.

41Id. at § 7(A).

42Id. at n.17.

43Fed. Trade Comm’n & Dep’t. of Justice, Antitrust Guidelines for Collaborations Among Competitors (April 2000), at § 4.2, available at https://www.ftc.gov/sites/default/files/documents/public_events/joint-venture-hearings-antitrust-guidelines-collaboration-among-competitors/ftcdojguidelines-2.pdf. DOJ under the Biden Administration withdrew this guidance in 2023. “Justice Department Withdraws Outdated Enforcement Policy Statements,” Dep’t. of Justice (Feb. 3, 2023), https://www.justice.gov/archives/opa/pr/justice-department-withdraws-outdated-enforcement-policy-statements. But the Biden Administration did not replace it, and since the guidance was based on case law, there is no reason to consider it to be incorrect. The Trump Administration has not specifically addressed this guidance.

44Id. Note that application of merger analysis is unlikely to be a problem in this context, since a de facto merger that does not create more than 20% market share is unlikely to be challenged.

45See “FTC and DOJ Withdraw Guidelines for Collaboration Among Competitors,” Fed. Trade Comm’n (Dec. 11, 2024), https://www.ftc.gov/news-events/news/press-releases/2024/12/ftc-doj-withdraw-guidelines-collaboration-among-competitors.

46So named for two landmark Supreme Court cases that helped establish the rules. See Eastern R.R. Presidents Conference v. Noerr Motor Freight, Inc., 365 U.S. 127 (1961); United Mine Workers v. Pennington, 381 U.S. 657 (1965).

47Parker v. Brown, 317 U.S. 341 (1943).

48Keogh v. Chicago & Nw. Ry., 260 U.S. 156, 162-63 (1922) (railroad shipping rates); Nantahala Power & Light Co. v. Thornburg, 476 U.S. 953 (1986) (FERC decision pre-empts inconsistent state regulatory order); Mississippi Power & Light Co. v. Mississippi ex rel. Moore, 487 U.S. 354 (1988) (same); Taffet v. Southern Co., 967 F.2d 1483 (11th Cir.) (en banc), cert. denied, 13 S. Ct. 657 (1992) (RICO claim barred, rates filed with state public service commissions).

49Scott Deatherage, Mutually Evolving Technologies: Blockchain, Renewable Energy, and Energy Storage, ABA Business Law Today (Dec. 13, 2019), https://www.americanbar.org/groups/business_law/publications/blt/2019/12/evolving-tech/.

50See Fed. Trade Comm’n, Advisory Opinions, https://www.ftc.gov/policy/advisory-opinions.

51See Dep’t. of Justice, Business Review Letters and Request Letters, https://www.justice.gov/atr/business-review-letters-and-request-letters.