[co-author: John McLean]

Startups continue to have an increasingly international presence (or, at the very least, an international plan), and investors continue to scour the globe for investment opportunities. Therefore, it is important for both founders and investors to understand the key differences between the U.S. and the UK’s most common instruments for startup’s first round of capital or bridging instruments. These instruments are typically used as they are far less expensive than implementing a full suite of documentation for a priced round, and they are very quick to prepare as they often take a standard format in each jurisdiction.

So, what are these documents?

- The simple agreement for future equity (SAFE) (U.S.) and the advance subscription agreement (ASA) (UK) although it is more and more common to see the SAFE adapted to English companies

- Convertible loan notes, commonly referred to as just convertible notes in the U.S. (either referred to as CLNs throughout).

A potentially unfamiliar term like “ASA” to a U.S.-based startup and “SAFE” to a UK-based startup should not stop them from seeking investment across the Atlantic. However, it is important to understand the standard structure and potential tax implications of these instruments in each jurisdiction to determine which instrument is the right vehicle.

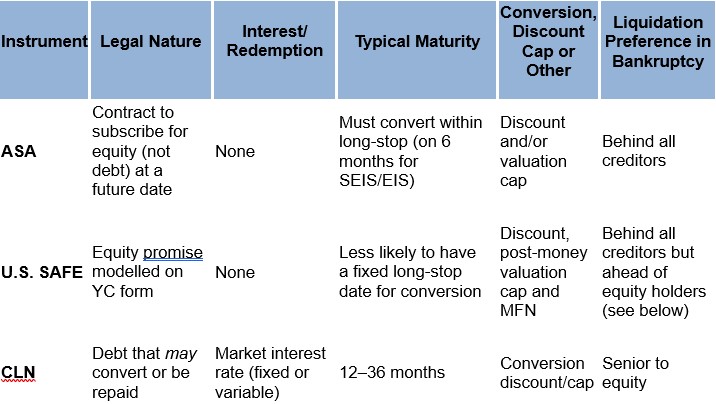

High-Level Summary of Each Instrument

SAFEs: Originally developed by Y Combinator (YC), SAFEs are popular with U.S. investors as a fast, (usually) more founder-friendly alternative to a convertible loan note to raise capital without setting a current valuation. (See a comparison focused on just SAFEs and CLNs

here.) This article will discuss the three most common YC SAFEs: (1) post-money valuation cap, (2) discount and (3) most-favored nation (MFN).

(In the interest of time, this article will not tackle preferential rights such as information rights, pro rata rights or liquidation preferences contained in side letters that can accompany SAFEs. You can, however, reach out to the Pillsbury team to discuss.)

ASAs: A widely used UK investment instrument that allows funds to convert into equity at a future date, typically on the long-stop date (usually 6 months as dictated by requirements for SEIS or EIS) or during the next priced funding round. ASAs are straightforward, quick to implement, and offer flexibility for both founders and investors. Note, if companies have used Seedlegals, they will have a SeedFast (which is the same thing in essence), and, as mentioned above, we are starting to see SAFEs adapted to UK companies becoming more and more common.

CLNs: A convertible debt instrument that allows the investor to either convert their loan into equity at a later stage or be repaid at maturity. CLNs are often used when investors want downside protection, such as interest accrual, security interests, creditor rights in events of default, and/or repayment rights at a maturity date. The CLN is more costly to put into place than an ASA or SAFE so is not used as frequently in the early funding rounds of startups. Further, a CLN is not an appropriate instrument in those instances where the investor is seeking SEIS or EIS relief.

Similarities and Differences

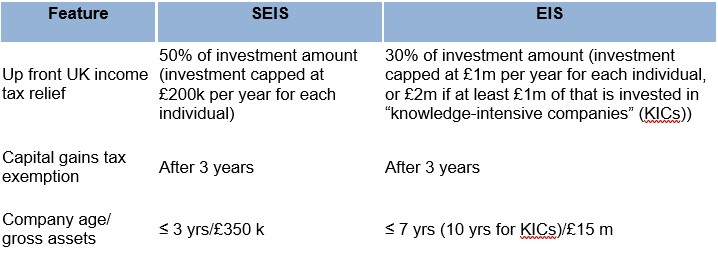

Requirements for UK SEIS/EIS Tax Relief (current law as at 26 August 2025)

The Seed Enterprise Investment Scheme (SEIS) and Enterprise Investment Scheme (EIS) are UK-government tax incentive programs designed to encourage investment in early-stage (SEIS) and growth-stage (EIS) startups by offering significant tax relief to individual investors similar to U.S. state-specific angel investor tax creditors (similar to SEIS) and “qualified small business stock,” a.k.a. QSBS, explored here. (Our colleagues have also examined recent amendments increasing its benefits under the One Big Beautiful Bill Act that was passed into U.S. law on July 4, 2025.)

Non-UK companies can still benefit from SEIS or EIS using SAFEs, if structured right. Even if your company is incorporated outside the UK (like in Delaware), you can still raise investment under SEIS/EIS, but only if the company has a real UK presence. That usually means a UK office or team doing meaningful work (like marketing or R&D) with UK-based contracts. Without that UK “permanent establishment,” the tax relief isn’t available to your investors. This structure often appears in climate tech flips where a Delaware top-co migrates IP to a new UK hold-co yet maintains U.S. operations.

Only equity qualifies; CLNs won’t qualify for SEIS/EIS. If they include things like interest, repayment rights, or look too much like debt, they’ll likely be disqualified. Under U.S. GAAP, the same instrument might still be shown as a liability, so it’s important to think about how this affects your books and investor reporting. Her Majesty’s Revenue and Customs (HMRC), the UK tax authority, expects conversion into ordinary shares: Shares with preferential rights (such as a U.S. VC-style liquidation preference, anti-dilution or a right to accumulating dividends ahead of dividends payable to ordinary shareholders) are not eligible for SEIS/EIS relief.

The June 2025 HMRC’s Tightening of Conditions

To qualify for SEIS or EIS, HMRC now expects any ASA or SAFE to include a fixed long-stop date of six months or less from the date of the agreement. The document should clearly state this date and include an automatic (and guaranteed) conversion trigger, usually the earlier of a priced funding round or the long-stop date. This ensures the investment is a genuine equity subscription, not a debt instrument. Comparatively, the standard form U.S. SAFE provides no guaranteed conversion mechanism and therefore no guaranteed equity interest in the company issuing such SAFE.

The agreement must also exclude any interest or coupon payments. For SEIS/EIS to apply, the investment must be equity only, with no guaranteed return.

It’s also critical that the instrument doesn’t give the investor a right to redeem or demand repayment. The agreement should use “conversion only” language, meaning the investor either converts to equity or walks away with nothing. SEIS/EIS eligibility depends on the investment being made “wholly in cash,” and any repayment right is treated as failing to meet this requirement. “Repayment” for these purposes includes the return of a SAFE investor’s investment or some other cash amount upon dissolution of the company. Investors should carefully examine whether forgoing the one guaranteed form of repayment (contingent of course on the company dissolving) is worth receiving UK tax relief.

Lastly, investor veto rights must be kept to a minimum. Broad consent rights (e.g., requiring investor approval for business plans, hiring decisions, or future fundraising) suggest the investor has control, which HMRC does not allow under SEIS/EIS. Instead, limit protections to what’s legally required under the UK Companies Act 2006—such as shareholder approval for issuing new shares or changing the company’s articles. MFNs (usually reserved for the earliest SAFE investors and almost always in a SAFE with a discount) appear in more SAFEs than ASAs because MFNs risk SEIS/EIS eligibility. For example, if a startup issues another ASA with preferential terms to an existing ASA with an MFN, then the holder of the existing ASA now automatically benefits from (or in some cases has the right to elect to benefit from) such preferential terms. This means the shares issuable under the existing ASA may have preferential rights that render them ineligible for SEIS/EIS tax benefits.

Failure to comply means HMRC will refuse advance assurance of SEIS/EIS eligibility or claw back relief later.

Further Considerations

If your main goal is to raise SEIS- or EIS-qualifying investment quickly and efficiently, an ASA is usually the best fit. ASAs are simple, low-cost to prepare, and, when drafted correctly, are the most HMRC-friendly option. They work well for UK-based angel rounds and are familiar to UK investors who prioritise tax relief.

If you’re working with U.S. investors, especially those used to making pre-seed investments via SAFEs, a “UK SAFE” may be more appropriate than an ASA. It mimics the core economics of an ASA, but is called a SAFE. When drafted properly, a UK SAFE can still work for SEIS/EIS, while keeping U.S. seed investors comfortable.

A UK SAFE—meaning eligible for SEIS/EIS—differs from U.S. SAFEs in the following important ways:

- It must convert into shares by a certain date no longer than 6 months from the date of the agreement (not upon certain events), not just contemplate the right to convert into shares.

- It must convert into ordinary (i.e., common) shares or SEIS/EIS complaint preference shares. Relatedly, side letter agreements granting certain rights preferential to other investors as discussed above cannot be executed as a condition to providing capital to a company under a UK SAFE.

- It must convert into a certain number of shares at a determinable price (i.e., no MFN or valuation cap or discount on its own). A pre- or post-money valuation cap, discount SAFE may qualify for SEIS/EIS if otherwise structured correctly.

- “Debt-like” features, including any right to demand repayment, to receive interest, or to repayment of investment or some other cash amount upon dissolution of the company must be removed.

For later-stage or more cautious investors who want stronger downside protection, a CLN may be preferred. CLNs are structured as debt: They accrue interest, rank ahead of equity if the company fails, and typically include a maturity date that allows the investor to force repayment. However, CLNs don’t qualify for SEIS or EIS, and they introduce more complexity and risk to the company’s balance sheet which might affect government funding applications which can require a certain debt-to-equity ratio.

Common Pitfalls and HMRC Red Flags

It’s important to tailor your investment documents to support your fundraising goals, long-term strategy and eligibility for available tax reliefs.

- One common mistake is using an evergreen SAFE, i.e., a SAFE with no fixed deadline for conversion or long-stop date. HMRC expects any SEIS-/EIS-qualifying instrument to convert into shares within six months, or it won’t approve advance assurance. Without this clear timeframe, the investment is viewed as too open-ended and not genuinely at risk.

- Another issue is adding interest to an ASA. The moment interest is included, HMRC will likely treat the agreement as a debt instrument, which automatically disqualifies it from SEIS/EIS relief. These schemes are strictly for equity investments, so any debt-like features raise a red flag.

- Be careful, too, with what kind of shares your ASA or SAFE converts into. If it converts into preference shares (rather than ordinary shares), the investment will not satisfy the requirements for SEIS/EIS tax relief unless those preference shares are carefully crafted to comply with the requirements.

- Finally, using any veto rights from a U.S. investor with high leverage can cause problems. Including broad investor controls, such as requiring investor consent for major business decisions, can make the investment look like debt. To qualify for SEIS/EIS, the investor must take real equity risk, not have rights that reduce their exposure. Keep consent rights to the legal minimum required under UK company law.

Deciding On an Instrument

[View source.]