In This Edition

SEC Developments

Corporate Law Developments

Stock Exchange Developments

Other Developments

U.S. Equity & Debt Markets Activity – Q2 2025

SEC Developments

SEC Reverses Course on Gensler-Era Rule Proposals – Withdraws Proposed Amendments to Its Shareholder Proposal Rule

The Bottom Line

- Among other Gensler-era rule proposals withdrawn by the SEC, the SEC withdrew its 2022 rule proposal that proposed amendments to certain substantive bases under Exchange Act Rule 14a-8 for excluding shareholder proposals from proxy statements.

- The proposed amendments under the 2022 rule proposal would have made it more difficult for issuers to exclude shareholder proposals from their proxy statements.

The Details

In a broad reversal of course on proposed rules issued by the Securities and Exchange Commission (SEC) under the leadership of former SEC Chair Gary Gensler, on June 12, 2025, the SEC issued a notice withdrawing fourteen of the proposed rules.

While most of the withdrawn proposals (thirteen of them) relate to investment management, and trading and markets matters, the SEC also withdrew its July 2022 rule proposal (the “rule proposal”) that had proposed amendments to certain substantive bases for excluding shareholder proposals from issuers’ proxy statements for annual or special shareholder meetings under the SEC’s shareholder proposal rule, Rule 14a-8 under the Securities Exchange Act of 1934 (the “Exchange Act”).

The withdrawal of the rule proposal will be welcome news to issuers as the proposed amendments, which would have amended the substantial implementation, duplication, and resubmission exclusion bases, would have made it more difficult for issuers to exclude shareholder proposals from their proxy statements. The public comment period for the rule proposal had been closed since September 12, 2022, and based on the SEC’s fall 2024 regulatory flexibility agenda, final rules were planned for adoption in October this year.

While the substantial implementation exclusion permits an issuer to exclude a shareholder proposal that “[it] has already substantially implemented,” the duplication exclusion permits an issuer to exclude a shareholder proposal if the proposal “substantially duplicates another proposal previously submitted to [it] by another proponent that will be included in [its] proxy materials for the same meeting,” and the resubmission exclusion permits an issuer to exclude a shareholder proposal if it “addresses substantially the same subject matter as a proposal, or proposals, previously included in [its] proxy materials within the preceding five calendar years” if the matter was voted on at least once in the last three years and received support below specified vote thresholds on the most recent vote.

In the rule proposal, which we discuss in detail here, the SEC proposed to amend:

- the substantial implementation exclusion by specifying that a proposal may be excluded on that ground only if “essential elements” of the proposal have been implemented;

- the duplication exclusion by specifying that “substantially duplicates” means that a proposal “addresses the same subject matter and seeks the same objective by the same means” as a previously submitted proposal; and

- the resubmission exclusion by changing the “addresses substantially” standard to a “substantially duplicates” standard (as defined above).

In the notice of withdrawal, the SEC noted that it will publish new proposed rules if it decides to pursue future regulatory action on any of the withdrawn rules.

The withdrawal of the rule proposal follows the SEC Division of Corporation Finance’s issuance of SEC Staff Legal Bulletin No. 14M in February 2025 (which we discuss here) to clarify its application of the economic relevance and ordinary business exclusion bases of its shareholder proposal rule, and shows that the SEC remains focused on its shareholder proposal rule.

In Concept Release, SEC Invites Public Brainstorming on Reconsidering the Foreign Private Issuer Definition

The Bottom Line

- Given significant changes in the population of foreign private issuers (FPIs) over the past two decades that have resulted in more FPIs not being subject to robust home country disclosure requirements, among other concerns, the SEC is seeking public comment on whether, and how, to amend the FPI definition.

- The SEC is soliciting public input on several possible approaches to amending the FPI definition, including (i) revising the current test (e.g., by lowering the 50 percent ownership threshold or revising the U.S. assets threshold), (ii) requiring that a certain percentage of an FPI’s trading volume occur outside the U.S., (iii) requiring FPIs to be listed on a “major foreign exchange,” and (iv) limiting FPI status to issuers incorporated or headquartered in certain jurisdictions.

The Details

On June 4, 2025, the SEC published a concept release (the “Concept Release”) seeking public comment on whether, and how, to amend the definition of “foreign private issuer” considering significant changes in the FPI population and the regulatory accommodations afforded to FPIs under federal securities laws. While the Concept Release does not propose any rule changes, it poses many questions that signal that the SEC is questioning whether the current FPI test still identifies the class of foreign companies for which the SEC’s longstanding regulatory accommodations—some of which allow FPIs to follow their home country rules—remain appropriate.

The Concept Release represents the most significant step in the reevaluation of the FPI definition in a quarter-century. While the SEC’s ultimate course is uncertain, companies currently relying on FPI status, or considering accessing the U.S. capital markets as FPIs, should closely monitor the SEC’s next steps.

Key Developments Prompting Reconsideration

The Concept Release presents SEC staff data showing dramatic changes in the FPI population over the past two decades that, according to the SEC, undercut two assumptions underlying the FPI accommodations: (i) that FPIs would be subject to meaningful disclosure and regulatory requirements in their home countries and (ii) that their securities would be primarily traded in foreign markets. The changes in the FPI population highlighted in the Concept Release are:

- Shifts in FPI Jurisdictions: There has been a dramatic change in the incorporation and headquarter jurisdictions of FPIs that file annual reports on Form 20-F (20-F FPIs), with the Cayman Islands and mainland China being, respectively, the most common incorporation and headquarter jurisdictions in 2023, as compared with Canada and the United Kingdom being the most common jurisdictions for both incorporation and headquarters in 2003. The data also show a notable increase in FPIs incorporated in the British Virgin Islands, as well as in FPIs whose incorporation jurisdictions differ from their headquarter jurisdictions. According to the Concept Release, the Cayman Islands, the British Virgin Islands, and some other jurisdictions of incorporation that have become more common have limited or minimal home country disclosure and reporting requirements.

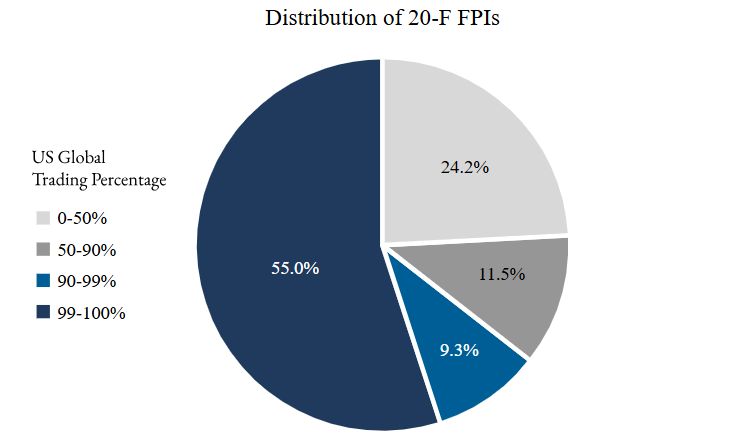

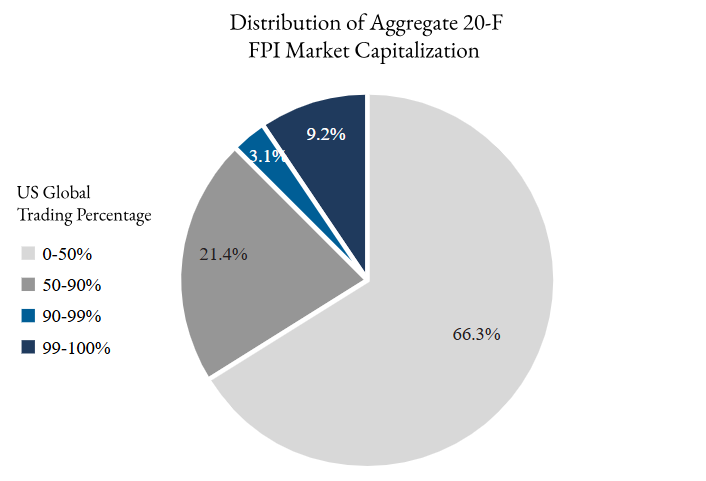

- Increased U.S. Market Reliance: A majority of 20-F FPIs—most of whom have smaller market capitalizations and have a higher propensity of being incorporated in the Cayman Islands and headquartered in China—now have their equity securities traded almost exclusively in the U.S. capital markets, rather than in foreign markets. Specifically, in fiscal year 2023, approximately 55 percent of 20-F FPIs had 99 percent or more of the global trading of their equity securities in the U.S. capital markets. That group, however, made up only 9.2 percent of the aggregate 20-F FPI market capitalization.

Concerns Arising from the Change in FPI Population

According to the SEC, these developments raise the following concerns:

- Less Disclosure Available to Investors: As the changes in FPI jurisdiction have resulted in more FPIs not being subject to robust home country disclosure requirements, U.S. investors are likely receiving less information about FPIs and their securities, increasing risks to U.S. investors and creating competitive disparities with domestic issuers.

- Regulatory Arbitrage: Some FPIs may be seeking to minimize regulatory costs by incorporating in jurisdictions with less stringent requirements or by listing primarily in the U.S. without meaningful foreign oversight.

- Home Country Exemptions: Certain foreign jurisdictions, such as Israel, provide exemptions from their own disclosure requirements for issuers that qualify as FPIs under U.S. law, further reducing the regulatory oversight of these companies.

Approaches Under Consideration

The SEC is soliciting public input on several possible approaches to amending the FPI definition, including:

- Updating Existing Eligibility Criteria: Revising the current bifurcated test (shareholder ownership and business contacts tests), such as lowering the 50 percent U.S. ownership threshold or revising the U.S. assets threshold.

- Foreign Trading Volume Requirement: Introducing a requirement that a certain percentage of an FPI’s trading volume occur outside the U.S. (e.g., 1%, 5%, 10%, or higher).

- Major Foreign Exchange Listing Requirement: Requiring FPIs to be listed on a “major foreign exchange” to ensure they are subject to meaningful foreign regulation and oversight.

- Commission Assessment of Foreign Regulation: Limiting FPI status to issuers (i) incorporated or headquartered in jurisdictions that the SEC determines have robust regulatory and oversight frameworks and (ii) that are subject to such regulations and oversight without modification or exemption.

- Mutual Recognition Systems: Developing systems of mutual recognition for issuers from selected foreign jurisdictions, like the existing Multijurisdictional Disclosure System (MJDS) with Canada.

- International Cooperation Arrangement Requirement: Requiring FPIs to be subject to the oversight of a foreign securities authority that is a signatory to the IOSCO Multilateral Memorandum of Understanding Concerning Consultation, Cooperation, and the Exchange of Information (MMoU) or the Enhanced MMoU.

SEC Staff Updates Rule 10b5-1 Guidance

In April 2025, the SEC staff updated its Compliance and Disclosure Interpretations (C&DIs) relating to Exchange Act Rule 10b5-1, the SEC rule which provides an affirmative defense to allegations of insider trading liability for sales and purchases of securities made pursuant to contracts, instructions, or written plans that satisfy all of the rule’s requirements. While most of the updates involve withdrawals and revisions of C&DIs to conform the C&DIs to the 2022 amendments to the rule, which we discuss here, the SEC staff issued two new C&DIs as part of the update:

- The SEC staff clarified that trades in issuer securities through a 401(k) plan pursuant to a self-directed “brokerage window” may only get the benefit of the rule’s affirmative defense if the instruction for any self-directed “brokerage window” transaction satisfies all conditions of Exchange Act Rule 10b5-1(c)(1), including those applicable to purchases and sales of the issuer’s securities on the open market.

- Among other conditions, to qualify for the affirmative defense, a person (other than an issuer) may not have more than one qualifying plan for trades in an issuer’s securities on the open market, subject to certain exceptions, including that a plan for an eligible sell-to-cover transaction will not be considered a qualifying plan for this purpose. The rule defines an eligible sell-to-cover plan as one that authorizes an agent to sell only such securities as are necessary to satisfy tax withholding obligations arising exclusively from the vesting of a compensatory award, where the insider does not otherwise exercise control over the timing of such sales. In its updated guidance, the SEC staff clarified that the definition’s reference to “necessary to satisfy tax withholding obligations” means tax withholding payments that are calculated to satisfy the insider’s expected effective tax obligation solely with respect to the vesting transaction (and does not mean the minimum tax withholding obligation imposed under the applicable tax rules).

Corporate Law Developments

Texas Adopts Significant Corporate Law Changes, Intensifying Race for Corporate Law Dominance

The Bottom Line

- A Texas corporation’s charter may now dispense with the need for separate class votes in approving any matter, including fundamental business transactions and charter amendments (such as increases or decreases in the number of the class’s authorized shares).

- Texas corporations may opt to make it more difficult to find directors and officers liable for fiduciary duty breaches (even in the context of conflicted transactions) by imposing liability only where the business judgment rule presumption is rebutted and the breach involved fraud, intentional misconduct, an ultra vires act, or a knowing violation of law.

- Shareholders of nationally listed Texas corporations or Texas corporations with at least 500 shareholders will find it more difficult to institute derivative actions; to institute a derivative action, a shareholder must satisfy the corporation’s share ownership threshold (not exceeding three percent of outstanding shares) for instituting such action.

- Texas corporations may now include a waiver of the right to a jury trial in respect of internal claims in their governing documents.

- From September 1, 2025, nationally listed corporations that are headquartered in Texas or listed on a Texas exchange may amend their governing documents to restrict the submission of shareholder proposals by allowing only shareholders who (i) hold at least $1 million in market value of the corporation’s voting shares (or at least three percent of such shares), (ii) hold such shares continuously for at least six months before the shareholder meeting, and (iii) solicit holders of at least sixty-seven percent of the corporation’s voting shares, to submit such proposals.

- Texas corporations may now petition a court to determine the disinterestedness of the directors on special board committees established to approve conflicted transactions.

- Shareholders may generally not obtain emails and other electronic communications in books and records demands, and Texas corporations may opt to impose further conditions on such demands, including prohibiting demands that are in connection with derivative actions.

The Details

In May 2025, Texas intensified its bid to unseat Delaware as the corporate law jurisdiction of choice by passing two laws back-to-back: Texas Senate Bill 29 (SB 29), adopted by the Texas Legislature on May 7 and signed into law on May 14, and Texas Senate Bill 1057 (SB 1057), adopted by the Texas Legislature on May 6 and signed into law on May 19. Both laws make significant changes to the Texas Business Organizations Code (TBOC). While SB 29 is effective immediately, SB 1057 is effective September 1, 2025.

We summarize the main changes below.

Class Vote Exemptions

Changes to Authorized Shares. SB 29 amends Section 21.364 of the TBOC to dispense with separate class votes on charter amendments that increase or decrease the number of authorized shares of a class and instead requires only a vote of holders of a majority of the corporation’s stock if such exemption is provided for in the certificate of formation or in a charter amendment adopted before the issuance of shares of the class or authorized by holders of a majority of the shares of the class. This change brings the TBOC in line with Section 242(b)(2) of the Delaware General Corporation Law (DGCL), which it mirrors, and would make it easier for Texas corporations that comply with its conditions to pass such charter amendments. Under the TBOC, the default voting standard for such charter amendments is a vote of holders of two-thirds of the corporation’s stock and a vote of holders of two-thirds of the class shares.

General Exemption. SB 29 goes even further by allowing Texas corporations to dispense with separate class votes in all cases by providing in their charters that only a vote of all classes of stock as a single class shall be required to approve any matter, including a charter amendment and a fundamental business transaction. This is a significant change and a major distinction from the DGCL, which does not include a similar provision. For example, this means that a corporation could include in its original charter or a charter amendment a provision dispensing with a class vote for charter amendments that seek to change the preferences or rights of a class of shares, though it is doubtful that such a provision would be acceptable to shareholders.

Codification of Business Judgment Rule

New Section 21.419 of the TBOC (the “BJR provision”) codifies the business judgment rule for corporations with voting shares listed on a national securities exchange, as well as corporations that elect to be governed by the BJR provision. It provides that directors and officers of such corporations are presumed to act (i) in good faith, (ii) on an informed basis, (iii) in the corporation’s interests, and (iv) in compliance with law and the corporation’s governing documents. Under the BJR provision, such directors and officers may only be held liable where (i) the business judgment rule presumption is rebutted, (ii) the director’s or officer’s act or omission constituted a breach of duty, and (iii) the breach involved fraud, intentional misconduct, an ultra vires act, or a knowing violation of law. In suits against such directors or officers, the circumstances of the fraud, intentional misconduct, ultra vires act, or violation of law to be stated with particularity.

As compared to Delaware law, the BJR provision is notable in two major respects. First, it means that, unlike in Delaware where a breach of the duty of loyalty is sufficient for director liability, such directors may only be liable for breaches of their duty of loyalty where there is fraud, intentional misconduct, an ultra vires act, or a knowing violation of law. Second, it means that, unlike in Delaware, such directors who are grossly negligent may still not be found liable for breaching their duty of care.

Application to Conflicted Transactions Involving Directors and Officers. Relatedly, new Section 21.418(f) reinforces this provision in the context of corporate transactions in which directors or officers have an interest. It provides that, even where the safe harbor procedures or requirements for such transactions are not satisfied, directors or officers of corporations that are governed by the BJR provision will not be liable for breach of duty in respect of such transactions unless the BJR provision’s conditions for liability are met.

Committee of Disinterested Directors for Approval of Conflicted Transactions

Under an amendment to Section 21.416, boards of certain corporations (those with voting shares listed on a national securities exchange or that elect to be governed by the BJR provision) may form a committee (which may be a standing committee) of independent and disinterested directors to approve transactions involving the corporation (or any of its subsidiaries) and a controlling shareholder, director, or officer. In addition, new Section 21.4161 permits a corporation that forms such a committee to petition the Texas business court or a Texas district court, as applicable, to determine whether the directors on such committee are independent and disinterested with respect to any such transaction. A petitioning corporation must notify its shareholders of the petition and their right to participate in the action.

Share Ownership Threshold for Derivative Actions

SB 29 imposes a significant restriction on the ability of shareholders of certain corporations to pursue derivative actions. To institute or maintain a derivative action, a shareholder of a corporation with common shares listed on a national securities exchange or that is governed by the BJR provision and has at least 500 shareholders, will now need to beneficially own shares that meet a share ownership threshold specified in the corporation’s governing documents. That threshold may, however, not exceed three percent of the corporation’s outstanding shares.

Waiver of Jury Trial

New Section 2.116 of the TBOC allows corporations to include a waiver of the right to a jury trial in respect of internal claims in their governing documents. It also provides that such waivers will be enforceable, regardless of whether the governing document is signed by the corporation’s shareholders, directors, or officers. This provision seeks to empower Texas corporations to place themselves in the same position as Delaware corporations, given that jury trials are unavailable in the Delaware Chancery Court.

Restrictions on Books and Records Demands

On the heels of Delaware’s recent lead in restricting books and records demands, SB 29 amends Section 21.218, governing books and records demands, to clarify that, for purposes of such demands, a corporation’s records shall not include emails, text messages, or similar electronic communications, or information from social media accounts, unless they effect a corporate act. Amended Section 21.218 further provides that a shareholder’s books and records demand shall not be permissible if (i) the demand is in connection with derivative actions instituted or expected to be instituted by the shareholder or its affiliates or is in connection with a civil lawsuit in which the shareholder (or its affiliates) and the corporation (or its affiliates) are adverse parties, and (ii) the corporation has voting shares listed on a national securities exchange or has elected to be governed by the BJR provision.

Exclusive Forum Provision

Amended Section 2.115 clarifies that a corporation’s charter or bylaws may provide that one or more Texas courts shall serve as the exclusive forum and venue for any internal claims.

SB 1057 – Restrictions on Submission of Shareholder Proposals

Effective September 1, 2025, “nationally listed corporations” will have the option to impose the conditions discussed below (including share ownership and holding-period conditions) on the submission of shareholder proposals at shareholder meetings (other than director nominations and procedural resolutions ancillary to the conduct of meetings).

This option is not limited to Texas corporations, as a nationally listed corporation is a corporation that (i) has its principal office in Texas or is listed on a Texas exchange (i.e., a Texas-authorized stock exchange with its principal office in Texas), (ii) has a class of equity securities registered under the Exchange Act, and (iii) is listed on a national securities exchange.

Specifically, nationally listed companies may require that a shareholder or shareholder group may only submit a proposal for consideration at a shareholder meeting if the shareholder or shareholder group:

- holds voting shares of the corporation of at least (i) $1 million in market value or (ii) three percent of the corporation’s voting shares;

- holds such shares continuously for at least six months before the meeting and through the meeting’s duration; and

- solicits shareholders representing at least sixty-seven percent of the voting power of shares entitled to vote on the proposal.

To have these conditions apply to its shareholders, a nationally listed corporation must amend its governing documents to provide that it has elected to be governed by those conditions.

Notably, while the holding period conditions are more lenient than those shareholders must satisfy under Exchange Act Rule 14a-8 for their proposals to be eligible for inclusion in a corporation’s proxy statement for a shareholders’ meeting, the share ownership thresholds are markedly more onerous than under Rule 14a-8; under Rule 14a-8, a shareholder must have continuously held at least $2,000, $15,000, or $25,000 in market value of a corporation’s voting shares for at least three years, two years, or one year, respectively. Relatedly, while the solicitation condition has no analogue under Rule 14a-8, it mirrors the solicitation requirement under Exchange Act Rule 14a-19 that applies to solicitation of proxies for dissident director nominees.

Nevada Enacts Corporate Law Changes in Push to Enhance Its Corporate Law Standing

The Bottom Line

- Nevada corporations may now include in their charters a waiver of the right to a jury trial in respect of internal actions to be tried in Nevada courts.

- Under the Nevada corporate law changes:

- Controlling stockholders are the only stockholders that have a fiduciary duty. A controlling stockholder’s only fiduciary duty is to refrain from unduly influencing a director or officer to induce a breach of the director’s or officer’s fiduciary duty in relation to a controlling stockholder transaction involving the controlling stockholder.

- A controlling stockholder is presumed not to have breached its fiduciary duty where the transaction is approved by a board committee of only disinterested directors or by the board in reliance on the recommendation of such a committee.

- A controlling stockholder transaction is one in which (i) a controlling stockholder is a party or has a material and nonspeculative financial interest, and (ii) receives a material, nonspeculative, and non-ratable financial benefit, resulting in a material and nonspeculative detriment to other stockholders generally. In contrast, the recent DGCL amendments do not expressly impose a materiality requirement and contemplate that the controlling stockholder’s benefit could be nonfinancial.

- A “controlling stockholder” is defined simply as a stockholder with voting power to elect at least a majority of the corporation’s directors, a much narrower definition than under the DGCL amendments.

- The changes make it easier for publicly traded Nevada corporations to amend their charters solely to increase or decrease the number of their authorized shares by requiring only the vote of the affected class for such charter amendments and allowing such vote on a majority-of-votes-cast basis.

The Details

On May 30, 2025, the Governor of Nevada signed Nevada Assembly Bill 239 (AB 239) into law, effective immediately. Among other things, AB 239 amends certain provisions of the Nevada Revised Statutes governing Nevada corporations. The amendments, which include revisions that address a couple of concepts that featured in the 2023, 2024, and March 2025 amendments to Delaware’s corporate statute, the DGCL, are intended to enhance Nevada’s competitive standing among Delaware and other corporations that may be looking to reincorporate in other jurisdictions.

We discuss the more significant amendments below.

Waiver of Jury Trial

In a bid to afford Nevada corporations with the option of having cases tried by judges, as is the case in the Delaware Chancery Court where jury trials are unavailable, the amendments provide that a corporation’s charter may require that certain or all internal actions to be tried by a Nevada court must be tried by a judge and not by a jury, and that such a requirement will operate as a waiver of jury trial by the parties to such internal actions. Under Nevada corporate law, internal actions are generally actions against directors, officers, or controlling stockholders for breach of fiduciary duty or actions arising from a corporation’s charter, bylaws, or stoc lder-related agreement.

Controlling Stockholder Provisions

The amendments address the fiduciary duties of controlling stockholders, providing that a controlling stockholder’s fiduciary duty may only arise where a controlling stockholder receives a material, nonspeculative, and non-ratable financial benefit from a transaction to which the controlling stockholder (including any of its affiliates or associates) is a party or in which the controlling stockholder has a material and nonspeculative financial interest, and such financial benefit is to the exclusion of, and results in a material and nonspeculative detriment to, the other stockholders generally. Specifically, the amendments provide that a controlling stockholder’s only fiduciary duty is to refrain from unduly influencing a director or officer to induce a breach of the director’s or officer’s fiduciary duty in relation to such a transaction. Notably, the scope of a controlling stockholder transaction under the Nevada amendments is narrower than under the recent DGCL amendments—unlike the DGCL amendments, which contemplate that a controlling stockholder’s benefit could be non-financial, the Nevada amendments require the controlling stockholder’s benefit to be financial in nature. Furthermore, while the Nevada amendments require that the benefit must be material, the DGCL amendments do not expressly impose a materiality requirement.

Unlike the DGCL amendments, which provide procedural safe harbor protections from controlling stockholder transactions where a transaction has been approved (or recommended for approval) by a disinterested board committee or by a majority of votes cast by disinterested stockholders (or both, in the case of going-private transactions), the Nevada amendments only create a presumption that the controlling stockholder has not breached its fiduciary duty where the transaction is approved by a board committee of only disinterested directors or by the board in reliance on the recommendation of such a committee.

Importantly, the Nevada amendments’ definition of “controlling stockholder” is much narrower than the definition under the DGCL amendments. Under the Nevada amendments, a controlling stockholder is simply a stockholder with voting power to elect at least a majority of the corporation’s directors. In contrast, under the DGCL, a controlling stockholder is a stockholder who:

- Owns or controls a majority of the voting power of the corporation’s stock entitled to elect directors; or

- Owns or controls at least one-third of the voting power of the corporation’s stock entitled to elect directors or to elect directors entitled to cast a majority voting power of all directors, and has the power to exercise managerial authority over the corporation’s business and affairs.

Relatedly, while not in identical terms to the DGCL amendments, the Nevada amendments’ definition of “disinterested director” is substantially the same as that under the DGCL amendments. Under the Nevada amendments, a disinterested director is a director who is not a party to the transaction, does not have a material and nonspeculative financial interest in the transaction, and, in the case of a company with stock listed on a national securities exchange, would satisfy the audit committee director independence requirements under applicable SEC rules and the exchange’s rules. While the DGCL’s definition only requires that the director not have a material interest in the transaction and not be a party to the transaction, the DGCL amendments provide that, for a similarly listed company, a non-party director would be presumed not to have a material interest in the transaction if the company’s board has determined that the director meets the exchange’s independence standards.

The Nevada amendments also make clear that a stockholder that is not a controlling stockholder shall not have any fiduciary duty to the corporation or any other stockholder.

Publicly Traded Corporations: Changes to Number of Authorized Shares

The amendments make it easier for publicly traded corporations to amend their charters solely to increase or decrease the number of their authorized shares by providing that only the vote of the affected class will be required for such charter amendments and that the default voting standard for the affected class’s vote will be the majority-of-votes-cast standard. Before the amendments, the default voting standard applicable to all corporations (and still applicable to non-publicly traded corporations) for such charter amendments was the majority-of-voting-power standard. While the amendments mainly mirror the 2023 DGCL amendments that introduced a default majority-of-votes-cast standard for such charter amendments by publicly traded Delaware corporations, such charter amendments should be easier for Nevada corporations, because, unlike the DGCL amendments which also require a majority-of-votes-cast vote of stockholders in general (i.e., not only a class vote), the Nevada amendments only require a vote of the affected class.

Delaware Supreme Court Agrees to Answer Constitutional Questions Arising from Recent Delaware Corporate Law Amendments

On June 11, 2025, the Delaware Supreme Court accepted two constitutional questions certified to it by the Delaware Chancery Court in relation to recent amendments to the Delaware General Corporation Law, which we discuss here, regarding safe harbor provisions for controlling stockholder transactions and conflicted transactions involving directors or officers. Among other things, the amendments, which were effected by Senate Bill 21 (SB 21) effective March 25, 2025, eliminated the Chancery Court’s ability to award either “equitable relief” or “damages” where the safe harbor provisions were satisfied and apply retroactively to transactions occurring before the enactment of SB 21, except transactions that are the subject of any court proceedings completed or pending on or before February 17, 2025, the date SB 21 was introduced in the Delaware Senate.

The constitutional questions that the Delaware Supreme Court will address are: (i) whether the provision eliminating the Chancery Court’s ability to award “equitable relief” or “damages” where the safe harbor provisions are satisfied violates the Delaware constitution by purporting to divest the Chancery Court of its equitable jurisdiction; and (ii) whether the retroactive application of SB 21 violates the Delaware constitution by purporting to eliminate causes of action that had already accrued or vested.

The questions were certified by the Chancery Court at the request of the plaintiff in Rutledge v. Clearway Energy Group LLC, et al.,No. 2025-0499 (Del. Ch. May 6, 2025), a derivative action challenging the fairness of Clearway Energy, Inc.’s purchase of an asset from its majority stockholder in 2024. In the action, the plaintiff sued both the majority stockholder and the chief executive officer of Clearway for breaches of fiduciary duty and sought a declaration that SB 21 is unconstitutional (on its face or as applied to the action). According to the plaintiff’s complaint, although the purchase was approved by a committee of directors deemed independent by Clearway’s board, the purchase was not approved by a majority of Clearway’s disinterested stockholders, an omission that would have called into question the fairness of the purchase under Delaware case law predating SB 21. SB 21 had, however, changed the law (retroactively, in the plaintiff’s case) by providing that controlling stockholder transactions that are not going-private transactions (such as the purchase) would be protected if they are either approved by such a board committee or by a majority of votes cast by disinterested stockholders.

According to the briefing schedule issued by the Delaware Supreme Court, filing of briefs of arguments on the questions is expected to be completed by September 19, 2025.

Stock Exchange Developments

Under New Rule, NYSE-only Listed Companies from Outside North America Can Comply with Holder Distribution Standards on a Global Basis

On May 2, 2025, the SEC approved an amendment to Section 102.01 of the New York Stock Exchange (NYSE) Listed Company Manual allowing companies organized outside North America (i.e., outside the U.S., Canada, and Mexico) listing in connection with an initial public offering (IPO)—and not listed on any other regulatory exchange—to take into account all of their stockholders on a global basis in complying with the NYSE’s minimum stockholder distribution standards.

Those distribution standards require companies conducting an IPO to have a minimum of 400 stockholders holding a trading unit or more of the relevant security (typically, one hundred shares). The amendment is effective immediately.

Under the previous rule, companies organized outside North America that are not listed on any other regulatory exchange could only count U.S. holders toward meeting the stockholder distribution standards, while such companies that are listed on another regulatory exchange could, in addition to U.S. holders, count holders from their home market only at the NYSE’s discretion. The amendment further clarifies that this discretion applies only when the issuer is listed on another regulated exchange.

The new rule is intended to enhance the NYSE’s competitiveness in attracting non-U.S. company listings, particularly relative to Nasdaq, which already permits worldwide stockholder counts. According to the NYSE, the amendment reflects the reality that modern cross-border settlement systems allow investors outside North America to participate effectively in U.S. trading markets.

By limiting the accommodation to companies for which the NYSE would be the sole regulated exchange, the NYSE believes the liquidity policy underlying the distribution standards will be satisfied since trading in the securities will be concentrated on the NYSE.

NYSE Rule Bars Listing Compliance Plans for Companies with Unpaid NYSE Fees

In May 2025, the SEC approved a new NYSE rule regarding the review of compliance plans submitted by listed companies that fall below continued listing standards. Under the new rule, the NYSE will not review or approve a compliance plan from a company that has any unpaid listing or annual fees as of the date of the non-compliance letter, which is the formal notification from the exchange that the company is out of compliance. The amount of unpaid fees will be disclosed in the letter. If the company fails to pay all outstanding fees by the compliance plan submission deadline (within forty-five days for domestic companies or ninety days for non-U.S. companies), the NYSE will promptly begin suspension and delisting procedures. Additionally, during the plan period, the NYSE will provide quarterly (or semi-annual for non-U.S. companies) written disclosures of any unpaid fees, and failure to pay these within forty-five days will also trigger the commencement of suspension and delisting procedures. The rule, however, does not apply to companies that are non-compliant solely due to late SEC filings or clawback requirements, as, according to the NYSE, those situations generally require less regulatory effort to resolve.

The rule is aimed at reducing the risk of non-payment of fees and ensuring that the NYSE is better able to allocate its resources by preventing companies with unpaid fees from utilizing the compliance plan process. In proposing the rule, the NYSE noted that reviewing and monitoring compliance plans is a resource-intensive process, requiring significant staff time and expertise, and that many companies that fall below compliance standards, particularly those with low market capitalization and limited liquidity, often delay fee payments and may never pay outstanding fees if ultimately delisted.

Other Developments

In Novel Law, Texas Mandates Disclosures for Proxy Advisory Services Not Provided Solely in Shareholders’ Financial Interests

Amendments to Sections 144 and 220 of the Delaware General Corporation Law, which respectively deal with conflicted transactions, and stockholder inspection of books and records, were signed into law on March 25, 2025, as part of an effort to maintain Delaware’s competitive edge as the preeminent jurisdiction for incorporation amid some recent exits of Delaware companies to other states.

The Bottom Line

- Beginning September 1, 2025, proxy advisory firms that provide proxy advisory services (including voting recommendations) to shareholders of publicly traded companies that are organized, headquartered, or proposing reincorporation in Texas must provide certain disclosures when those services are based on nonfinancial factors (such as environmental, social, or governance (ESG) factors, diversity, equity, or inclusion (DEI) considerations, or social credit or sustainability factors) and when they give conflicting voting recommendations to different shareholders on the same company or shareholder proposal.

- Among other things, in such cases, the proxy advisory firms must disclose to the shareholder clients that the service is not provided solely in the financial interest of the company’s shareholders.

- The law appears aimed at discouraging voting recommendations based on nonfinancial factors, thereby providing publicly traded companies with one more reason to consider reincorporating in Texas or moving their headquarters to Texas.

The Details

On June 20, 2025, the Governor of Texas signed into law Senate Bill 2337 (SB 2337), which requires proxy advisory firms to provide certain disclosures when their proxy advisory services are based on nonfinancial factors and when they give conflicting voting recommendations to different shareholders in respect of the same company or shareholder proposal. SB 2337 applies to proxy advisory services given to shareholders of publicly traded companies that are either organized or headquartered in Texas or are the subject of a pending proposal to reincorporate in Texas, and applies only to such advisory services provided on or after September 1, 2025. A “proxy advisory service” includes a voting advice or recommendation on a shareholder or company proposal (including a proposal regarding director nominations or elections); proxy statement research and analysis regarding such proposals, and a rating or research on corporate governance.

While the law is framed in investor protection terms—protecting investors from fraudulent or deceptive practices by proxy advisors—it would appear that the law is primarily aimed at discouraging proxy advisors from issuing voting recommendations that are based on nonfinancial factors, such as (ESG) factors, (DEI) considerations, or social credit or sustainability factors, and provide companies with one more reason to consider incorporating or reincorporating in Texas or moving their headquarters to Texas.

Required Disclosures

Services Not Based Solely on Shareholders’ Financial Interests. Under the new law, a proxy advisor that provides a proxy advisory service that is not provided solely in shareholders’ financial interests must:

- disclose to its shareholder clients receiving the service:

- that the service is not being provided solely in the financial interest of the company’s shareholders; and

- the basis of the proxy advisor’s advice on each recommendation and that the advice subordinates the financial interests of shareholders to other objectives;

- provide the company that is the subject of the service with a copy of the shareholder disclosure; and

- conspicuously disclose on its website that its services include advice and recommendations that are not based solely on the financial interests of shareholders.

Under the law, a proxy advisory service is not provided solely in the financial interest of shareholders if (i) it is based solely or partly on nonfinancial factors (such as ESG, DEI, or social credit or sustainability factors), (ii) without including an economic analysis of the financial impact of the proposal on shareholders, it recommends a vote on a shareholder proposal that is contrary to the voting recommendation of the company’s board on the proposal, or (iii) it recommends against voting for a company’s director nominee without stating that its recommendation is based solely on its consideration of the financial interest of shareholders.

Conflicting Advice to Different Shareholders on Same Proposal. In addition to the above disclosures, proxy advisors that provide materially different advice to different shareholder clients on a company or shareholder proposal where those clients have not requested the advice for a nonfinancial purpose must:

- notify the shareholder clients, the company that is the subject of the proposal, and the Texas attorney general of the conflicting advice; and

- disclose which of the conflicting advice is provided solely in the financial interest of the shareholders and supported by financial analysis relied on by the proxy advisor.

For this purpose, “materially different” advice includes advising one or more clients to vote for a proposal and one or more clients to vote against the proposal and advising one or more clients to vote for or against a proposal in opposition to the recommendation of the company’s management.

The Company Notice Requirement. According to SB 2337, the company notice mandated by both disclosure requirements is necessary because the “company . . . may have information regarding whether the proposal is in the shareholder’s financial interests or regarding the costs of the proposal, and notice would allow the company to provide relevant information to shareholders that may prevent fraudulent or deceptive practices associated with proxy advisors making recommendations for nonfinancial reasons.”

Enforcement

If a proxy advisor violates any of these requirements, the consumer protection division of the office of the Texas attorney general may bring an action for deceptive trade practice against the proxy advisor seeking injunctive relief and civil penalties. SB 2337 also provides a private right of action for violations, permitting recipients of the proxy advisory services, and the affected company and its shareholders to seek a declaratory judgment or injunctive relief against the proxy advisor.

Landmark Legislation to Regulate Payment Stablecoins Signed into Law

On July 18, 2025, U.S. President Donald J. Trump signed the GENIUS Act (Guiding and Establishing National Innovation for U.S. Stablecoins Act), an act designed to establish a framework for the regulation of “payment stablecoins,” into law. The GENIUS Act marks a significant development for both the digital asset and banking industries, establishing a comprehensive regulatory regime for payment stablecoins.

The GENIUS Act narrowly defines a “payment stablecoin” as a digital asset that is, or is designed to be, used as a means of payment or settlement, the issuer of which is obligated to convert, redeem, or repurchase it for a fixed amount of money, and represents that it will maintain, or create the reasonable expectation that it will maintain, a stable value relative to the value of a fixed amount of money.

The GENIUS Act primarily seeks to regulate the issuance of payment stablecoins in the United States, as well as the offer and sale of payment stablecoins in the United States by “digital asset service providers” (essentially, crypto exchanges and certain other crypto asset service providers). Specifically, the GENIUS Act limits the issuance of payment stablecoins in the United States to entities that are licensed to issue payment stablecoins (referred to as “permitted payment stablecoin issuers”) and prohibits digital asset service providers from offering or selling payment stablecoins that are not issued by permitted payment stablecoin issuers, subject to certain limited exceptions for non-U.S.-based issuers of payment stablecoins and limited safe harbors authorized by the Treasury Secretary. Among other things, the GENIUS Act provides that payment stablecoins are not securities or commodities, identifies the key agencies (primarily the same federal agencies that serve as primary regulators of banks and credit unions or certain state regulators) that will regulate permitted stablecoin issuers, details the types of assets that must be held by those issuers in reserves on at least a one-to-one basis with their outstanding payment stablecoins, and prohibits those issuers from paying any form of interest or yield on payment stablecoins.

We discuss the GENIUS Act in more detail here.

SEC Approves FINRA Rule Exempting Private and Non-Traded BDCs from IPO Investment Restrictions

On June 26, 2025, the SEC approved a rule change proposed by the Financial Industry Regulatory Authority, Inc. (FINRA) to facilitate the ability of certain business development companies (BDCs) to acquire securities in initial public offerings of equity securities (IPOs) by exempting those BDCs from FINRA Rule 5130 (Restrictions on the Purchase and Sale of Initial Equity Public Offerings) and FINRA Rule 5131(b) (New Issue Allocations and Distributions—Spinning). The exemption would apply to private BDCs and non-traded BDCs (i.e., BDCs that have shares registered under the Securities Act of 1933 but that are not listed on a national securities exchange), affording them the same exemptive treatment that currently applies to publicly traded BDCs and investment companies registered under the Investment Company Act of 1940 (Investment Company Act). The exemption will, however, apply to those BDCs only if they are not formed or maintained for the specific purpose of permitting restricted persons to invest in IPOs.

While FINRA Rule 5130 restricts the sale of IPOs to accounts or persons that have an insider position or a conflict of interest in the public offering process, including FINRA members, broker-dealers, broker-dealer personnel, certain owners of broker-dealers, and portfolio managers, and requires FINRA members to obtain representations as to compliance from accounts prior to IPO sales to their accounts, FINRA Rule 5131(b) restricts the allocation of IPO securities to accounts in which executive officers or directors of public companies or certain private companies have beneficial interests under certain conflict of interest situations.

The rule change aims to facilitate easier access to IPOs for private BDCs and non-traded BDCs, including by reducing the operational burdens they face in demonstrating their eligibility to purchase IPOs. The change should foster greater IPO diversification of the portfolios of these BDCs to the benefit of their investors, subject to the thirty percent cap in new issue investments applicable to BDCs under the Investment Company Act.

The effective date of the rule change will be announced by FINRA in a regulatory notice.

U.S. Equity & Debt Markets Activity – Q2 2025

(Data sourced from Dealogic)

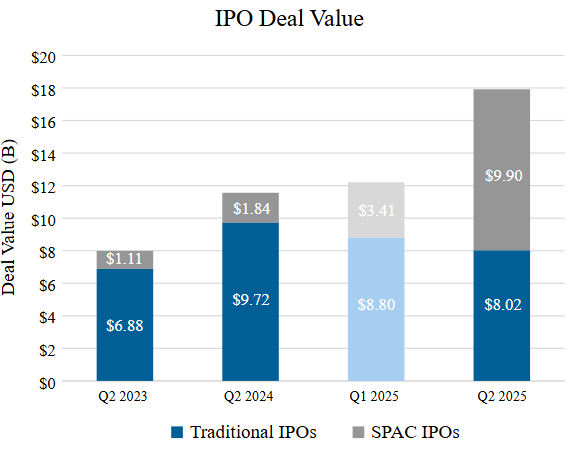

Traditional IPOs

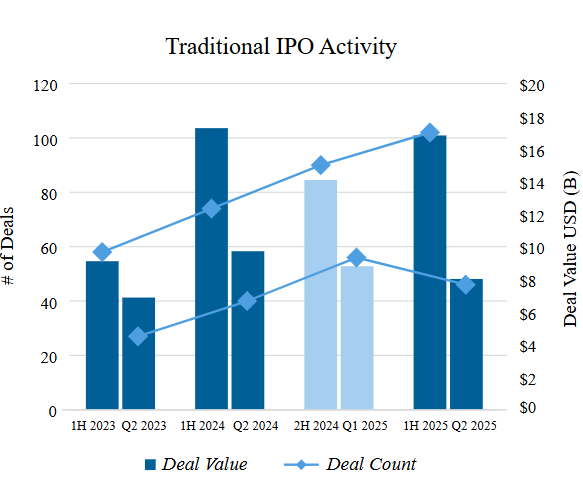

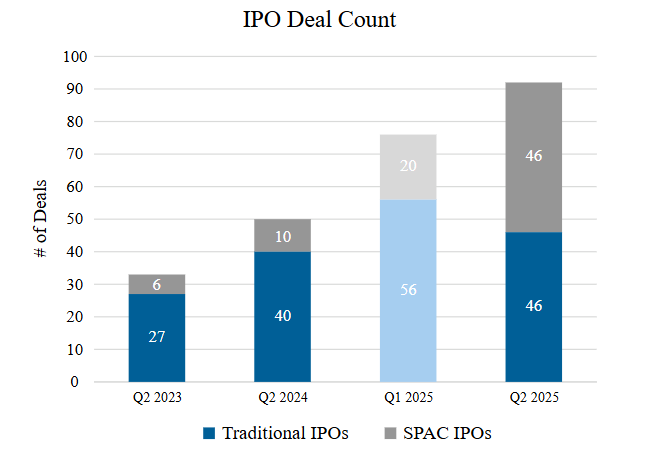

Traditional IPO activity was mixed in Q2 2025, as compared to Q2 2024, with deal value down by 17% but deal count up by 15%. As compared to Q1 2025, however, traditional IPO activity dipped in Q2 2025, down 9% in deal value and down 18% in deal count. The dip in deal count is particularly notable as the number of traditional IPOs has increased from one quarter to the next since Q4 2023. That notwithstanding, with 102 IPOs totaling $16.8 billion, the first half of 2025 (1H 2025) was better for the traditional IPO market than the preceding half year (2H 2024) with 90 IPOs totaling $14.1 billion (an increase of 19% in deal value and 13% in deal count). As compared with the first half of 2024 (1H 2024), however, while deal count in 1H 2025 increased significantly by 38%, deal value was down slightly (3%). Overall, in the first half of 2025, the traditional IPO market demonstrated resilience and growth over the previous half-year (2H 2024), but with deal values slightly lagging last year’s record (1H 2024) despite a notable increase in the number of IPOs, more growth is still needed in the market, with larger companies hopefully making their IPO debuts in the coming months.

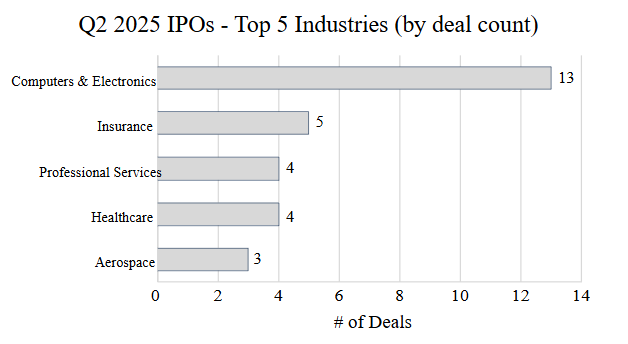

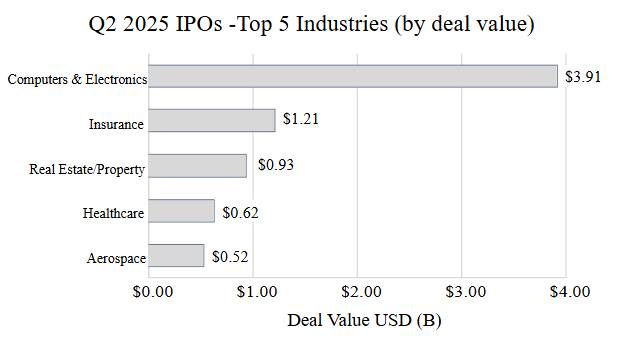

In Q2 2025, the computer and electronics industry continued to top the charts with thirteen IPOs raising $3.9 billion, almost triple the deal count and deal value of the insurance industry, which made a strong showing in Q2 2025, coming in second place by both deal value and deal count. Historically one of the top industries, healthcare dropped down the charts in Q2 2025 with only four healthcare IPOs raising $620 million.

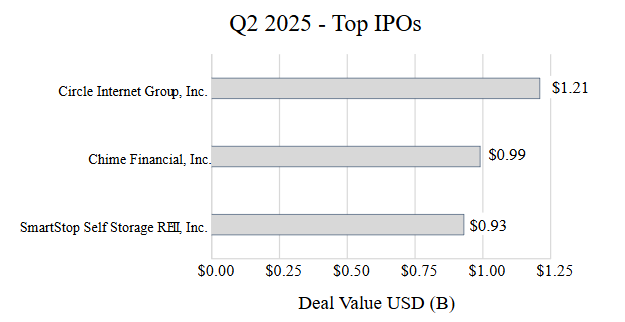

Cryptocurrency and financial technology made the headlines in Q2 2025, with the largest IPO (raising $1.2 billion) by Circle Internet Group, Inc., an issuer of payment stablecoins, and the second largest IPO (raising $990 million) by Chime Financial, Inc., a fintech company.

SPAC IPOs

Q2 2025 was a momentous quarter for IPOs by special purpose acquisition companies (SPACs), marked by a dramatic resurgence in activity, signaling renewed investor interest and momentum after several quieter years. SPAC IPOs boomed in Q2 2025 with forty-six IPOs raising nearly $10 billion, over four times the deal value (up 439%) and 4.5 times the deal count (up 360%) in Q2 2024—records not seen in three years. Compared to Q1 2025, SPAC IPOs were nearly triple in deal value (up 191%) and 2.5 times in deal count (130%).

Follow-Ons

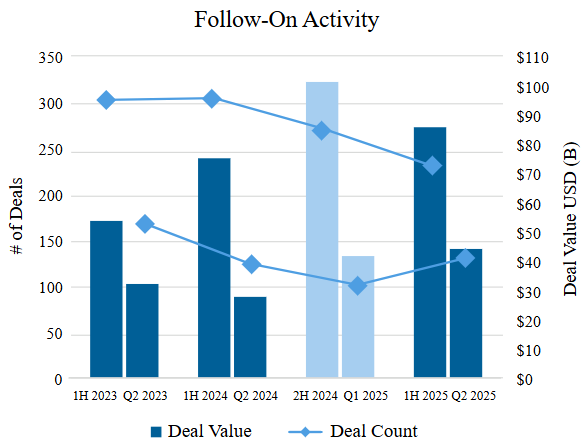

While there was only a modest (5%) increase in the number of follow-on offerings (FOs) in Q2 2025 as compared to Q2 2024, there was a significant increase in deal value with issuers raising 59% more funds than in Q2 2024. Compared to Q1 2025, the uptick in activity was flipped with deal value up only by 6%, while deal count jumped by 29%. Overall, 1H 2025 was mixed as compared to 1H 2024—up 14% by deal value but down 24% by deal count.

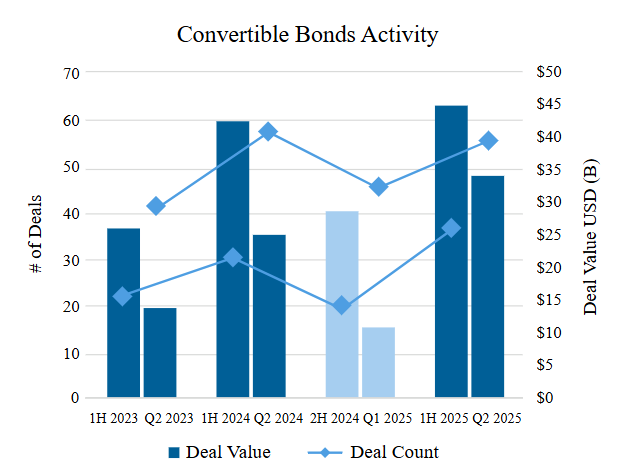

Convertible Bonds

Q2 2025 was a record quarter for the convertible bonds market, recording the highest numbers in deal value and deal count since at least Q1 2023. Convertible bond issuance accelerated sharply in Q2 2025, with Q2 2025 numbers outpacing activity in the second half of 2024, suggesting issuers are increasingly turning to this financing option.

As compared to Q2 2024, deal value and deal count were up 36% and 20%, respectively, in Q2 2025. The increase in activity was greatly amplified as compared to Q1 2025, with deal value more than tripling and deal count nearly doubling. Convertible bond activity overall in 1H 2025 was pretty level with 1H 2024, up just 6% by deal value and down only 4% by deal count.

Investment-Grade Debt

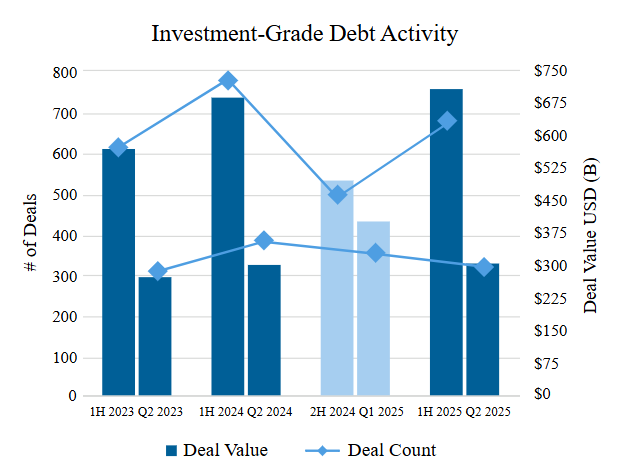

Issuance of investment-grade corporate bonds [1] was down in Q2 2025 by deal count as compared to Q2 2024 (16%) and Q1 2025 (9%), but deal value was more mixed—relatively flat with Q2 2024 and down almost a quarter from Q1 2025. Investment-grade corporate bond issuance in 1H 2025 was mixed compared to 1H 2024 (up 3% by deal value and down 14% by deal count), but 1H 2025 significantly outperformed 2H 2024 with a 42% increase in deal value and a 37% increase in deal count. Despite a dip in deal count, investment-grade corporate bond issuance remains robust in 2025, indicating continued strong demand for high-quality debt.

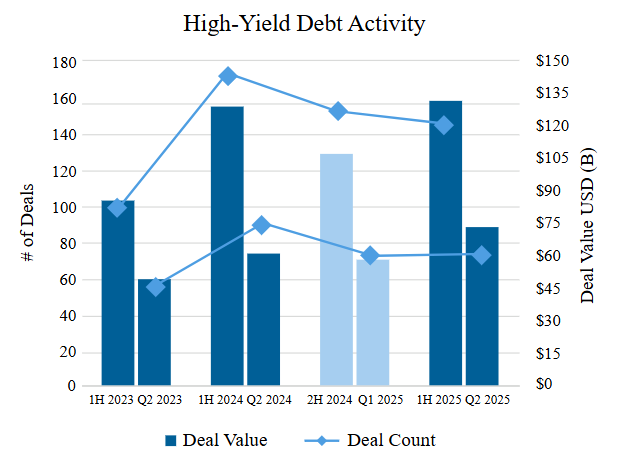

High-Yield Debt

While the number of high-yield debt offerings in Q2 2025 decreased by 19% as compared to Q2 2024, deal value increased by almost the same amount (20%). Compared to Q1 2025, deal value was up even more (26%) but deal count held steady, up by only one deal. Overall, 1H 2025 was up just 2% by deal value from 1H 2024 but down 16% by deal count. All in all, high-yield debt offerings are seeing higher deal values but fewer transactions.