In Dealmaker’s Digest, read the top 10 latest developments in global transactions. We offer insights into M&A activity across industries and borders.

Key Takeaways

- The first half of 2025 saw a 13% increase in global deal value and 5% increase in U.S. deal value from the same period last year.

- Aggregate global monthly deal value in June exceeded $450 billion, the highest monthly value in three years.

- U.S. crossborder activity in Q2 2025 declined by most metrics from Q1.

Global M&A Activity Update

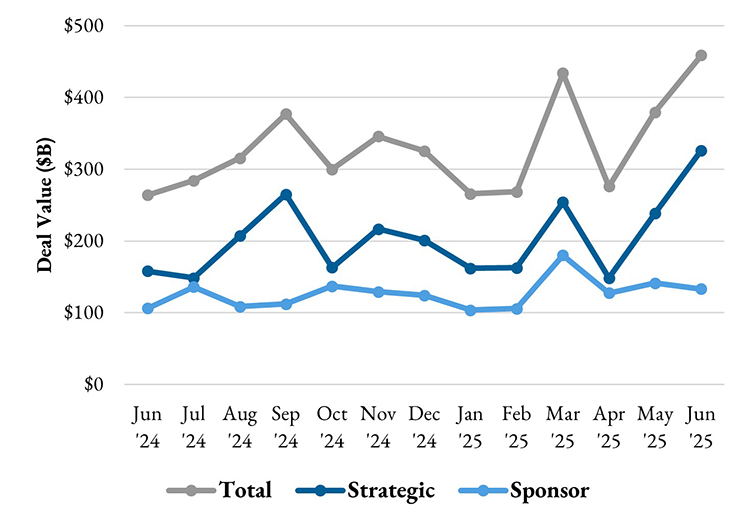

Monthly Deal Value Trends

Monthly Deal Value Trends

Aggregate global monthly deal value1 in June increased 21% from May to over $450 billion, the highest monthly value since May 2022. Total deal value was up 74% year-over-year.

Aggregate global monthly deal value1 in June increased 21% from May to over $450 billion, the highest monthly value since May 2022. Total deal value was up 74% year-over-year.

Transactions involving strategic buyers surpassed $325 billion in June, a 37% increase from May. Strategic deal value more than doubled (107%) year-over-year, driven by multiple June mega-deals in the software and industrials sectors.

Financial, or sponsor, buyer transactions decreased slightly in June, down 6% by value from May but up 25% year-over-year.

Financial, or sponsor, buyer transactions decreased slightly in June, down 6% by value from May but up 25% year-over-year.

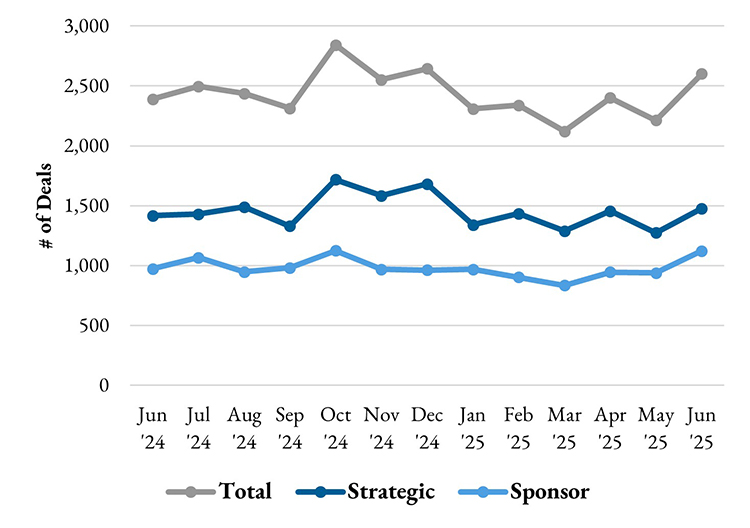

Monthly Deal Count Trends

Monthly Deal Count Trends

Global deal count in June reached its highest level since December; monthly deal count increased 17% from May and 9% year-over-year.

Strategic buyer deal count in June increased 16% from May and remained roughly steady year-over-year (+4%).

Sponsor buyer deal count in June was up 19% month-over-month and increased 15% year-over-year.

Crossborder Corner

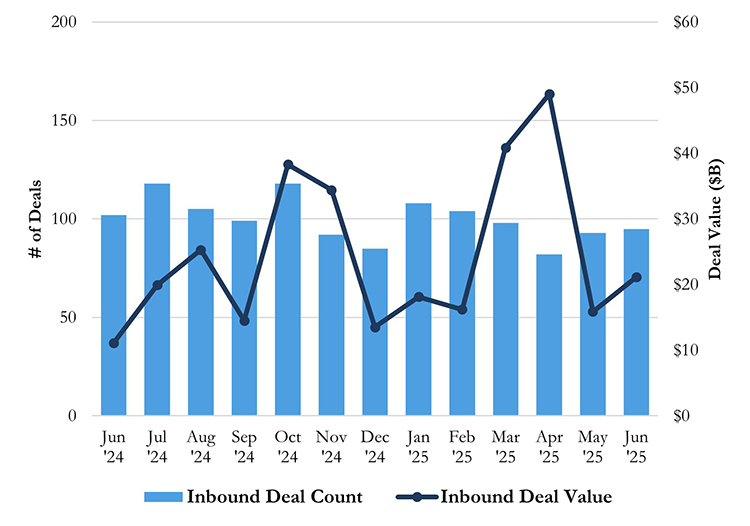

Monthly Inbound U.S. M&A Activity

Monthly Inbound U.S. M&A Activity

- By deal value, inbound U.S. activity increased 33% in June after declining sharply in May. Year-over-year, inbound deal value jumped 91%. Nearly half of June inbound value resulted from Sanofi’s $9.6 billion acquisition of Blueprint Medicines.

- By deal count, acquisitions of U.S. targets by non-U.S. acquirers held steady in June (up by only two transactions). Year-over-year, inbound deal count declined 7%.

- UK and Canada-based acquirers undertook the largest number of inbound transactions in June, with 17 and 13 deals, respectively. France-based acquirers followed with 9 inbound deals.

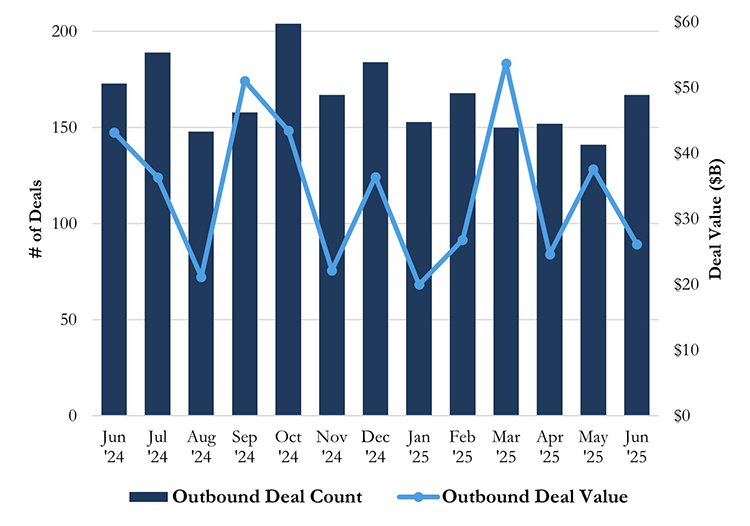

Monthly Outbound U.S. M&A Activity

Monthly Outbound U.S. M&A Activity

- By deal value, acquisitions of ex-U.S. targets by U.S. buyers in June dropped 31% from May, and 40% year-over-year.

- By deal count, outbound activity increased 18% from May to June. Year-over-year, outbound deal count held steady (-3%).

- U.S. acquirers predominantly looked to targets in the UK in June, with 47 transactions. Canada and Australia-based targets followed, with 17 and 12 deals, respectively.

Quarterly Review

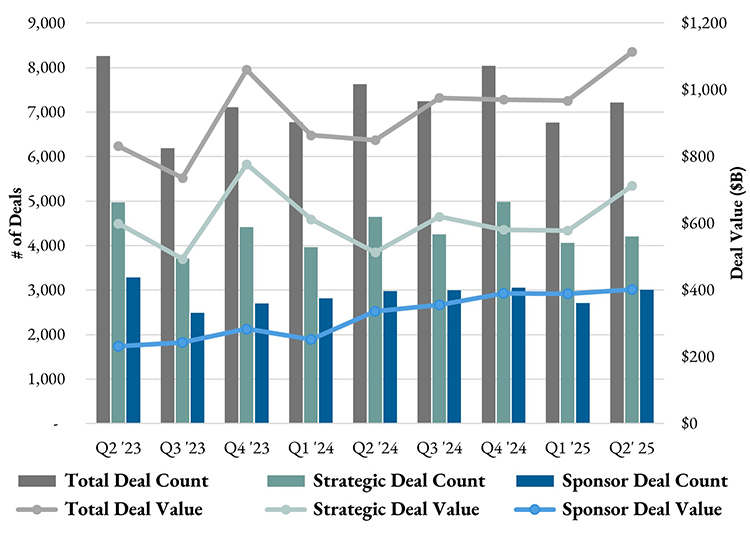

Quarterly Global M&A Activity

Quarterly Global M&A Activity

- Global M&A activity in Q2 2025 was up 15% by deal value quarter-over-quarter to a three-year record of $1.1 trillion. Compared with the same period last year (Q2 2024), deal value jumped 31%.

- Strategic deal value drove the increase, up 23% quarter-over-quarter, while sponsor deal value held steady (+3%). Compared with Q2 2024, strategic and sponsor deal value were up 39% and 19%, respectively.

- Global deal count in Q2 2025 increased 7% quarter-over-quarter, with sponsor activity (+11%) outpacing strategic deals (+4%). Compared to Q2 2024, deal count across buyer types held roughly steady.

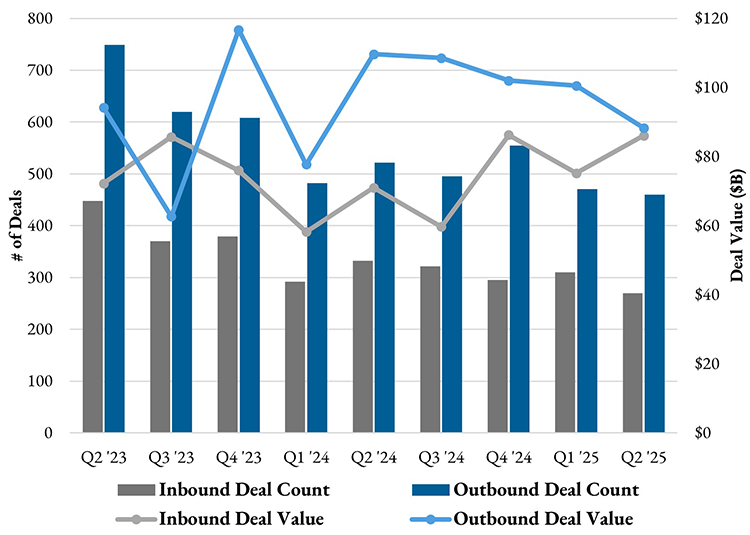

Quarterly U.S. Crossborder Activity

Quarterly U.S. Crossborder Activity

- U.S. crossborder activity was down by most metrics from Q1 2025, although inbound deal value increased 15% quarter-over-quarter and 21% compared with Q2 of last year.

- Outbound deal value in Q2 2025 was down 12% quarter-over-quarter and 19% compared with Q2 2024.

- Crossborder activity by deal count was mixed: quarter-over-quarter, inbound deal count was down 13%, while outbound activity held steady (-2%). Compared with Q2 2024, volume was down across the board: inbound deal count was down by 19%, and outbound by 12%.

Quarterly Active M&A Industries (U.S. Targets)

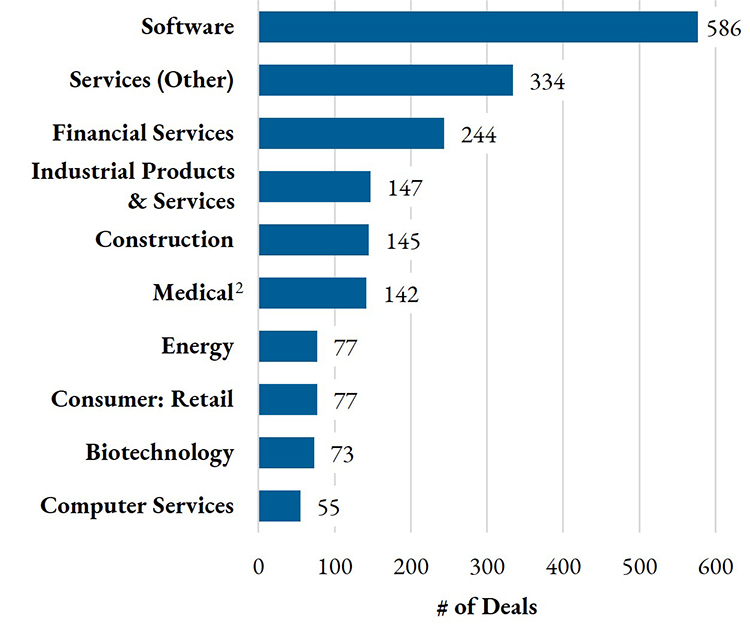

By Deal Count

By Deal Count

- The software industry remained at the top for U.S. M&A activity by deal count in Q2 2025, continuing its streak as the leading industry by volume.

- Services industries remained active, with financial services and other professional services rounding out the top three sectors in Q2 2025 by deal count.

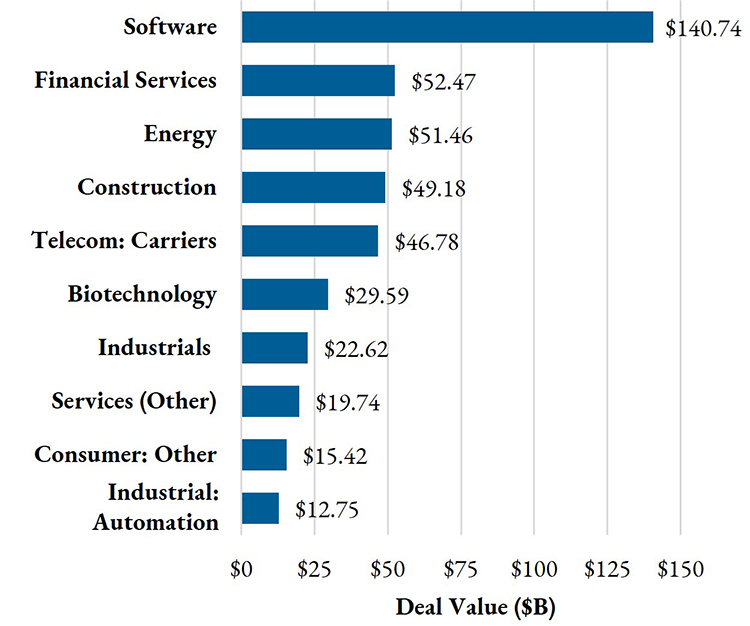

By Deal Value

By Deal Value

- The software industry also topped the charts by deal value in Q2 2025, more than doubling M&A value of any other industry.

- The financial services and energy sectors trailed, each exceeding $50 billion in aggregate value, closely followed by deals in the construction and telecom industries.

Quarterly Blockbuster Deals

Quarterly Blockbuster Deals

2025 First-Half Recap

2025 First-Half Recap

M&A activity was generally mixed in the first half (“1H”) of 2025. Global, U.S. and crossborder deal counts declined from last year, with a slowdown in U.S. deal volume coinciding with tariff-driven market volatility. Despite the macroeconomic headwinds, global and U.S. deal value marginally outpaced 1H 2024, with numerous transformative deals announced through June.

A snapshot of 1H 2025 metrics, and how they stack up against last year’s midway point: