Dealmakers in Europe have had plenty of reasons to pause forward movement on deals. From new tariffs on transatlantic trade to weak industrial output in Germany—which also saw a snap election in February—2025 has brought a wave of uncertainty.

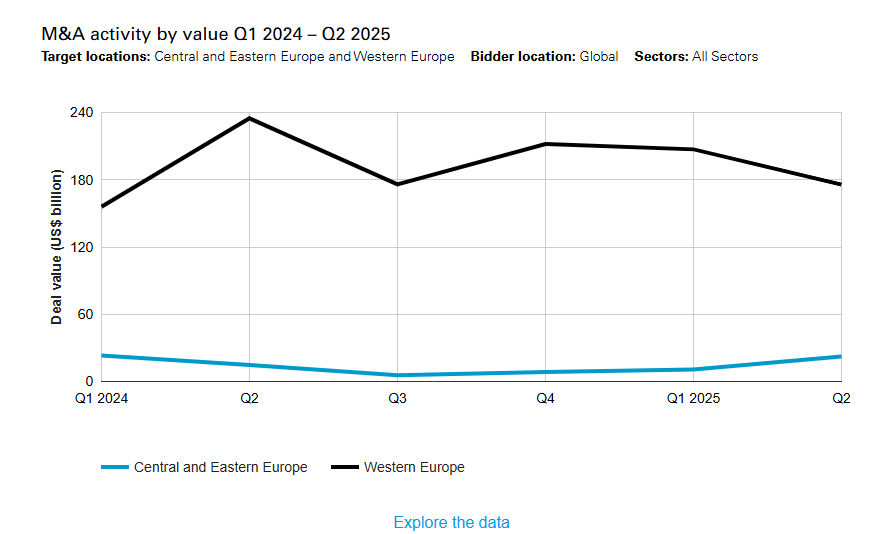

Yet M&A activity has held up remarkably well. In the first half of the year, total deal value reached US$416 billion across 6,634 transactions, just 2.6 percent below the US$427 billion recorded in H1 2024, despite a steeper 18.1 percent fall in volume. This is indicative of a market led by fewer, larger transactions, as companies pursue transformative opportunities and private equity returns to the fray.

The summer has seen a wealth of deals being announced across the continent. At the time of writing (August 11), annual value has risen to US$547 billion, just 10 percent lower than the first three quarters of 2024.

By the numbers

One of the clearest signals of current market stress, however, has been the increasing prominence of distressed M&A. With slowing growth, elevated input costs and tight financing conditions, more companies across Europe are facing liquidity and solvency challenges.

According to consultancy Alvarez & Marsal, 32 percent of European companies had fragile balance sheets even before the latest wave of tariffs was introduced, marking the highest proportion since 2021. Structural weaknesses are now colliding with macroeconomic inertia, pushing more businesses into formal processes and triggering heightened deal activity in the distressed space.

That trend is borne out in the numbers. Distressed M&A activity in Europe, which covers a cross-section of liquidations, bankruptcies and restructurings, rose in value but declined in volume in H1 2025.

A total of 163 deals were announced across administration, distressed and liquidation processes, down 10.9 percent from 183 in the same period last year. However, aggregate deal value surged by 56.3 percent year on year, climbing to US$2.5 billion from US$1.6 billion in H1 2024. This increase was largely led by a sharp rise in liquidation-related transactions, which jumped in value from just US$4 million to US$882 million. As of August 11, the third quarter has seen volume rise to 183 deals and value climb to US$2.6 billion, an 8 percent increase on the first three quarters of 2024 overall.

Regional fault lines

Distress is playing out unevenly across the continent, with Germany experiencing some of the deepest and most systemic pressures. Corporate bankruptcies in Europe’s largest economy reached their highest level in a decade in H1 2025, as companies contend with soft demand, rising wage costs, export competition from China and global uncertainty.

Alvarez & Marsal noted that 31.5 percent of German companies now have fragile balance sheets, up from 25.5 percent just two years ago, while the proportion of underperforming firms has grown to nearly 18 percent.

One notable transaction is the restructuring of Grover, the Berlin based tech rental platform. Creditors led by Fasanara Capital and M&G converted a large portion of their debt into equity in a court-sanctioned debt for equity swap, injecting US$34 million of fresh capital into the business and substantially diluting existing shareholders. The plan involves flipping senior secured loans into deeply subordinated obligations at the operating company level, with lenders also receiving equity and upside participation instruments, commonly referred to as “hope notes.”

In the UK, distress remains elevated despite a recent decline in insolvency filings in June. The largest deal of the year so far, Fidelity European’s acquisition of Henderson European Trust, was not a straightforward insolvency, but the US$842 million transaction followed shareholder unrest and reflected a liquidity-driven restructuring of the trust’s portfolio. With shareholders given the option of cash or shares, the deal illustrates the creative structures now being used to solve corporate distress, especially in financial services.

France has also seen a rise in distress-driven activity. Alvarez & Marsal’s latest data confirms increasing fragility among French companies, particularly in consumer-facing industries. Even legacy brands are no longer insulated from distress and are being targeted by entrepreneurs and family offices with turnaround expertise. Le Coq Sportif, a household sportswear brand, was recently sold through a court-led process to Franco-Swiss investor Dan Mamane, who committed to a €70 million (US$82 million) recapitalization and a relaunch of the company.

Sectoral stress points

Certain sectors have become clear hotspots for distressed dealmaking. Retail, consumer goods, leisure and hospitality continue to face headwinds from shifting consumer behavior, rising input costs and persistent margin pressure. Numerous analysts highlight retail as one of the most distressed sectors in Europe, with many legacy players struggling to keep pace with digital-first competitors and high operating costs.

The Le Coq Sportif sale exemplifies this trend, but it is far from isolated. In recent years, Italy has seen multiple distressed and special situations deals across retailers including department store brand Coin and fashion retailer Conbipel.

In the hospitality sector, Cedar Capital and Ares Management’s US$415 million rescue of a European lifestyle hotel portfolio reflects growing opportunism from investors seeking discounted assets in cyclical industries.

Industrial companies are also under pressure. Germany’s mid-sized “Mittelstand” industrial base is managing converging pressures. The country endured negative growth in 2024, with GDP stagnating in 2025. Growth in 2026 is forecast at just 0.7 percent, far below historical norms. German export-driven industries are contending with surging competition from Chinese producers that leverage state-backed overcapacity to flood global markets with lower-cost goods such as steel, machinery and automotive components.

At the same time, Germany’s auto sector, traditionally a jewel in the industrial crown, is facing mounting disruption. While electric vehicle adoption rises, with an estimated 25 percent of all car sales in Europe expected to be EVs in 2025, incumbents in Germany struggle to compete on cost against nimble Chinese manufacturers backed by subsidies and vertical supply chain integration.

One industry survey found that 67 percent of German auto suppliers expect a “significant number” of companies to exit the market amid this transition. Volkswagen, for example, is undertaking drastic restructuring, cutting 750,000 automobiles from production, reducing German headcount by 35,000 by 2030, and allocating €165 billion (US$191 billion) toward electrification and digitalization through 2030.

Outlook: A moving market

Distressed M&A is expected to remain a defining feature of the European market. Many of the drivers continue to affect business planning and investor confidence. In the UK, a rise in National Insurance contributions for employers is expected to further strain labor-intensive sectors. In Germany, weakness in manufacturing and the automotive sector continues to drive restructurings.

At the same time, a broad base of well-capitalized investors is positioning to take advantage of the dislocation. Private equity firms globally are sitting on around US$1.2 trillion in buyout dry powder, with a growing share allocated to special situations and turnaround strategies. For example, last year Bain Capital was reported to raise US$9 billion for its global special situations strategy.

This does not include the US$385 billion in available private credit powder, much of which is managed by hybrid capital providers prepared to manage both debt and equity positions. Last year, US firm H.I.G. Capital closed on US$1 billion for its credit and stressed situations Europe fund. Family offices, sovereign funds and companies are also showing increased appetite for distressed deals, particularly where they can leverage operational expertise to drive recovery.

Sectors undergoing structural change and regions with higher concentrations of vulnerable SMEs and mid-sized corporates, such as Germany, France and parts of Southern Europe, will remain key hunting grounds for companies and financial sponsors.

A bigger window of opportunity is opening for the right buyers. Those with the capital, risk appetite and operational sense see Europe as a market rich with businesses in need of repositioning, and trading at significantly discounted valuations. Distress may be rising, but so is the potential upside.

[View source.]