On July 28, 2025, the U.S. Department of Labor (“DOL”) issued some new interpretive guidance as part of a request for information (“RFI”) about pooled employer plans (“PEPs”) and an employer’s fiduciary responsibilities that arise when participating in one of these plans. Most notably, the RFI reminds employers that while they can mitigate their risk of ERISA fiduciary liability by having a PEP’s pooled plan provider assume full responsibility for selecting and retaining investment managers, the employer still must prudently select and monitor the pooled plan provider. The RFI also solicits information about prevailing market practices in order to determine the need for a potential safe harbor to promote greater utilization of these plans, which were created by the SECURE Act of 2019.

We have been actively involved in reviewing and evaluating PEPs for our clients since their inception, and we welcome this RFI as an important next step in the evolution of these plans, which, according to the DOL’s most recent statistics, cover over 618,000 participants and hold nearly $5 billion in assets. Last year, we released a two-part podcast series that highlights the positive aspects of PEPs for our plan sponsor clients and addresses some of the challenges associated with reviewing and monitoring PEPs (See here and here).

While it generally reaffirms the current understanding for how employers should evaluate PEPs and pooled plan providers, this guidance (and any future DOL pronouncements that derive from it) should help spur the proliferation of these plans and facilitate innovation in terms of the kinds of investment options they offer. Furthermore, with the imminent release of the Trump Administration’s executive order on expanding 401(k) plan access to private equity and other alternative investments, it is possible that we will see a number of PEPs that provide exposure to these asset classes in the near future.

Brief Overview of PEPs

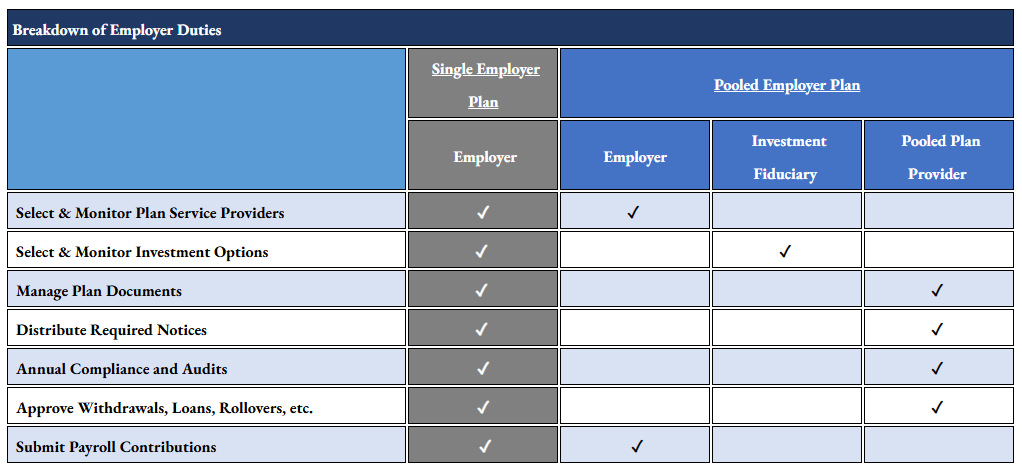

The RFI begins by providing a general description of the ERISA framework applicable to PEPs and the role of the pooled plan provider. Congress’s intent in creating these plans was to give employers—particularly, small employers—an efficient retirement savings vehicle for their workers with reduced administrative burdens and diversified investment lineups at a lower cost than small single employer plans could likely negotiate on their own. This is possible because when an employer participates in a PEP, it is able to (i) outsource, to the pooled plan provider, many of the administrative and fiduciary duties that come with sponsoring its own plan and (ii) take advantage of the lower service provider fees and costs associated with day-to-day plan administration. The chart below compares the various fiduciary roles and responsibilities of a traditional single employer plan versus a PEP.

Investment Selection and Management Guidance

The RFI next describes some of the common elements of the largest PEPs based on the DOL’s review of the plans’ Form 5500 filings, including, how nearly all of the largest PEPs offer target date funds (“TDFs”), and most offer limited investment lineups that would be designed to be accepted in their entirety by participating employers. The RFI also notes how in reviewing the largest PEPs, the DOL encountered a diversity of business models and kinds of employers these plans serve. These findings demonstrate the versatility of PEPs and how employers of various sizes and circumstances have joined them in the last few years.

The RFI then provides some interpretive guidance for PEP investment selection and management. As noted above, PEPs allow employers to shift the majority of their standard ERISA fiduciary responsibilities (e.g., monitoring the menu of investment options, management of retirement plan administration and investment management) to the pooled plan provider and any ERISA Section 3(38) investment managers the provider selects.

The RFI makes clear that if a pooled plan provider, as named fiduciary, were to appoint an investment manager, the manager would be responsible for the prudent investment and management of the plan’s assets—not the participating employers. Moreover, in these circumstances, neither the participating employers nor the pooled plan provider would be liable for any acts or omissions of the investment manager, except for any potential co-fiduciary liability under ERISA Section 405(a). According to the DOL, “the risk to participating employers of fiduciary liability could be minimized greatly if the pooled plan provider, as named fiduciary, expressly assumed full responsibility for, and exercised sole discretion and judgment in selecting and retaining the manager…[i]n these circumstances, fiduciary liability of participating employers would be minimized because the pooled plan provider assumed full responsibility for selecting and retaining the investment manager. This means the pooled plan provider has the duty to directly monitor the investment manager. Participating employers, in turn, must prudently monitor the pooled plan provider.”

Guidance for Choosing a PEP

The RFI also provides a series of relevant questions for employers (with a focus on small employers) to consider in order to prudently select a PEP and its pooled plan provider. Some examples include:

- the experience and qualifications of the pooled plan provider (the quality of the pooled plan provider’s services, customer satisfaction, prior litigation or government enforcement matters, and whether the provider is registered with the DOL as is required by law);

- whether the PEP will be able to offer economies of scale (how many employers and participants are in the plan and what is the total amount of the PEP’s assets);

- understanding the PEP’s fees (breakdown by service of all the fees and expenses associated with joining the PEP, breakdown by service of how much the pooled plan provider (and any affiliate) gets paid and who approves these fees and expenses, whether the pooled plan provider receives any compensation from third parties in connection with the PEP and whether it uses the data from participant accounts for cross-selling activities); and

- understanding the PEP’s investment options (the number of fund options, whether they are diversified, how they perform relative to their benchmarks, whether they have materially different risk and return characteristics, who selects the funds on the menu and how often their choices and process are reevaluated, what is the default investment for participants and whether the PEP has TDFs);

Request for Information; Next Steps

The RFI concludes with a series of inquiries as to what additional guidance would be needed to help promote employers’ wider participation in PEPs. For example, this section asks about the necessity for a new prohibited transaction exemption to address the unique conflict-of-interest scenarios that arise with these plans (for example, if the pooled plan provider utilizes an affiliated investment manager, or the PEP offers investments in which the pooled plan provider holds a financial interest). Other questions pertain to (i) PEP marketing and distribution processes, (ii) the challenges that arise in the corporate transaction context when a target company belongs to a PEP; (iii) revenue-sharing arrangements that offset the costs of recordkeeping or other plan services; and (iv) whether PEP vendors also offer model single employer plans and how they determine which option to recommend to employers.

The feedback the agency receives from the RFI will help it assess whether to issue a regulatory safe harbor to ensure participating employers and pooled plan providers are satisfying their fiduciary responsibilities under ERISA. The scope of any future safe harbor will likely focus on, among other things, the independence of the investment managers retained by the pooled plan provider, the types of investment products a PEP offers (including any issues that might arise by utilizing collective investment trusts and TDFs) and what disclosures should be provided to participating employers.

This RFI is a positive development in the emergence of the PEP as a key player in the retirement plan marketplace. Future guidance should hopefully provide additional clarity for participating employers and pooled plan providers as to how a PEP can be operated in compliance with ERISA. That said, for an employer that is considering whether to join a PEP, this RFI reiterates how critical it is to have a prudent decision-making process in place, as well as the need to be able to monitor and benchmark on an ongoing basis a PEP’s fees and investments once the employer has joined the plan.