Against a remarkably volatile macroeconomic backdrop, US and European high yield bond markets recorded conspicuous year-on-year declines in issuance during the first quarter of 2025.

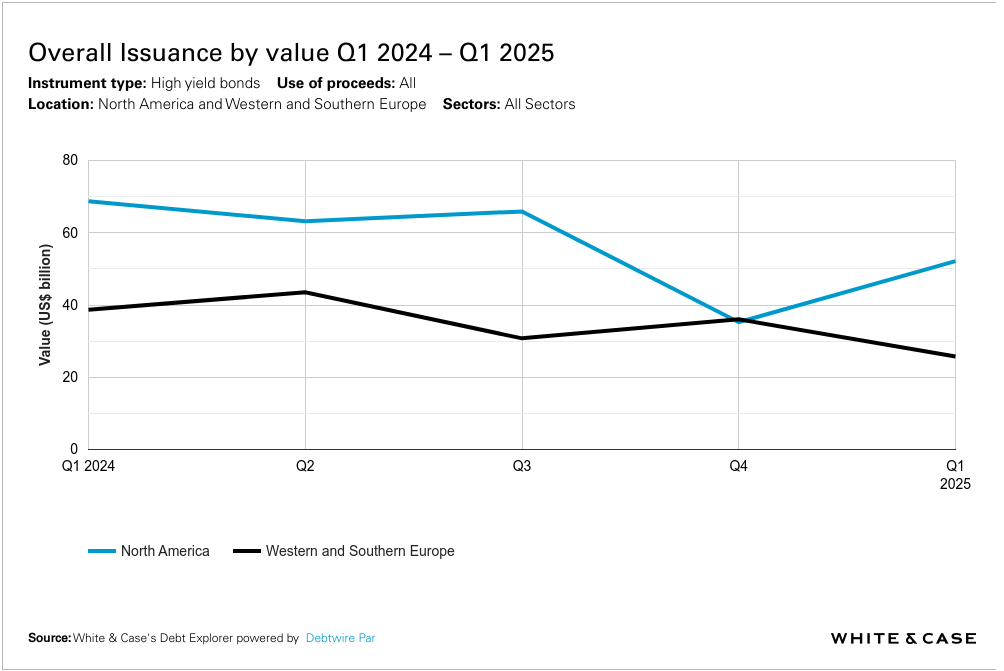

US high yield bond issuance totaled just under US$52.2 billion, down 24% compared to the US$68.7 billion worth of issuance logged in Q1 2024. However, US issuers can take some solace in the fact that issuance was up quarter-on-quarter, increasing by 48% relative to the US$35.3 billion of issuance recorded in the closing quarter of 2024.

Meanwhile, in Europe, year-on-year issuance dropped 34%, from US$38.7 billion in Q1 2024 to US$25.7 billion in Q1 2025. The latter figure also represents a quarter-on-quarter decline of 29%, from just over US$36 billion in Q4 of last year.

However, the overall year-on-year dips in the US and European activity levels were not mirrored in the APAC (excl. Japan) region. In Asia, high yield issuance volume recorded strong gains over the same period last year, more than doubling from US$2.5 billion in Q1 2024 to US$5.6 billion in Q1 2025. Issuance in the region has improved as the fallout from a liquidity crisis in the Chinese real estate market has to a large degree settled, with defaults trending down and investor sentiment improving.

Sentiment shifts in the US

Elevated yields continued to temper new high yield issuance in the US, with investor sentiment becoming more risk-sensitive over the course of the first quarter. Average bond yields tracked higher in the quarter compared to those reached at the same point in 2024, with margins for single-B and double-B notes coming in at 8.3% and 7.3%, respectively, according to Debtwire.

The announcement by US President Donald Trump on April 2nd of far-reaching tariffs put additional pressure on new issuance activity, with investors’ risk sensitivity to US high yield debt intensifying in the face of rising global trade tensions and supply-chain uncertainty. According to Bloomberg, several high yield deals were postponed or pulled from the market entirely following the announcement.

On a positive note, US high yield has demonstrated remarkable resilience—the rate of loan defaults remains mild, according to Debtwire, and in fact, eased slightly during the first quarter, dropping to 5.2% in February from January’s 5.3%. Economic disruption and trade tensions could have an adverse impact on high yield default rates throughout the rest of the year, but for now, the market appears to be holding steady.

Maturity wall looms over European market

High yield bond yields have remained stubbornly high in Europe, barely shifting over the past 12 months to an average of 6.78% through Q1 2025.

With yields elevated, refinancing activity in Europe—a primary driver of issuance last year—almost halved year-on-year from US$24 billion in Q1 2024 to just under US$12.3 billion in Q1 2025.

The drop in refinancing through Q1 is a major concern for issuers and investors. Over the past five years, high yield refinancing issuance in Europe has averaged €40.2 billion per year, according to Debtwire. However, the maturity wall for the next five years averages €83.2 billion per year. Meeting this refinancing demand will be challenging, especially if trade-related tensions exacerbate market uncertainty.

Indeed, the US tariff announcement in early April took a toll on the European market. The iTraxx Crossover, an index tracking around 50 European issuers with non-investment grade credit ratings, spiked 47 basis points following the announcement. This pushed the index to the highest levels seen since November 2023, with issuers in the chemicals, automotive and real estate sectors particularly exposed.

APAC uplift

Even though economies in APAC (excl. Japan) have also faced heightened risk during the course of 2025, high yield markets in the region were able to post year-on-year gains in Q1.

Asia’s high yield markets have stabilized as the impact of China’s real estate liquidity crisis starts to fade. Spreads have narrowed, allowing issuers to raise capital at lower cost, but the market also continues to present higher yields than other major credit markets. This has made Asian high yield assets especially attractive to investors, according to PineBridge Investments. Expectations of declining default rates amid a recovery in China’s property sector have also helped draw investors back to the market. For instance, in February 2025, Greentown China Holdings Limited, one of the leading property developers in China, issued US$500 million of 8.45% senior guaranteed notes due in 2028 to refinance certain of its then existing bonds. It marked Greentown’s first return to the public debt market since its last issuance in January 2022, and it was the first large-scale debt offering by a major Chinese real estate enterprise since 2023.

The APAC (excl. Japan) market will not be immune to higher US tariffs, with China, South Korea and Singapore all potentially exposed to major trade shocks. Other export-driven economies, such as Indonesia, Malaysia and Vietnam, will also face disruption, although the impact on these countries may be cushioned by the ongoing diversification of international supply chains outside of China, according to PineBridge. Meanwhile, the outlook for the Indian economy remains bullish, with domestic consumption and high business confidence presenting positive signals for credit markets, according to PineBridge.

Asian dollar-denominated bonds are also relatively insulated against tariff risks in the sense that few issuers of these bonds are export-focused. Additionally, the market has become more diversified in the wake of China’s real estate crisis and is less reliant today on that country’s property sector to drive issuance and returns.

International high yield markets went down diverging tracks in Q1 2025: the US and Europe faltered under high yields and rising trade tensions, while APAC was able to find its footing amid easing defaults and robust investor appetite. But as refinancing pressures build and geopolitical volatility casts a pall over the world economy, the path ahead for high yield markets remains uncertain.

[View source.]