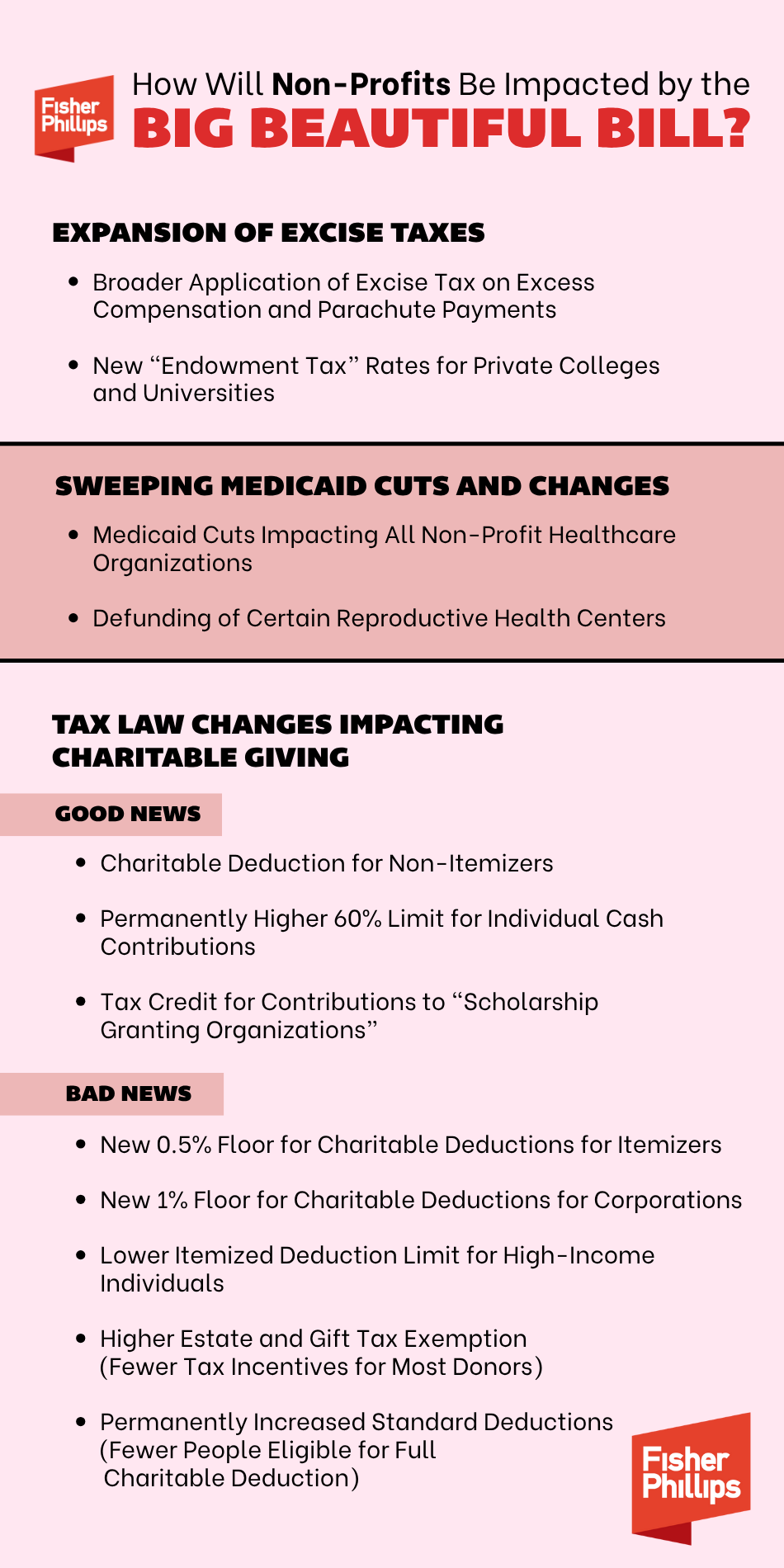

President Donald Trump signed a massive budget bill last month – the “One Big Beautiful Bill Act” (OBBBA) – and it significantly impacts non-profits and tax-exempt organizations. While some of the new changes may be beneficial, many others will increase financial and compliance burdens for your organization. Here’s an overview of the OBBBA’s impact on non-profits – including the good, the bad, and the ugly.

Expansion of Excise Taxes

1. Broader Application of Excise Tax on Excess Compensation and Parachute Payments (OBBBA Section 70416)

The definition of “covered employee” for purposes of the excise tax rules under Internal Revenue Code (IRC) Section 4960 will soon be significantly expanded.

- Quick Background. Since the 2018 tax year, “applicable tax-exempt organizations” (ATEOs), including 501(a)-exempt organizations, generally have been required to pay a 21% excise tax on remuneration in excess of $1 million and on any “excess parachute payment” (certain payments upon a separation of service that exceed a specified “base amount”) paid by the ATEO to any employee (or former employee) who is (or who was, during any preceding tax year in 2017 or later) one of the five highest paid employees for the taxable year.

- What’s Changing? Starting with the 2026 tax year, ATEOs must pay the 21% excise tax on remuneration in excess of $1 million and excess parachute payments paid, during the applicable tax year, to any current or former employee of the ATEO or a predecessor.

- Current Exceptions Will Remain. For example:

- “Remuneration” will continue to exclude payments to licensed medical professionals, including veterinarians, for performance of medical or veterinary services.

- “Excess parachute payments” will continue to exclude payments made to individuals who are not “highly compensated employees” (HCEs) under IRC Section 414(q), such as 5-percent owners and employees who earned above the HCE threshold ($160,000 in 2025) in the preceding year.

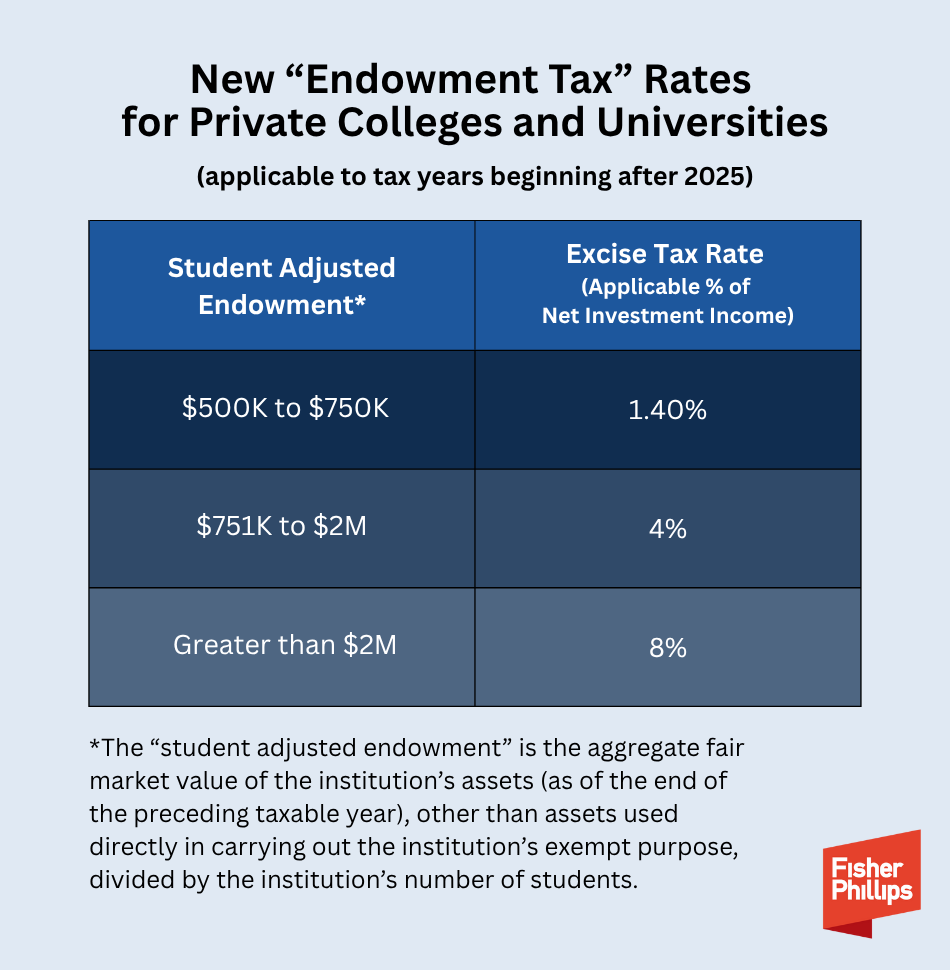

2. New “Endowment Tax” Rates for Private Colleges and Universities (OBBBA Section 70415)

Starting in the 2026 tax year, certain educational institutions will owe higher excise taxes on their net investment income.

- Quick Background. Since 2018, certain educational institutions have been required to pay an excise tax equal to 1.4% of the institution’s net investment income for the taxable year.

- What’s Changing? Effective January 1, 2026, the 1.4% flat excise tax rate will be replaced by a progressive tax rate (see chart below) that reaches as high as 8% for “applicable educational institutions” with a student adjusted endowment exceeding $2 million. In addition, “net investment income” will include certain student loan interest income and federally-subsidized royalty income.

- “Applicable Educational Institutions.” Under the amended IRC Section 4968, the excise tax on net investment income will be imposed on eligible educational institutions that have:

- at least 3,000 tuition-paying students during the preceding taxable year (note: this is an increase from the current threshold of 500 tuition-paying students);

- more than 50 percent of their tuition-paying students in the U.S.;

- a student adjusted endowment of at least $500,000; and

- no relation to State colleges and universities.

Sweeping Medicaid Cuts and Changes

1. Medicaid Cuts Impacting All Non-Profit Healthcare Organizations

The OBBBA contains various provisions that would massively impact the healthcare industry, including a reduction in federal Medicaid spending over a decade by an estimated $911 billion. According to this Nonprofit Quarterly article, nonprofit healthcare organizations will be hit hard by the Medicaid cuts: “In recent months, nonprofit healthcare organizations have finally begun to recover from the impact of the COVID-19 pandemic, but Medicaid cuts could reverse this progress, as more patients would be unable to pay for their care.”

2. Defunding of Certain Reproductive Health Centers (OBBBA Section 71113)

Section 71113 of the OBBBA blocks certain prohibited entities from receiving federal Medicaid funding through July 4, 2026. A “prohibited entity” means an entity – including its affiliates, subsidiaries, successors, and clinics – that, as of October 1, 2025:

- is a 501(c)(3) tax-exempt organization;

- is an essential community provider that is “primarily engaged in family planning services, reproductive health, and related medical care”;

- provides for abortions (excluding abortions in cases where the pregnancy is the result of rape or incest, or where a woman suffers from a physical disorder, injury, or illness that would, as certified by a physician, place the woman in danger of death unless an abortion is performed); and

- received more than $800,000 in Medicaid reimbursements during fiscal year 2023.

Note, however, that Section 71113 is under challenge in several ongoing lawsuits:

- Planned Parenthood’s Lawsuit. In a July 7 complaint filed in a Massachusetts federal court, the organization claimed that the provision was an unconstitutional bill of attainder because its “clear purpose” is to “categorically prohibit health centers associated with Planned Parenthood from receiving Medicaid reimbursements” and therefore to “punish them for lawful activity, namely advocating for and providing legal abortion access wholly outside of the Medicaid program and without using any federal funds.”

- For now, a court order is blocking the federal government from enforcing Section 71113 against any member of Planned Parenthood. After initially granting Planned Parenthood a temporary restraining order (which expired July 21) followed by a partial preliminary injunction, US District Judge Indira Talwani issued a full preliminary injunction on July 28 blocking the federal government from enforcing Section 71113 against any member of Planned Parenthood. The court found that Planned Parenthood and its members are “likely to establish that Congress singled them out with punitive intent and have therefore shown a substantial likelihood of success on their bill of attainder claim.”

- The Trump administration is appealing this decision to the 1st Circuit Court of Appeals.

- Other Lawsuits

- Maine Family Planning, a non-profit that operates 18 sexual and reproductive healthcare centers throughout Maine, is also challenging the constitutionality of Section 71113 in federal court. The judge has not yet issued a ruling regarding the non-profit’s request for immediate relief (the initial complaint was filed on July 16).

- At least 22 states (plus D.C.) are also suing the Trump Administration over Section 71113. In a complaint filed on July 29, the Democratic-led states brought the action to “avoid being compelled to participate in Congress’s unconstitutional conduct.” According to the filing, Section 71113 “will force Plaintiff States either to use states funds to keep Planned Parenthood health centers operating and forgo matching federal funds, or exclude the Planned Parenthood health centers from any state Medicaid program and lose critical healthcare infrastructure.” This case is still playing out in a Massachusetts federal court.

Stay tuned for updates related to these lawsuits.

Tax Law Changes Impacting Charitable Giving

Good News: Changes That Encourage Charitable Giving

Below are three changes under the OBBBA that will incentivize taxpayers to give more to non-profits and potentially increase the amount of donations your organization receives (though other OBBBA changes will do the opposite – see the “Bad News” section below).

1. Charitable Deduction for Non-Itemizers (OBBBA Section 70424)

For tax years starting in 2026 or later, individuals who do not elect to itemize deductions on their federal tax returns will be allowed to deduct charitable contributions of up to $1,000 (single filers) or $2,000 (joint filers). Gifts made to donor-advised funds, supporting organizations, or private foundations do not qualify for this new universal deduction.

2. Permanent 60% Limit for Individual Cash Contributions (OBBBA § 70425)

The Tax Cuts and Jobs Act of 2017 (TCJA) increased the deduction limit for charitable cash contributions made by individuals to qualifying organizations from 50% to 60% of the taxpayer’s contribution base (generally, their adjusted gross income) for the taxable year. This provision was set to expire after 2025, but the OBBBA made it permanent.

3. Tax Credit for Contributions to “Scholarship Granting Organizations” (OBBBA Section 70411)

For tax years starting in 2027 or later, a new tax credit of up to $1,700 (subject to reductions based on similar allowable credits on state tax returns) will be available to US citizens and legal residents who make a cash donation to any 501(c)(3) organization that qualifies as a public charity and meets specified requirements, including using the donation to fund scholarships for eligible students and their qualified elementary or secondary education expenses.

Bad News: Changes That Discourage Charitable Giving

Below are five changes under the OBBBA that will, starting in the 2026 tax year, reduce the federal tax incentives for charitable giving and potentially decrease the amount of donations your organization receives.

1. New 0.5% Floor for Itemizers (OBBBA Section 70425)

Individual taxpayers who itemize will be allowed to deduct charitable contributions only to the extent the aggregate of such contributions exceeds 0.5% of their adjusted gross income. Further, contributions that are not allowed to be deducted due to the new floor may be carried forward only from years in which the floor is exceeded (and will be subject to other carryover rules added by the OBBBA).

2. New 1% Floor for Corporations (Section 70426 of the OBBB Act)

Corporations will be allowed to deduct charitable contributions only to the extent that the aggregate of such contributions exceeds 1% of the taxpayer’s taxable income for the taxable year. The existing 10% ceiling will remain, but the new rules will permit contributions disallowed as deductions due to the ceiling to be carried forward for up to five years, subject to additional carryover rules. Further, contributions disallowed as deductions in a certain tax year due to the new 1% floor may be carried over only if the corporation’s contributions exceeded the 10% ceiling for such tax year.

3. Lower Itemized Deduction Limit for High-Income Individuals (OBBBA Section 70111)

The value of each dollar of all itemized deductions (including for charitable contributions) will be capped at $0.35. This 35% cap will be a negative change for individuals in the 37% tax rate bracket who are currently subject to a 37% cap.

4. Increased Estate and Gift Tax Exemption (OBBBA Section 70106)

The TCJA temporarily doubled the basic exclusion amount for federal estate and lifetime gift tax exemption purposes, but that increase was set to expire after this year. The OBBBA permanently increases this basic exclusion amount to $15 million for single filers ($30 million for joint filers) for estates of decedents dying, and gifts made, in 2026. The exemption amounts for future years will be subject to an annual cost-of-living adjustment.

5. Permanently Increased Standard Deductions (OBBBA Section 70102)

The TCJA’s significant increase to the standard deduction was set to expire after this year, but the OBBBA locks it in and increases it further. For example, for the 2025 tax year, the standard deduction is $15,750 for single filers and $31,500 for joint filers.

Conclusion

Non-profits must regularly evaluate how legal changes could impact their funding, budgets, and compliance obligations. Now is a critical time for your executive leadership, board of directors, and other key players to assess how the OBBBA’s sweeping changes impact your organization and determine next steps.