Investors in the Middle East have good reason to be optimistic. Despite ongoing tensions and conflicts in the region, economic growth prospects in many countries are improving. The International Monetary Fund expects GDP in the Middle East and Central Asia to grow 3.4 percent this year, up from 2.4 percent in 2024, and is forecasting 3.5 percent for 2026. In Saudi Arabia, it predicts 3.6 percent and 3.9 percent growth in 2025 and 2026.

The positives are numerous. The region’s powerful and sizeable sovereign wealth funds (SWFs) continue to invest heavily—and not only in the petrochemicals sector, now that accelerating digital transformation is creating new opportunities. Regulatory reforms aimed at delivering greater transparency and improved governance are boosting capital markets, while the Gulf Cooperation Council’s pursuit of free trade agreements, including with the UK, provides further support.

Moreover, despite the region’s ongoing conflicts, there has so far been only a modest spike in oil prices. Middle Eastern central banks remain relatively relaxed about inflation, with many cutting interest rates in line with their Western counterparts, creating benign conditions for investment.

Middle Eastern deals

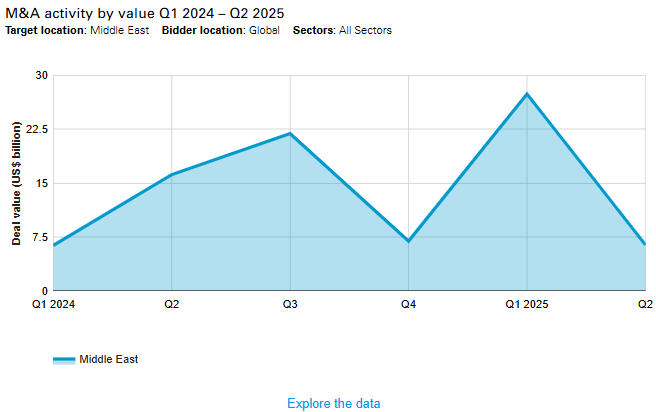

Against this backdrop, the Middle East is experiencing a strong uptick in M&A activity, particularly in terms of overall value. The first half of 2025 saw 227 deals worth a collective US$33.8 billion, compared to only US$22.5 billion spread across 260 deals in the same period last year. At the time of writing (August 22), this year’s value had jumped to US$78 billion, outstripping total value for all of 2024.

This spike in value is not just down to more megadeals. M&A activity in the Middle East is also now broadly based, with significant transactions taking place in industries including technology, financial services and consumer, as well as in energy, the region’s traditional power base.

Notably, Middle Eastern acquirers are also becoming significant players on the global M&A stage, as SWFs and other investors flex their financial muscles and look to diversify beyond regional oil and gas holdings. Outbound M&A activity totaled US$49.5 billion in H1, ahead of the US$45.8 billion seen in all of 2024.

Many of these drivers have coalesced around three countries in particular: Saudi Arabia and the United Arab Emirates account for a significant proportion of overall dealmaking, while Qatar is also fast becoming an important center for M&A activity.

M&A in Saudi Arabia

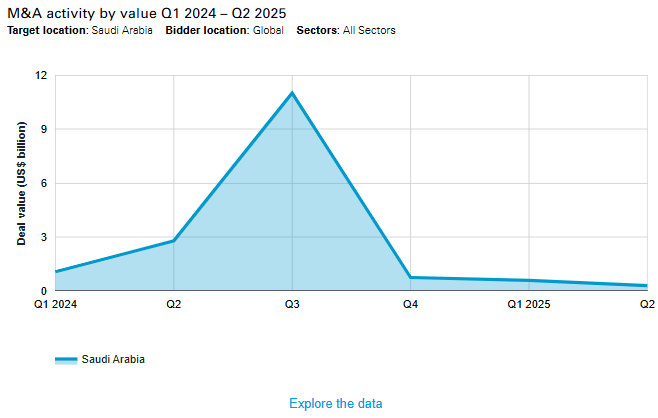

In Saudi Arabia, the first six months of 2025 saw 21 deals valued at US$850 million, down year on year from 30 deals worth US$3.8 billion. The third quarter, however, has seen a spike in deals, with year-to-date value rising to US$12.8 billion by August 22.

This is largely down to two deals, namely Saudi Aramco’s US$11 billion lease-and-leaseback deal for the Jafurah Midstream Gas Company, which involved selling a 49 percent stake to a consortium led by Global Infrastructure Partners, and the US$667 million bid from Dubai-headquartered family business Al-Futtaim for a 49.9 percent stake in Saudi Arabia’s Cenomi Retail, owned by Fawaz Abdulaziz Alhokair Co.

Saudi Arabia’s economic landscape remains extremely supportive of dealmaking. The IMF’s projections for a sharp acceleration in GDP growth reflect the strong performance of the country’s non-oil sectors. Inflation remains low in the country, easing the way for supportive dealmaking.

The government’s Vision 2030 blueprint for broadening Saudi Arabia’s economy also continues to drive investment, both from within the Middle East and beyond. The plan envisages a major diversification from oil into new industries built on technology and innovation, with a number of new economic zones already in place throughout the country.

The kingdom is also focusing on greater sustainability, emphasizing the importance of renewable energy. The government’s target is to source at least 50 percent of power from renewables by 2030. Financial markets are also undergoing reforms, with the Saudi Exchange opening up to foreign investors.

Saudi Arabia’s focus on diversification is changing the shape of its M&A market. Where dealmaking was once dominated by the energy sector, activity is now much more broadly based.

For example, the biggest transaction of the first half was in the tech industry, where Elm Co agreed to pay US$906 million for Thiqah Business Services. Digital transformation specialist Elm sees Thiqah as key to broadening its value proposition.

Meanwhile, the second-biggest deal was in the consumer sector and Almarai acquire Pure Beverages Industry Co. Pure Beverages, a bottled water company best known for its Ival and Oska brands, enables Almarai to expand beyond its existing range of dairy and food products.

Vision 2030 has the potential to drive further investment into Saudi Arabia, particularly as the Public Investment Fund, the country’s SWF, continues to play a key role directing support into critical sectors.

There is also scope for diversification to drive further outbound activity. Saudi Arabian acquirers spent US$7.7 billion on overseas targets during the first half of the year, beating 2024’s overall figure total by more than US$2 billion.

The technology, media and telecoms sector has been a particular focus for outbound activity, accounting for three of the five largest deals in the first half. One of them was Savvy Games Group’s US$3.5 billion acquisition of US gaming business Niantic, best known as the maker of the popular Pokémon Go. PIF-backed Savvy is growing rapidly, not least thanks to its hugely successful Monopoly Go game.

M&A in UAE

The UAE’s economy, boosted by its strong tourism, retail and energy sectors, is expected to be the Middle East’s top performer in 2025, with the IMF predicting GDP growth of 4 percent.

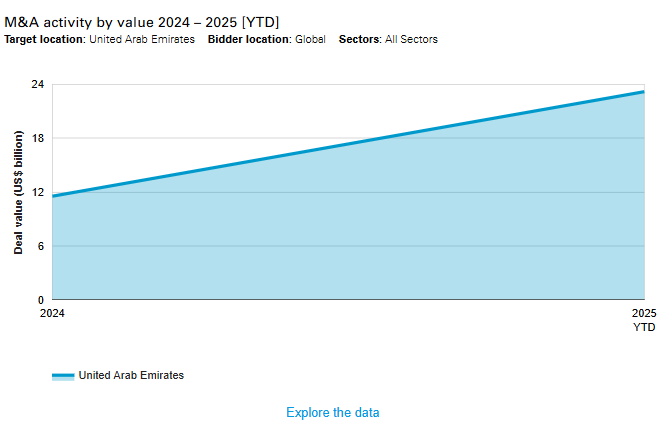

This broad-based strength is underpinning UAE M&A activity, particularly at the larger end of the market. While H1 deal numbers were down on the same period in 2024—64 transactions compared to 67—total deal value was more than double all of last year’s, at US$23.2 billion versus US$11.5 billion. By August 22, the figures were even healthier, with value rising to US$26.3 billion and deals increasing to 79.

Part of this success story is the government’s determination to diversify the country’s economy and industry. Its National Investment Strategy 2031 provides huge support for investment in the technology sector, spanning everything from artificial intelligence to advanced manufacturing.

Infrastructure has also received substantial backing, as has tourism. Given the UAE’s status as the world’s eighth-largest oil producer, traditional energy continues to loom large, though significant investment in renewable energy is accelerating. The UAE has already spent US$12 billion with the aim of boosting its renewables output to meet 32 percent of the country’s total energy needs by 2030.

The diversified nature of the country’s economy is mirrored by the leading M&A transactions seen so far this year.

The largest transaction of H1 was a more conventional UAE deal. It saw the Abu Dhabi National Oil Company and Austrian energy company OMV agree to combine their polyolefins businesses in a deal valued at US$16.5 billion. The arrangement will create a US$60 billion business, the world’s fourth largest in the sector.

By contrast, the second-biggest deal was in tech. Abu Dhabi-based G42, an AI and cloud computing specialist, is paying US$2.2 billion to increase its ownership stake in Khazna Data Centers, where it originally invested in 2020.

UAE’s diversification story could signal more deals to come as domestic and international investors explore opportunities created by the government’s efforts to move toward a more knowledge-based economy. Transport, infrastructure, construction and tourism are also part of that narrative.

UAE investors are also looking further afield. The US$18.7 billion megadeal that saw a consortium led by Abu Dhabi National Oil Company announce the intended acquisition of Santos, the Australian gas business, was one of a growing number of cross-border megadeals in the first half.

Total outbound activity rose to US$38.7 billion of deals in H1, compared with US$35 billion in all of 2024, and includes significant transactions in financial services, consumer and healthcare.

M&A in Qatar

Qatar’s growing prominence on the world stage, boosted by its hosting of the World Cup in 2022, has helped the country to continue broadening its economy. Like its Middle Eastern neighbors, Qatar is keen to diversify beyond oil and gas, particularly in sectors including retail, tourism and technology. Its support for the latter has seen Qatar rise 16 places on the WIPO Global Innovation Index since 2019. Real estate and manufacturing have also seen investment.

With Qatar now targeting 4 percent growth per year from its non-oil sectors by 2030, the country’s economic momentum is gathering pace. GDP growth reached 3.7 percent year on year during the first quarter of 2025, according to official statistics. The IMF is cautious about the rest of the year, predicting more gradual growth over 2025 as a whole, but it points to the favorable medium-term outlook.

Such optimism is seeing Qatar emerge as another busy hub of Middle Eastern M&A activity.

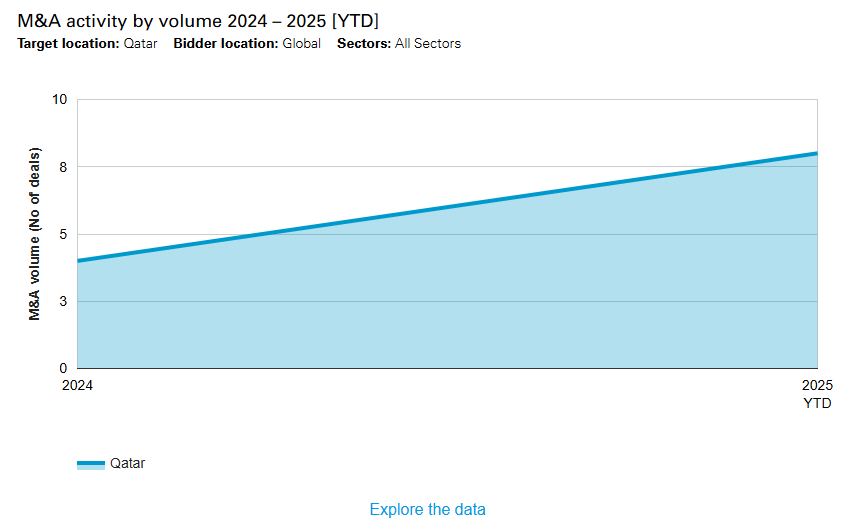

The first half of the year saw eight transactions in the country, double the volume of all of 2024. However, total deal value was only US$250 million, compared to US$350 million last year. That said, inbound dealmaking has made a strong start in the second half, reaching US$498 million by time of writing (August 22). The bulk of that value was down to the US$245 million transaction announced in July by the Saudi Arabian online food delivery platform Jahez, which is acquiring a controlling stake in Qatari logistics and e-commerce company Snoonu. The deal underlines Qatar’s potential to attract increasing M&A activity as the economy strengthens and diversifies.

There has also been a string of outbound investments, as the Qatar Investment Authority, the country’s SWF, and other Qatari investors look for diversification opportunities worldwide.

Those announced outbound deals—worth US$1.2 billion during the first half of 2025, compared to US$640 million in the same period of 2024—include Power International Holding’s US$1.1 billion acquisition of Mobile Telecom-Service in Kazakhstan.

Outlook

Building on a strong first half, dealmaking in the Middle East is widely expected to continue to show strength in the second half and beyond, as evidenced by a number of megadeals in the first months of Q3.

Domestic M&A activity is also an important part of the mix, with companies and SWFs across the region exploring new opportunities as governments seek to move away from dependence on oil and gas.

Outbound M&A should also benefit from this ongoing push for diversification. Access to capital in the Middle East continues to improve, driving expectations of further activity in sectors such as consumer and technology.

Indeed, with Middle Eastern governments now demonstrating growing confidence and strategic intent, optimism about M&A activity in the region is strengthening. The energy sector will continue to remain a key part of the dealmaking process, but a far broader range of industries are also now contributing to the momentum.

[View source.]