Key Takeaways:

- Come together: The alignment of interests between General Partners (GPs) and Limited Partners (LPs) can significantly improve value creation at the asset level. Additionally, it can foster enduring relationships, promote long-term commitment, and enhance governance.

- Be flexible: Flexibility on structures and fee arrangements is key for GPs to attract LP investments.

- Keep the receipts: A strong track record can enhance the GP's negotiating power with LPs.

GPs are increasingly exploring formalised co-investment structures in a bid to secure management fees and carried interest.

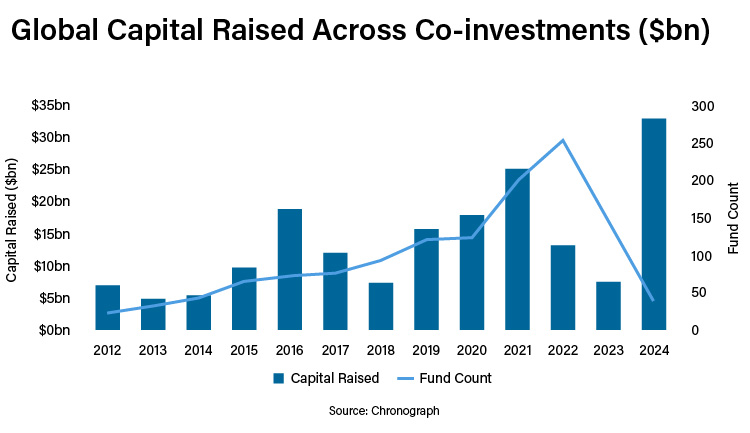

Co-investment activity has increased fivefold over the past two decades, hitting a record $33.2 billion in 2024, despite a muted dealmaking environment and investor liquidity constraints (Trends Shaping the Private Equity Co-Investment Landscape - Chronograph).

The advantages for both GPs and LPs are clear. GPs gain the flexibility to pursue high-potential deals while managing concentration limits; the opportunity to strengthen relationships with LPs, as well as access to fresh equity to support mid-life growth initiatives and acquisitions. Protracted fundraising challenges and the rising cost of debt have only encouraged GPs to seek co-investors who can underwrite deals in advance, providing greater funding certainty.

For LPs, co-investment offers a seductive number of advantages over traditional fund investment. There is no denying that the ability to secure co-investment with little or no attached economics, including the absence or reduction of management fees and carried interest, has become one of the most powerful draws for investors.

In addition, there is also the promise of greater control over deployment speed and diversification, which may allow investors to deepen relationships with their favourite managers.

Fee and Carry Arrangements

Over two-thirds of respondents to Private Fund CFO’s Fees & Expenses Survey 2024 do not charge any management fee on co-investment, while 42% charge no carry, with a further 39% charging carry at a reduced rate.

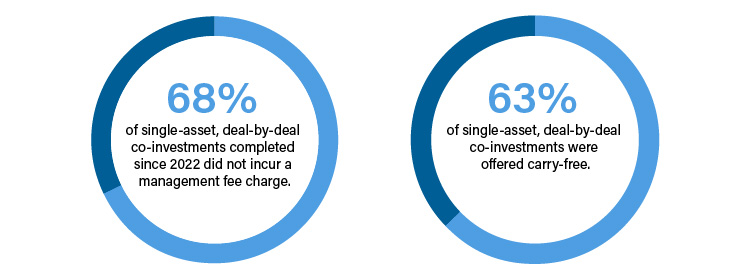

Ropes & Gray data tells a similar story. 68% of single-asset, deal-by-deal co-investments completed since 2022 did not incur a management fee charge, except for a nominal administration charge in a handful of cases, while 63% were offered carry-free.

Where management fees have been charged, particularly for direct co-investments from existing investors, they have typically fallen between 0.75% and 1%, with higher rates reserved for non-fund investors. Equally, where carried interest has been charged, it has typically been at a lower rate than the main fund at between 7.5% and 15%, with some managers opting for a performance-based tiered approach.

Meanwhile, almost half of co-investments in the past three years – 49% – have incurred neither fees nor carry in any form, according to Ropes & Gray data. As a result, the opportunity to blend down the cost of private equity and drive up returns to such an extent have become powerful drivers of LPs’ appetite for co-investments. It is not uncommon for investors to devote up to 30% of their private equity allocation to co-investment as a result.

Negotiating Positions

In response to the necessity of addressing the interests of LPs, GPs have begun to provide more adaptable co-investment frameworks, which in certain cases are tailored for individual LPs. Co-investors rarely invest directly alongside the main fund today.

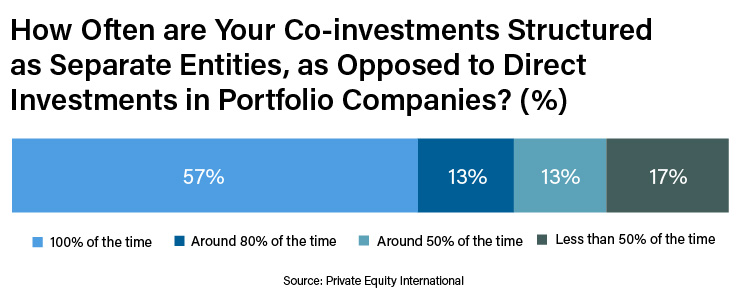

Private Funds CFO’s survey reveals that 70% of GPs usually or always structure co-investments as separate entities. These separate entities require work.

Co-investment funds need to be audited. Tax returns need to be filed, books and records maintained, and financial statements completed. Where no fees are charged, these costs are borne entirely by the GP.

GPs also increasingly believe that while co-investment offers important advantages to both parties, LPs are benefiting most from the arrangement. In some instances, GPs are increasingly looking to negotiate the economics in the co-investment they offer. This, in turn, is leading to an exploration of alternative co-investment structures.

Alternative Co-Investment Structures

The deal-by-deal co-investment remains the most common approach, given its flexibility concerning the size and time of investor allocations, as well as its potential for both parties to deepen relationships and access future deals.

LPs can choose which deals to invest in based on asset class, timing, and risk appetite. As a result, they can benefit from an improved portfolio customisation. However, it is relatively more difficult for a GP to secure economics with these structures. It is negotiated on a case-by case basis and often reduces the GP’s leverage in commercial terms.

There are alternatives, though. GPs are increasingly evaluating the relative advantages of establishing a committed co-investment programme, whereby investors commit upfront at the time of the initial fundraise, with separate co-investment vehicles then formed for each subsequent deal.

LPs generally prefer the flexibility offered by deal-by-deal investments and may insist on integrated economics in this scenario, given less capacity for managing their exposures and the need to ringfence capital for co-investment which may not ultimately be used. There is, however, a greater likelihood of the GP negotiating some level of management fee and/or carry.

GPs are also exploring a range of dedicated co-investment funds which will typically incur fees and carry, as well. These include overage funds – ten-year, closed-end structures – whereby all investors in the main fund agree to fund additional sums above their original commitment for the purpose of funding larger investments, with no fees charged on the amounts until capital is called. Capital is called more quickly into known transactions in this situation.

Other dedicated co-investment fund structures include annex funds, for later-stage or follow-on opportunities; industry or region-specific co-investment funds; pledge funds, where co-investors retain discretion to co-invest on a deal-by-deal basis and flex funds, where dormant commitments can be activated to invest alongside the main fund on an overflow basis.

Larger investors may also see advantages in creating a cross-platform separate account, including co-investment. This arrangement will typically result in some form of co-investment economics for the GP.

A Fairer Way Forward?

Clearly, there is no one-size-fits-all here. GPs and LPs will always have different priorities and requirements. The nature of the co-investment deals themselves also has a role to play.

Larger co-investors, particularly those with their own dedicated co-investment capital, are increasingly co-underwriting, doing their own diligence, helping form a view on price and taking a share of the risk.

In these scenarios, charging economics can be more challenging. Indeed, these investors are increasingly looking for greater governance and reporting rights at a portfolio company level, including asking for board seats. This represents a departure from the traditionally passive model of co-investment.

Equally, however, there are large numbers of investors that are not resourced to execute on co-investment in this way. There are opportunities for GPs to work with these LPs to explore alternative co-investment approaches that continue to offer the win-win that has driven the popularity of co-investment over many years, but which may also allow GPs to negotiate fairer share of the reward going forward.

This article is the latest in our series of European Private Capital Insights.