The Government has made the notification rules which determine the circumstances in which 2026 transactions will need to be notified to the Australian Competition and Consumer Commission (ACCC)1 under the new Part IVA of the Competition & Consumer Act 2010 (Cth) (CCA).2 The rules also detail the lodgement fees payable for notification, including significant fees based on deal value for “phase 2” transactions.3

The rules apply to deals coming into effect after 1 January 2026. If you have a transaction that may complete in 2026, you will need to consider whether it requires ACCC approval and if so, whether you can take advantage of the transitional rules to remove regulatory risk before 31 December 2025.

Here we explain the notification rules and some of the exemptions that may apply.

From 1 January 2026, businesses will need to notify the ACCC of any acquisition of shares or assets, that meet the notification thresholds. This includes the acquisition of units in unit trusts, interests in managed investment funds, or interests in land.

If the deal goes ahead without necessary approval, there will be steep penalties, and the deal will be automatically void.

Starting 1 July 2025, businesses can voluntarily notify the ACCC under the new regime. You will need to consider this option for deals that are expected to complete in 2026 and where you may not be able to rely on the transitional rules.

The new merger control regime applies to acquisitions of shares and assets. Assets are broadly defined. Section 51ABN of the CCA defines an asset to include ‘any kind of property, a legal or equitable right that is not property’ and acquisitions of shares and equitable interests in shares.

Later in this note we deal with specific exemptions to the obligation to notify in relation to acquisitions that do not confer ‘control’, the issuing or acquisitions of securities in entities regulated by Chapter 6 of the Corps Act (listed entities, unlisted entities with less than 50 members, and interests in registered managed investment schemes).

In addition, exemptions apply to an acquisition of shares arising from rights issues, authorised share buybacks and other financial markets transactions in circumstances where the acquisition satisfies or is consistent with certain Corps Act provisions.

Only include Australian revenues

The thresholds of A$200million and A$50million or A$500million and A$10million include only Australian revenues, being revenues that are determined in accordance with accounting standards and attributable to transactions or assets within Australia or transactions into Australia.

Australian revenues must be calculated for the:

- acquirer (the person who acquires the shares or assets);

- the acquirer’s “connected entities”;

- the target; and

- the target’s “connected entities” being directly or indirectly acquired.

Australian revenue is calculated as at the contract date being the date on which the contract, arrangement or understanding is entered into under which the acquisition is to take place.

Australian revenues are Australian gross revenues attributable to transactions or assets within or into Australia. The revenues are calculated in accordance with international and Australian accounting standards as at the most recently ending 12 month financial reporting period to the contract date.

Australian revenues includes “connected entities”

The Australian revenue of the principal party and the target include the Australian revenue of connected entities.

Connected entities include related entities and controlled entities.

The first test adopts the “related party” definition in section 4A of the CCA. A related entity to the principal party or the target includes: a holding company4; a subsidiary5; or another subsidiary of a holding company of another body corporate that is related to the principal party or target.

A controlled entity is a broader concept. It captures not just legal ownership, but practical control (including control together with one or more “associates”, within the meaning of Chapter 6 of the Corps Act). This second test adopts the definitions of “control” in section 50AA of the Corps Act and “associates” in Chapter 6 of the Corps Act. An entity controls another entity when it has the capacity to determine the outcome of decisions about the second entity’s financial or operating policies.

Control either alone or with “associates”

Particular care will need to be taken to ensure that the treatment of “associates” is appropriately considered – given the wide definition of associates under Chapter 6 of the Corps Act, this definition has the potential to capture revenue that might not otherwise be “consolidated” as part of a business’ typical internal reporting. For example, associates include entities within the same corporate group, counterparties to agreements for the purposes of controlling or influencing a third parties operations, and counterparties “acting, or proposing to act” in concert in relation to a third party. The practical implications of this are that:

- control will be aggregated at the group level (ie, where multiple group entities have a direct or indirect interest in the same entity, they will be aggregated together);

- joint venture agreements will need to be closely considered (ie, as they may be characterised as agreements regarding the control of the joint venture asset/company) to determine whether joint venture revenue needs to be assessed, even for relatively small minority interests; and

- voting agreements or even practical coordination with counterparties might make them an associate (eg, where a party has a small ownership interest but always votes with the 49% interest holder, that 49% interest holder might be considered an associate, and therefore together they would have joint control) and therefore the jointly controlled entity revenue might need to be assessed.

On the acquirer side, the connected entities test works both upwards and downwards from the principal party and will capture the revenue of other entities “connected” through the chain (ie, including parties that the acquirer owns/controls, is owned/controlled by or that it shares a common owner/controller with). However, the Australian revenue of the target’s “connected entities” is only included if they are being directly or indirectly acquired through the acquisition.

|

|

Warning! |

The “connected entity” test works both upwards and downwards through the supply chain and will capture the revenue of other entities “connected” through the chain. Great care will be needed to calculate revenues of “connected entities”, including whether there are any “controlled entities” in the supply chain by virtue of the wide “associate” definition. A failure to capture relevant revenues leading to a wrong decision to not notify a transaction may have serious consequences

How do I calculate Australian revenue when there are more than two parties to the acquisition?

More than two parties may enter into a contract, arrangement or understanding under which an acquisition or acquisitions may occur. For example, two parties may agree to separately acquire the assets of the target, or two parties may agree to acquire the assets of the target as an unincorporated joint venture. In these circumstances, if any one of the acquisitions satisfies a revenue threshold, all of the acquisitions need to be notified.

How do I calculate Australian revenue when I am buying assets?

Where the transaction concerned involves an acquisition of an asset, the Australian revenue “attributable” to the asset will need to be determined. The term “attributable” is not defined, however Australian and International accounting standards will assist. Where there is no revenue, the revenue for the threshold test will be zero. However, where there is revenue attributable to an asset but it is not reasonably practicable to determine it, the rules require that 20% of the market value be attributed to the revenue thresholds to understand whether notification is required.

For example, a principal party acquires a leasehold interest in a premises and will carry on its business at the leased premises. Some revenue is attributable to the leasehold interest, however it may not be reasonably practicable to determine the revenue attributable to it. Therefore, 20% of the market value of the leasehold interest (ie, the rent payable under the entire term of the lease) would be attributed as Australian revenue of the leasehold interest.

You will not be required to notify where the asset does not generate income or revenue, or where the asset otherwise falls within another exemption (for example, the ‘small acquisitions’ exemption where the revenue is less than A$2million).

Do I need to aggregate other ‘serial’ acquisitions?

In addition to including the Australian revenues of connected entities of the principal party and the target, the revenues associated with certain historic acquisitions (serial acquisitions) over the preceding three years by the principal party or a connected entity of the principal party will need to be included where:

- The revenues attributable to previous acquisitions of shares and assets are for businesses that are predominantly involved in the supply of the same, substitutable or otherwise competing goods or services of the target business.

- The combined revenue of those businesses acquired over the 3 years are A$50m or more for large business acquisitions or are A$10 for very large business acquisitions.

Revenues attributable to previous acquisition of shares or assets that are less than A$2 million (small acquisition test) and revenues where the shares or assets were not connected with Australia (revenues connected with Australia) do not need to be aggregated.

|

Warning!

|

The revenues of businesses that have to be aggregated under the three year serial acquisition provisions include revenues of businesses that both the principal party and its connected entities have acquired over time.

Are acquisitions of overseas shares or assets caught?

The notification thresholds apply to the acquisition of shares or assets connected with Australia. Shares and assets are connected with Australia when the entity in which the shares are held or the entity that has the asset carries on a business in Australia.

Businesses based predominantly overseas (such as tech and financial service companies) who make acquisitions of entities overseas that carry on business in Australia will be required to notify transactions, where the transaction value or combined revenues of the merger parties exceeds the relevant thresholds.

How do I calculate transaction values (A$250 million)?

The transaction value test of A$250 million is satisfied if the sum of market values of all shares and assets acquired as part of the contract, arrangement or understanding under which the transaction takes place is A$250 million or the consideration for all of the shares or assets acquired as part of the contract, arrangement or understanding under which the transaction takes place is A$250 million.

Exemptions from filing available for some interests in land

Acquisitions of interests in land exempt from notification in some cases

The following acquisitions of interests in land are not required to be notified:

- A legal or equitable interest in the land for the purpose of (1) developing residential premises, or (2) carrying on a business primarily of buying, selling, leasing or developing land.

- An interest that confers a right to develop land for any of the above purposes.

- An extension or renewal of a lease of the same land by the same party.

- A legal or equitable interest that relates only to a sale and leaseback arrangement.

Acquisitions of entities that only hold legal or equitable interests in land (as well as acquisitions of shares or units in such entities) are treated consistently with direct land acquisitions.

Only one notification is needed for an acquisition of the same land that occurs in multiple stages (for example, an acquisition of an equitable interest on signing, and later a legal interest on settlement). However, that exemption does not extend to an increased ownership interest in a parcel of land, such as moving from a 20% to 50% interest.

Purpose of ‘developing land’ exemption not available where land will be used for another commercial activity post-development

The availability of the exemption to filing where the primary purpose is to carry on a business primarily engaged in managing or developing land turns on the purpose of the land acquisition. The exemption is available regardless of whether the land is vacant or already developed, and even if ancillary or incidental services (such as property or facilities management, or concierge services) are provided by the developer.

However, the exemption does not extend to where the land will serve as a platform or location for operating other commercial activities. For example, a manufacturing company acquiring land to operate a factory would not be exempt from notifying the acquisition. That is because the primary purpose relates to operating the commercial business, not trading or developing the land itself.

|

Warning!

|

Businesses that acquire land or interest in land as an input to their commercial activities such as renewables projects, mining, data centres, port storage and terminals will now need to consider whether their transactions are notifiable to the ACCC.

Purpose of “developing residential premises” exemption is broader

The exemption for developing “residential premises” is cast by reference to GST legislation, and covers houses, apartments, townhouses, retirement villages, student accommodation, and other premises intended for residential purposes.

This exemption will extend to a developer acquiring land for the purpose of developing a retirement village or student accommodation, even if it then intends to operate a retirement or student accommodation business at the site. The exemption would not apply to any subsequent on-sale of the developed site or the business, however.

Lease renewal exception limited to the same land, but applies to substantive continuation

The exemption for lease renewals or extensions will not apply where it involves a new or expanded parcel of land, there is a change in the lessee party, or there is no continuous occupation of the land.

However, the exemption does extend to common contractual forms of lease renewals, including a new lease over the same land, exercising a contractual option to renew, signing of a renewal deed, and other common lease continuation practices such as surrender and regrant.

Additional requirements for Coles and Woolworths

Coles and Woolworths (Major Supermarkets) will need to notify acquisitions of legal or equitable interests in land where a supermarket business is operating or will operate on the site and:

- if the land has a commercial building upon it, the gross lettable area of the building is greater than 1,000 square metres; or

- if the land does not have a commercial building upon it, the land is greater than 2,000 square metres.

Extensions or renewals of existing leases are excluded from these requirements. However, where the land being acquired is adjacent to land already held by the relevant Major Supermarket, the existing land size is aggregated with the size of the land being acquired for the purposes of these rules.

Similar to the broader land provisions, the Major Supermarkets will need to notify these types of acquisitions when they first acquire a legal or equitable interest in the land.

When are acquisitions by financial providers caught?

There is an exemption that applies for acquisitions that are generally for the provision of capital, management of financial risk or facilitating of financial activities, as opposed to the acquisition of business operations. The exemption applies for acquisitions of shares or assets that are:

- debt instruments;

- debt interests in entities;

- asset securitisation arrangements;

- securities financing transactions such as repurchase agreements and securities lending;

- security interests (within the meaning of the Corps Act); and

- arrangements directly connected with these financial structures.

However, there are two exceptions where the exemption does not apply:

- where there is an acquisition of an equity interest, an acquisition that has the effect that a person will begin, or can begin, to ‘control’ the business; and

- for an acquisition of an asset, where the acquirer will in effect acquire all, or substantially all, of the assets of a business.

There is a further exemption for security interests that are taken or acquired in the ordinary course of financial accommodation on ordinary commercial terms.

The rules do not provide any guidance for how to apply the two exemptions to the provision of financial accommodation in the ordinary course when the terms of the security may confer control or a right to all or substantially all of the assets on default.

|

Warning!

|

Taking security interests that confer hybrid equity like rights may be subject to the notification obligations, if the financial thresholds are met and the exception to the exemption for lending in the ordinary course are not satisfied.

Exemptions for financial markets, clearing & settlement facilities and Corps Act securities

In addition, there are exemptions for acquisitions of shares arising from:

- rights issues and accelerated rights issues, including underwriting of those shares;

- authorised share buy backs;

- dividend re-investment schemes; and

- underwriting of fund raising where a disclosure document has been issued,

in circumstances where the acquisition satisfies, or is consistent with certain Corps Act provisions.

Also exempt are derivatives, except where that involves acquiring shares or assets which deliver “control”.

Additionally, acquisitions by operators of, or participants in clearing and settlement activities are exempt from notification requirements where these transactions legitimately arise in the ordinary course of clearing and settlement activities.

Additional exemptions to notification are in the CCA

Even in circumstances where an acquisition may satisfy the notification thresholds there are some key exemptions in the CCA.

Acquisition that does not confer control under a modified section 50AA test

An acquisition of shares (or units etc) that does not confer control within the meaning of a modified section 50AA Corps Act test (when control did not previously exist) is not required to be notified. Importantly, for the purposes of this assessment, the CCA modifies the test in section 50AA by excluding the operation of subsections 50AA(3) and (4), with the effect that you must consider, amongst other things, whether the acquirer will hold, jointly with a third party, the capacity to control.

|

Warning!

|

The control test for section 51ABS of the CCA is a different test to the control test used to calculate revenues of connected entities for the purpose of the threshold tests.

Acquisitions of shares giving 20% or less voting power in a Chapter 6 entity

An acquisition of shares in the capital of a body corporate of a Chapter 6 entity Corps Act (listed companies, unlisted companies with more than 50 members and registered listed managed investment schemes) that does not result in someone’s voting power in the body corporate increasing from:

- 20% or below to more than 20%; or

- from a starting point that is above 20% and below 100%,

is exempt from the obligation to notify.

Notification forms have been finalised

The Notification Determination has the final short and long form notification requirements for transactions which meet the notification thresholds.

To notify, you will need to provide the ACCC with considerable amounts of data and information. Access to clean data will be crucial for filling out the notification forms and providing the ACCC with necessary information.

If your acquisition is less likely to raise competition concerns you can provide a short form notification. You will need to provide:

- details of acquisitions over the previous three years where the targets were involved (directly or indirectly) in the supply or acquisition of substitutable or otherwise competitive goods or services;

- contact details for the top five closest competitors, top five largest customers and top five customers closest to the median customer spend;

- Australian revenue and market share information; and

- internal documents including transaction documents, supply or ancillary agreements conditional on the acquisition, audited financial reports and income statements, and organisation charts.

If you are filing a long form notification,6 the information requirements are more substantial and include providing:

- details of any recent entry into or exit from the market and information relating to potential barriers to entry;

- contact details for the top 10 closest competitors, top 10 largest customers and top 10 customers closest to the median customer spend;

- datasets or reports used by the parties to estimate or analyse its own and competitors’ market shares;

- papers that have been prepared by, for, or received by the Board or a Board Committee that assess or analyse the acquisition;

- papers that have been prepared by, for, or received by the Board or a Board Committee that describe or analyse competitive or market conditions, market shares, competitors or business plans in relation to the relevant goods or services;

- for horizontal acquisitions, details about how competition works;

- for vertical acquisitions, information and evidence about potential input or customer foreclosure; and

- for conglomerate acquisitions, information and evidence about potential foreclosure of competitors.

There is an additional form for parties applying for a public benefit determination. This requires you to provide information about potential public benefits and detriments as well as any relevant documents, including transaction documents that have not previously been provided to the ACCC.

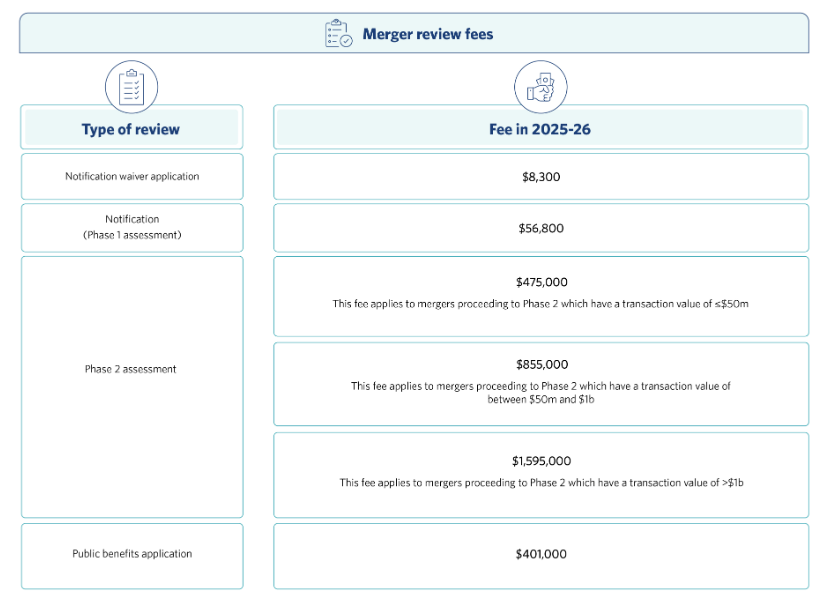

Filing fees

The Notification Determination prescribes the fees which notifying parties will incur at each stage of the ACCC’s review. These fees are connected to the value of the notifiable transaction and are set our below:

Acquisition register

The Notification Determination specifies the details regarding the notification to be included on the acquisition register. The acquisition register will be live from 1 July 2025.

Details that will be published on the register within one business day after the effective notification date of the notification are:

- the notifying / target party (name, identifying number, contact details) – this information will have been provided as part of a notification form;

- a non-confidential summary of the acquisition provided – this information will have been provided as part of a notification form; and

- details on timing – effective notification date, end of the determination period and the current stage of the notification (eg phase 1 determination period).

Additional details that will be published on the register, within one business day of occurrence, as the ACCC’s assessment progresses are:

- any extension to the determination period and a change to the current stage of the notification;

- a statement regarding any consultation occurring and the nature of the consultation;

- summaries of the notification waiver, extension of the determination period, notice of competition concerns and public benefit assessment (if relevant);

- copy of the ACCC’s acquisition determination (if any) plus statement of reasons; and

- notice of a phase 2 review (if relevant).

The ACCC has discretion to withhold or remove materials from the acquisitions register in limited circumstances, including if the material is commercially sensitive and has the potential to cause detriment to a party to the acquisition or a third party; is personal information within the meaning of the Privacy Act 1988, or could offend or unreasonably harm an individual. If materials are withheld or removed, the ACCC will publish a statement on the register, at the time, to that effect.

What’s next

We expect the Government may publish additional legislative instruments prior to 1 January 2026 dealing with several other aspects of the new regime including:

- details on the waiver process; and

- to clarify and potentially narrow the control exemption for notification of certain acquisitions of shares in a body corporate.

Recap

Australia’s new merger regime commences on a transitional basis from 1 July 2025 and officially commences on 1 January 2026. From 1 January 2026, all transactions which are caught by the notification thresholds must be notified to the ACCC.

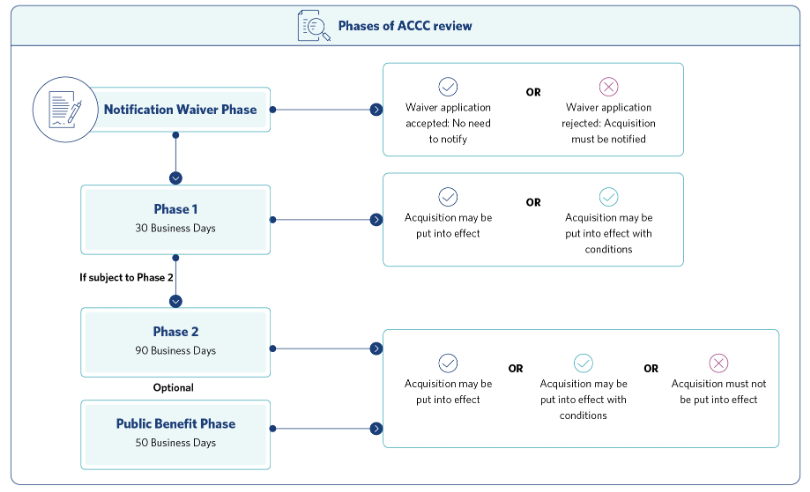

Once notified, the ACCC will commence a compulsory, staged review process, comprised of the following phases.