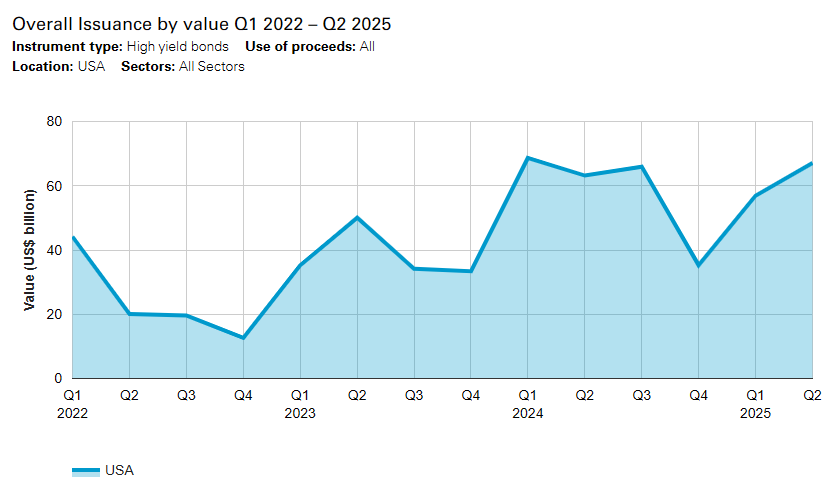

After a bumpy start to the second quarter, when tariff announcements inhibited issuance, US high yield bond activity rallied strongly, demonstrating the market’s resilience and maturity.

Total US high yield bond issuance for the first half of the year was down just 6% year-on-year, reaching US$123.9 billion. The market is well positioned for a steady second half after adapting swiftly to elevated trade tariffs and choppy stock markets.

Explore the data

Washington’s initial announcement on April 2 of plans to impose “reciprocal tariffs” on global trade partners saw US high yield issuance more than halve from US$18.4 billion in March to US$7.1 billion in April, according to Debtwire. But high yield markets bounced back in May and again in June, when monthly issuance hit US$32.4 billion—the best one-month total since 2021.

Dealmakers moved quickly to predict the potential impact of higher tariffs on company sales. As more company earnings reports were released following the initial tariff announcements, they allowed investors to draw a clearer picture of future earnings, and as a result, high yield markets accelerated.

Meanwhile, those issuers who opted to wait and see how the Trump administration would operate also returned to market toward the end of H1 2025. Much of this activity saw issuers make valuable progress on their refinancing plans and capital raisings to support long-term commercial objectives.

In another boon, investors have begun to pivot toward high yield bonds (which historically have performed better during economic cycles when interest rates are expected to fall), further fortifying the post-April rally in issuance.

Credit quality counts

The rebound in high yield issuance in June was driven by activity among higher-rated borrowers, reflecting investors’ appetite for credits that offer downside protection. Bonds rated “BB-” or higher generated almost 69% of US high yield activity during the first six months, according to Debtwire. Meanwhile, senior secured high yield issuance also accounted for more than two-thirds of issuance in June, reflecting investors’ continued focus on mitigating downside risk.

The resilience of US high yield issuance amid tariff turbulence is also a function of its evolution from a “junk bond” market into one comprised of stronger, better-quality issuers.

According to AXA Investment Managers, higher-quality BB-rated credits accounted for 38% of the US high yield market before the 2008 financial crisis—today they comprise 53% of the market, while lower-rated CCC issuers represent only 11%. The market’s more robust credit quality has translated into lower default risk, with default rates in the low single digits. In fact, in April of this year, the par-weighted 12-month trailing default rate of US high yield bonds fell to just 0.3%.

Nevertheless, for those investors open to taking on more risk, the US high yield market still has plenty to offer. As dealmakers have grown accustomed to tariff uncertainty over the past few months, more confident investors seeking higher yields have been willing to back lower-rated CCC issuers.

According to Bloomberg, CCC-rated bonds showed steady gains in July and outpaced investment-grade and higher-rated high yield bonds. This signals investors’ growing appetite to take on more risk in return for larger yields.

Short-term switch

Investors have also pivoted toward shorter-maturity high yield bonds. These offer investors more visibility on immediate financial risks. Bonds with shorter-dated maturities make it easier to filter out issuers at risk of short-term default and are less exposed to volatility in spreads.

In the current market, AllianceBernstein data shows that shorter-maturity high yield bonds—which typically provide lower yields than longer-dated bonds—are presently offering better yields than longer-dated issuance, providing investors with a highly attractive risk-reward balance.

Short-term bonds also offer issuers greater flexibility and shorter non-call windows compared to longer-dated bonds. This provides issuers with the scope to bring forward exit timelines, or to refinance in a more attractive rate environment, without incurring pre-payment penalties.

Adapting to change

The US high yield market has demonstrated remarkable resilience through this recent period of volatility. Rather than sit around and wait for conditions to improve, investors and issuers have shown their willingness to navigate near-term uncertainty and keep the market moving forward.

Issuers have responded by tailoring their collateral packages, maturities and pricing to dovetail better with investors’ priorities. Investors, too, have adjusted to the fluid macroeconomic backdrop, assessing each issuer on its own merits and negotiating security packages and interest rates accordingly, rather than taking a one-size-fits-all approach to underwriting.

After a brief pause, the US market has not just accepted the “new normal”—it has adapted and gotten back to business.

[View source.]