Contents

Executive Summary

I. Legislative and Policy Developments

II. Enforcement Overview and Trends

III. Merger Control Review and Enforcement

IV. Sectoral Competition Assessments

V. Practical Takeaways

Executive Summary

On June 7, 2025, China’s State Administration for Market Regulation (SAMR) released the 2024 Annual Report on Antitrust Enforcement (“Report”), providing a comprehensive overview of key legislative developments, enforcement activity, merger review, and administrative monopoly regulation over the past year. The Report indicates that China’s antitrust enforcement maintained a stable pace and policy direction in 2024, with sustained regulatory focus on sectors closely tied to public welfare and continued emphasis on procedural efficiency and compliance facilitation.

In terms of enforcement, SAMR initiated 17 new investigations into monopoly agreements and concluded 5 abuse of dominance cases, alongside 72 cases involving abuses of administrative power to restrict competition. The enforcement focus remained on classic types of conduct such as horizontal price-fixing, exclusive dealing, tying, and refusal to deal, particularly in sectors such as pharmaceuticals, energy, and public utilities. SAMR also continued to monitor post-penalty compliance by major platforms including Alibaba, Meituan, and CNKI, and employed soft tools such as compliance letters and administrative interviews to improve early-stage risk prevention and behavioral guidance.

On merger control, SAMR received 729 merger filings and formally accepted 643, of which 623 were cleared unconditionally and one was approved with remedies. Following the implementation of revised filing thresholds in 2024, the total number of filings dropped by 15% year-on-year, easing compliance costs for businesses. Over 90% of cases were reviewed under the simplified procedure, with an average formal review period after case acceptance reduced to 24.7 days.

The Report also highlights several emerging trends. Notably, SAMR launched ex officio reviews of transactions falling below the notification thresholds but potentially raising competition concerns. It also intensified post-clearance monitoring of conditional approvals, including initiating a formal investigation into NVIDIA’s acquisition of Mellanox. In parallel, 2024 saw China’s first court challenge against a merger control decision, marking the emergence of judicial review as a new avenue of relief in merger enforcement.

In addition, The Report reinforces SAMR’s ongoing emphasis on competition assessments across key sectors. Six industries—ticketing services, semiconductor materials, cloud computing, warehousing, new energy vehicle charging/swapping, and patent databases—were singled out for in-depth evaluation. These sectoral assessments aim to identify structural and behavioral risks and help shape future enforcement priorities and compliance expectations.

- Legislative and Policy Developments

In 2024, China continued to advance its antitrust legal framework through new legislation and the refinement of existing guidance, with a clear emphasis on improving regulatory clarity, promoting compliance, and addressing sector-specific risks.

In the area of merger control, the State Council revised Rules of the State Council on Declaration Threshold for Concentration of Undertakings in the early 2024, significantly raising the filing thresholds and leading to a 15% decline in the number of filing cases in 2024. In the end of 2024, SAMR issued the Guidelines on the Review of Horizontal Concentrations, which set out the analytical framework for assessing the competitive impact of horizontal transactions, with particular emphasis on the assessment of unilateral and coordinated effects, and offer clearer procedural expectations for notifying parties.

On the sectoral front, pharmaceutical enforcement remained a key focus. Building on earlier guidance for the Active Pharmaceutical Ingredient (API) sector, the State Council’s Antimonopoly and Anti-Unfair Competition Commission released the Antitrust Guidelines for the Pharmaceutical Sector, covering all types of drugs, detailing typical anticompetitive conducts and enforcement criteria, including for more complex or concealed practices. In the intellectual property sphere, SAMR issued the long-awaited Guidelines on Antitrust Issues Related to Standard Essential Patents (SEPs), clarifying the rights and obligations of SEP holders and implementers on FRAND negotiations, disclosure, licensing, and injunctive relief. The guidelines also provide analytical tools for assessing SEP-related conduct under monopoly agreement and dominance rules.

On the compliance front, the Antitrust Guidelines for Trade Associations were issued to guide trade associations to strengthen their development of anti-monopoly compliance. And the Antitrust Compliance Guidelines for Undertakings were updated to set out clearer expectations for companies to establish internal compliance systems and introduce a formal “compliance incentive” mechanism, which signals that a robust compliance program may be considered a mitigating factor in enforcement.

Finally, the State Council adopted the Fair Competition Review Regulation, the first administrative regulation dedicated to curbing anticompetitive government conduct. The regulation creates a binding framework for reviewing policy measures that may distort market access and strengthens the institutional basis for promoting a unified national market and improving the business environment. Based on this regulation, SAMR drafted Implementing Measures for the Regulation on Fair Competition Review which has been formal published in February 2025, to clarify the boundaries of rules, unify review standards and refine work requirements to strengthen institutional constraints.

- Enforcement Overview and Trends

In 2024, China’s antitrust enforcement remained focused on sectors closely tied to public welfare, such as healthcare, energy, and transportation. The SAMR maintained firm oversight in these areas while expanding its regulatory toolkit to enhance compliance monitoring and risk prevention.

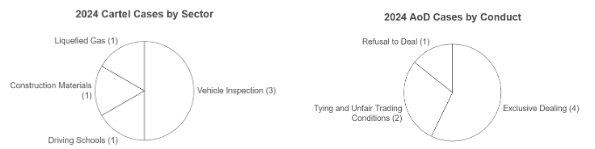

Seventeen new investigations into monopoly agreements were initiated during the year, with six cases concluded. These cases spanned sectors such as vehicle inspection, driving schools, construction materials, and liquefied gas, and primarily involved classic forms of horizontal coordination, including price fixing, output restriction, and market allocation. In parallel, five abuse of dominance cases were concluded, involving conduct such as exclusive dealing, tying, the imposition of unfair trading conditions, and refusal to deal, with total fines reaching RMB 106.9 million (approximately USD 15 million). SAMR also continued post-investigation oversight of key platforms, such as Alibaba,

Meituan, and CNKI, confirming the completion of Alibaba’s three-year remedial obligations.

Beyond formal enforcement, SAMR further institutionalized the use of “soft law” tools in 2024. Through compliance reminder letters, administrative interviews, and sector-specific training, the agency promoted early intervention and risk prevention. For instance, SAMR issued a letter to Avanci addressing potential antitrust concerns in its SEP licensing model. In the automotive sector, companies including Volkswagen, BMW, and Mercedes-Benz received warnings regarding possible resale price maintenance practices, including restrictions on dealer pricing and promotions. The authority also conducted training programs in high-risk sectors such as gas and pharmaceuticals to help businesses strengthen antitrust risk controls.

- Merger Control Review and Enforcement

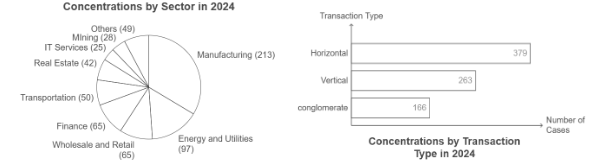

In 2024, China’s merger control regime saw notable developments in filing volume, review efficiency, and enforcement focus. SAMR received 729 merger filings and formally accepted 643 cases, of which 623 were cleared unconditionally and one was approved with remedies. No transactions were prohibited.

Domestic-to-domestic transactions accounted for around 57% of all filings. Manufacturing remained the most active sector (34%), followed by energy and utilities, wholesale and

retail, finance, transportation, real estate, IT services, and mining. Horizontally structured deals made up 61% of filings, and vertical mergers accounted for 42%, with conglomerate transactions also representing a significant portion.

Procedurally, the amended notification thresholds and documentation requirements resulted in a 15% year-on-year decrease in filings and helped to ease regulatory burdens for businesses. The simplified procedure applied to 91% of accepted cases, with the average review period for simplified cases reduced to 24.7 days—most concluded within the 30-day preliminary phase.

Substantively, SAMR continued to focus on sectors with high public interest or natural monopoly characteristics. Four transactions triggered competitive concerns, one of which—JX Nippon Mining & Metals’ acquisition of TANAKA—was conditionally approved. SAMR also maintained close scrutiny of deals below the notification threshold but with potential competitive implications. Two such cases in the high-tech sector were investigated, one of which was abandoned and the other later formally notified.

Three cases involving failure to notify were penalized under the 2022 revised Anti-Monopoly Law, with fines totaling RMB 6.15 million. SAMR also strengthened its post-clearance monitoring of remedy compliance—most notably launching a probe into NVIDIA’s acquisition of Mellanox for potential non-compliance with conditional approval terms.

Notably, 2024 saw China’s first-ever court case challenging a merger decision: Beijing Tobishi Pharmaceutical Co. v. SAMR. The court clarified several key issues: companies may only challenge merger decisions if their legitimate interests are materially affected; SAMR may impose remedies even in voluntarily notified transactions; and merger review aims to address competition concerns—not to prevent transactions outright. The ruling offers an initial judicial reference point for merger control disputes.

- Sectoral Competition Assessments

In recent years, SAMR has increasingly included market assessments of key industries in its annual antitrust enforcement reports. These assessments provide insights into sector-specific competition concerns and inform regulatory resource allocation. Past reports have covered sectors such as platform economy, oil and gas, online gaming, third-party payment, express delivery, and liquid dairy products.

The 2024 Report continues this trend with in-depth evaluations of six priority sectors: cultural entertainment ticketing, semiconductor materials, cloud services, warehousing, new energy vehicle (NEV) charging and battery swapping, and patent database services.

- Practical Takeaways

Antitrust enforcement in China became increasingly institutionalized in 2024, with a consistent focus on well-established priorities such as price-fixing, exclusive dealing, tying, and refusal to deal—particularly in sectors related to public welfare. Procedurally, improvements were made in review efficiency and regulatory transparency.

Core compliance areas remain unchanged: horizontal and vertical restraints, abuse of dominance, and merger filing obligations. SAMR has become increasingly alert to transactions below the notification thresholds that may still pose competition concerns, encouraging companies to assess not only formal filing criteria but also the substantive competitive impact of their transactions.

Meanwhile, SAMR continues to expand its use of non-punitive tools—such as warning letters, administrative interviews, and industry compliance training—to promote ex ante compliance. These soft-law measures reflect a regulatory shift toward proactive risk prevention and behavioral correction.

Importantly, the 2024 Report also reinforces SAMR’s ongoing commitment to sectoral competition assessments. Building on earlier efforts, this year’s report includes detailed evaluations of six high-profile industries: entertainment ticketing, semiconductor materials, cloud services, warehousing, NEV charging and swapping, and patent databases. Multinational firms should closely monitor whether their industry falls within SAMR’s focus and proactively assess potential risks and compliance strategies in anticipation of future scrutiny.