In startups and early-stage companies, founders often receive restricted equity grants as compensation for their services. With some planning, founders can potentially lower the taxes they pay on the appreciation of the equity by making a voluntary Section 83(b) election at the time the restricted equity award is issued. Crucially, a Section 83(b) election is expected to start the 5-year holding period for such newly issued restricted stock to qualify as Qualified Small Business Stock (QSBS), which opens the door to significant tax savings on an exit.

What is an 83(b) Election?

An 83(b) election permits employees and other service providers to elect to be taxed upon grant of restricted equity they receive as compensation for their services while it is still unvested instead of being taxed when the restricted equity becomes vested (which is the normal income tax timing rule absent an 83(b) election). An 83(b) election can only be filed within first 30 days after the issuance of the unvested restricted equity.

Why Would You Ever Choose to Pay Income Tax Sooner, Rather than Later?

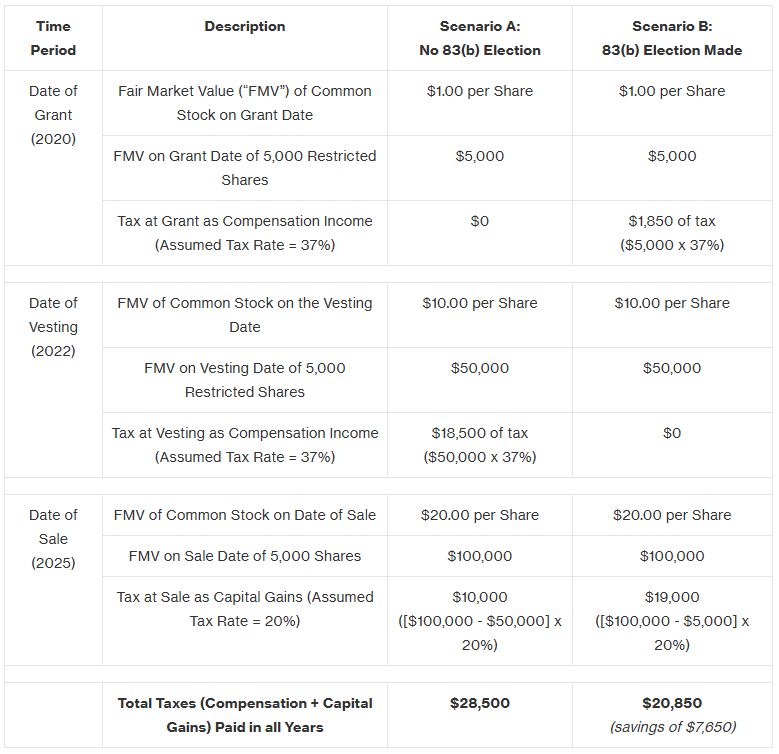

In a start-up or early-stage company where the value of the company’s stock often starts off low but has the potential for significant future appreciation, founders can potentially save taxes by making an 83(b) election. The example below provides a very simplified illustration of the potential federal income tax savings in a start-up formed in 2020 where a founder is initially granted 5,000 restricted shares that “cliff-vest” after 2 years (in 2022), and the value of the shares of this hypothetical start-up increases each subsequent year until the company is sold after the 5th anniversary of grant (in 2025). A different income tax calculation would apply if the founder paid a purchase price for the restricted shares.

In the example above, the founder would save $7,650 in federal taxes by making an 83(b) election on the restricted share grant. If the stock is QSBS, there would be even greater tax savings since there would be no tax at all upon sale if the 83(b) election had been made.

Are There Any Significant Downsides to Making an 83(b) Election?

If the restricted shares are forfeited (for example, because the employee quits before the vesting date) or the shares decrease in value, the employee may be limited in their ability to recoup the taxes already paid when the 83(b) election was made (i.e., $1,850 in the example above) because the employee may not be able to deduct a loss to net out those previously paid income taxes. Thus, if significant income taxes will need to be paid upon making an 83(b) election, an unusual situation if a founder receives unvested stock for services when the company is first founded, the founder may want to think twice about the risks of prepaying taxes.

What is New for 83(b) Elections?

The Internal Revenue Service (the “IRS”) recently released IRS Form 15620, an IRS-approved form that employees and other service providers may (but are not required to) use to make an 83(b) election. The new IRS Form 15620 largely follows prior IRS guidance on the content of an 83(b) election form, but the new form requires additional information about the company (or person) for whom the services were performed (including name, tax ID number, and address). Currently, IRS Form 15620 is optional, and founders can continue to use their own self-prepared forms (often provided by their accountant or company counsel) to make an 83(b) election.

The Upshot: If you receive a grant (or anticipate a grant) of restricted equity in exchange for services, talk to your accountant or lawyer about whether you should pay taxes on your equity award at the time of grant by filing an 83(b) election. The filing must be made within 30 days after the grant date. Don't miss the deadline or you may end up paying more taxes in the future, especially if the stock is QSBS and the 5-year holding period would otherwise be met.