Read our latest insights into the U.S. private equity market. We cover monthly deal activity and size, fundraising, exits, leveraged loans, and a look ahead.

Key Takeaways

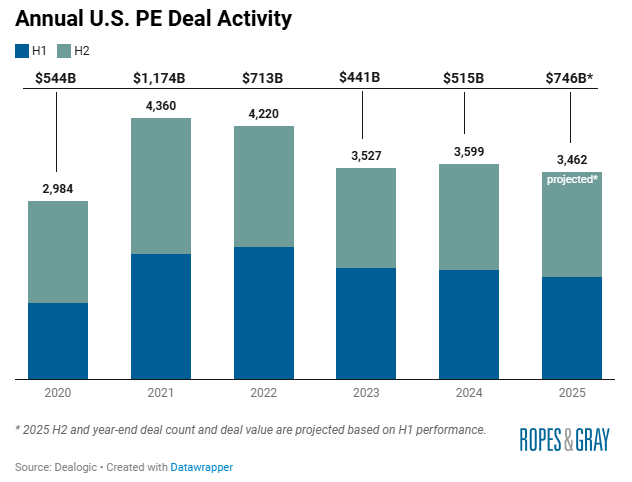

- Deal activity: The number of U.S. private equity deals didn’t rebound in H1 2025, but deal value was up 50% compared to the first half of 2024.

- Exits: U.S. PE exit value increased compared to both the first and second halves of 2024, driven by sales to strategic buyers.

- Fundraising: The share of PE fundraising as a percentage of overall U.S. private capital raised fell in H1 2025. While overall PE fundraising was down compared to H1 2024, the amount of growth equity capital raised increased.

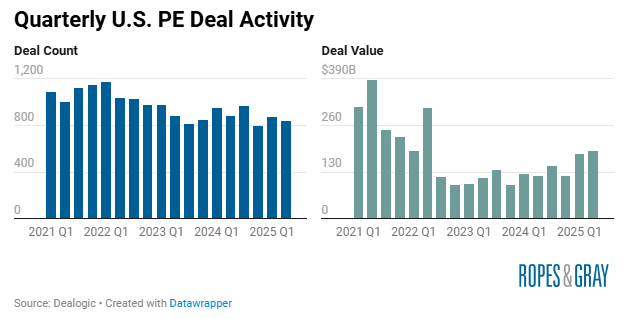

U.S. PE Deal Activity

- Deal Count: For the period ending June 30, 2025, the number of U.S. PE deals are down slightly on both a quarterly and half-year basis compared to both last period (QoQ and HoH) and last year (YoY).

- Deal Value: Despite deal counts being down, U.S. PE deal values continued to grow in the first half of the year. H1 2025 saw deal value jump 38% compared to H2 2024 and 50% compared to H1 2024.

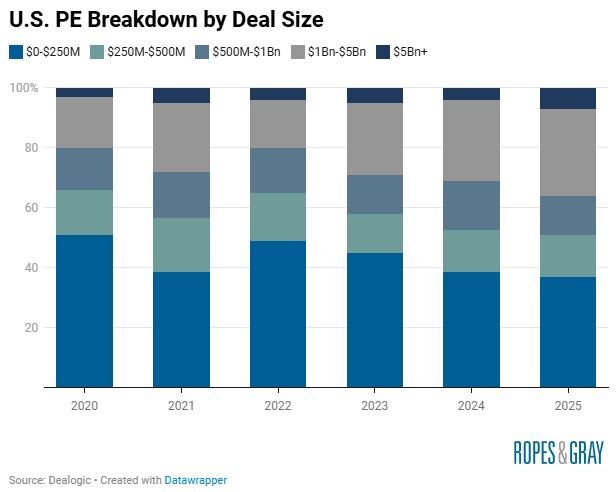

- Larger Deals: In H1 2025, the number of $1Bn+ deals increased by 35% compared to H1 2024. 37% of deals with disclosed values are now $1Bn+, up from just 20% in 2020.

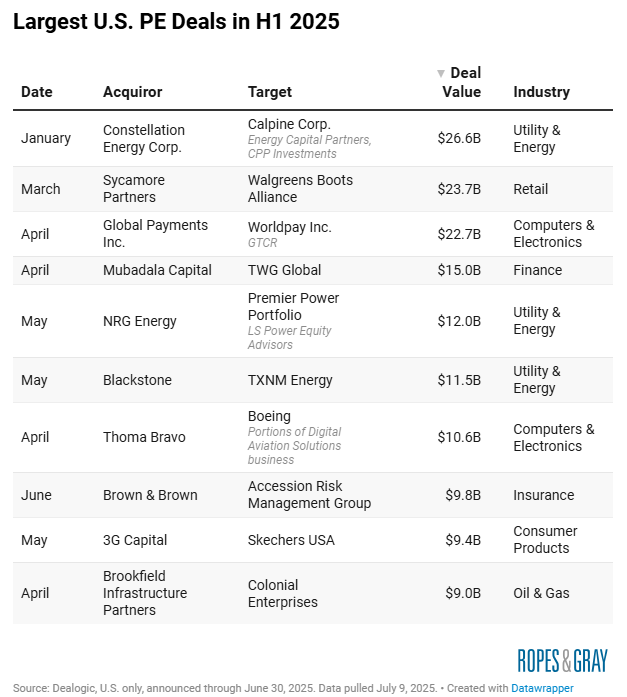

- Top 10 deals by value: Energy deals made up four of the top 10 deals by size in H1 2025. Five of the 10 largest deals were exits and three were take-privates.

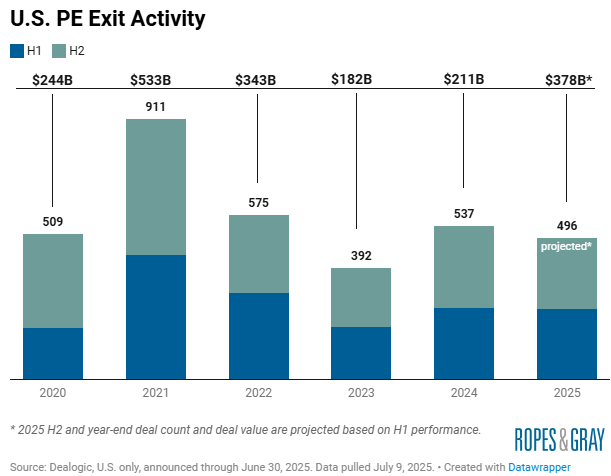

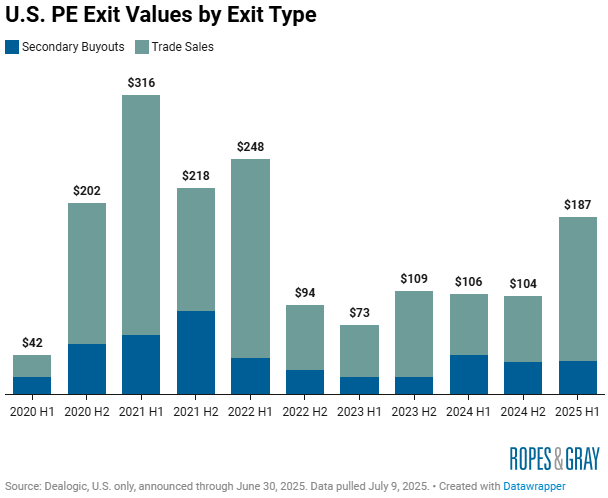

Exits

- Exit activity: After starting to pick up in 2024, the number of U.S. PE exits dropped in H1 2025, down 14% compared to H2 2024. On a more positive note, exit values are up dramatically compared to both H1 and H2 2024.

- Exit type: The jump in exit value is primarily driven by sales to strategic buyers, with trade sales up over 100% compared to both H1 and H2 2024.

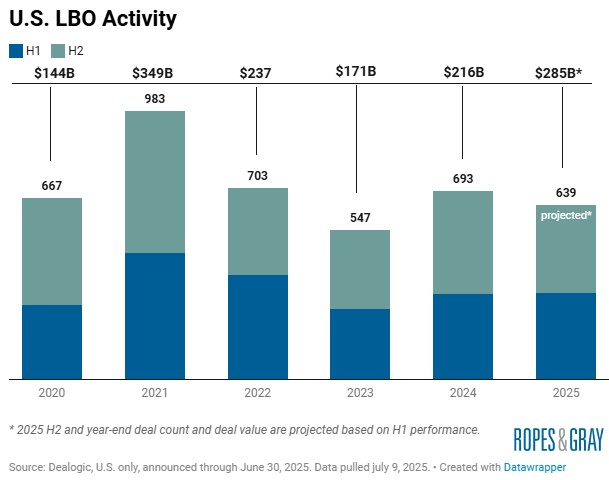

LBOs

- LBO activity: After increasing for the third consecutive period in H2 2024, the number of U.S. LBO deals dropped in H1 2025 by 16%.

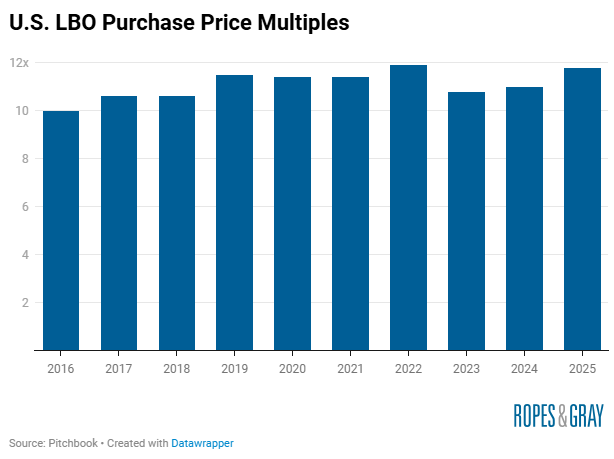

- Purchase price multiples: H1 2025 saw EV/EBITDA multiples for U.S. LBO jump by 0.8x from 2024, returning to 2022 levels.

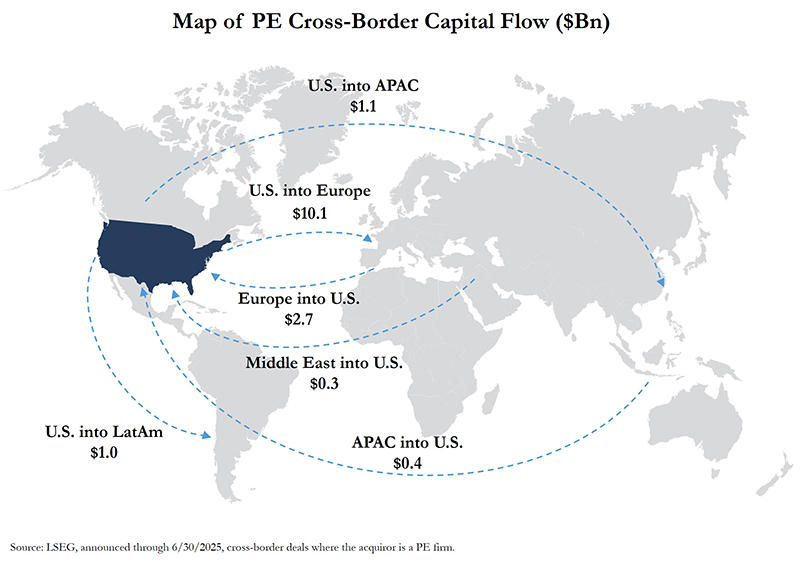

Cross-Border

- Outbounds: Overall U.S. PE cross-border outbounds hit $13.7Bn in H1 2025, up 24% from H1 2024. However, this level of investment is 40% below the 5-year average.

- To Europe: Europe has historically attracted the largest amount of U.S. PE cross-border capital. In H1 2025, U.S. investment into Europe represented ~75% of total U.S. outbounds and was up compared to both H1 and H2 2024.

- Inbounds: Total PE cross-border U.S. inbounds were $3.5Bn in H1 2025, down 38% from H1 2024 and 47% below the 5-year average.

- From Europe: In H1 2025, European PE investments into U.S. companies were down 51% compared to H1 2024 and 18% below the 5-year average.

Industry Breakdown

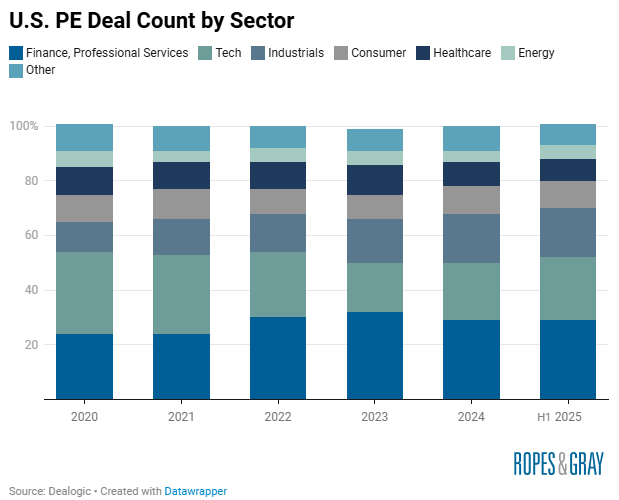

- Deal count by industry: The breakdown of U.S. PE deal count by sector is similar to 2024, with financial and professional services, tech, and industrials making up the largest number of deals.

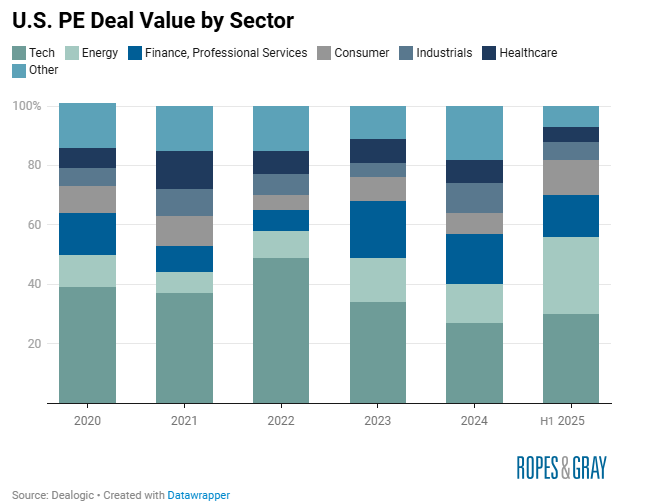

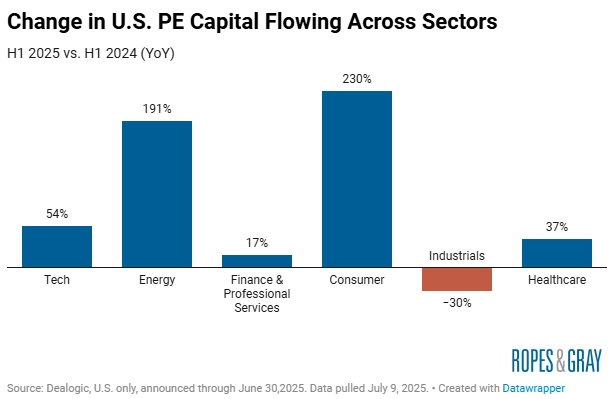

- Deal value by industry: H1 2025 has seen a shake up from historical averages in deal value breakdown. Specifically, deal values for the consumer and energy sectors have jumped and are respectively up 230% and 191% compared to H1 2024.

Fundraising Trends

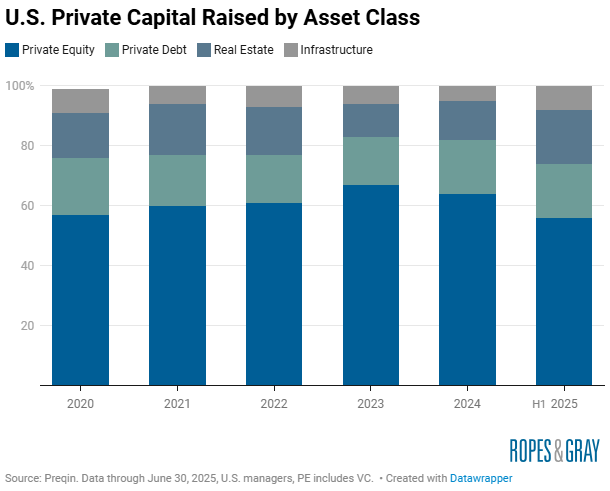

- Asset class breakdown: PE’s share of U.S. private capital raised dropped notably in H1 2025 to 56%, down from 64% in 2024. Fundraising for real assets (real estate and infrastructure) jumped to 26% of capital raised up from 19% last year.

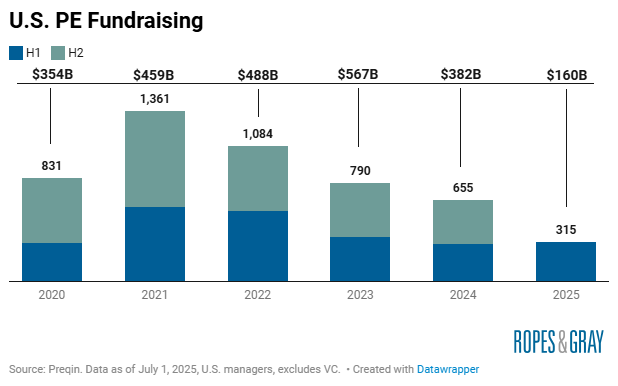

- PE fundraising: U.S. PE fundraising remained subdued in H1 2025, with the amount of capital raised down from last year.

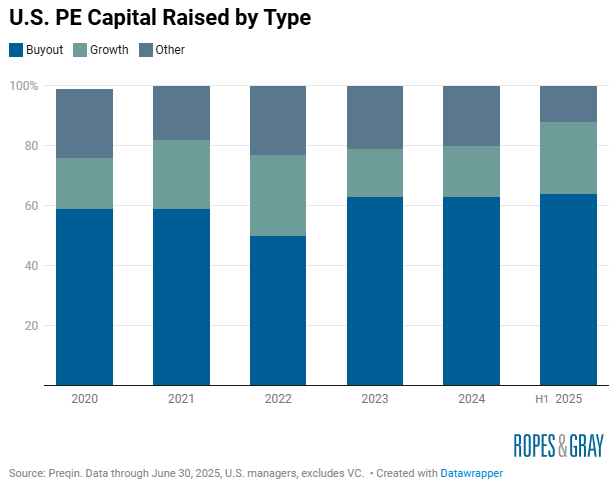

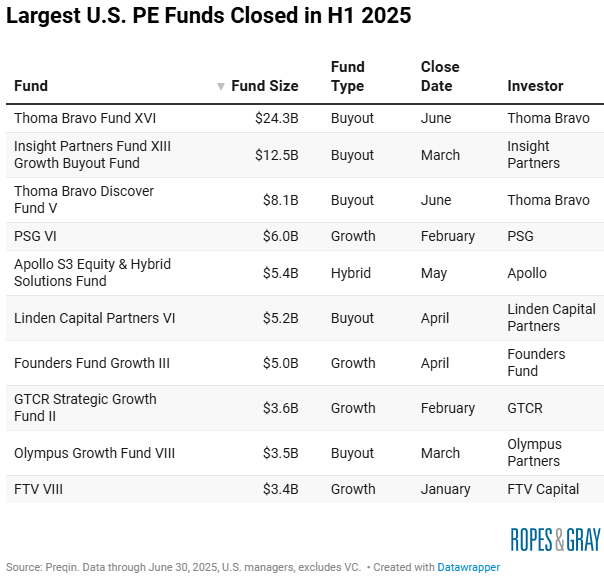

- PE fundraising breakdown: Growth funds made up an increasing proportion of U.S. PE fundraising, at 24% of capital raised in H1 2025. Five of the 10 largest U.S. PE funds closed in H1 2025 were buyout funds and four were growth funds.

- Largest fund: Thoma Bravo closed its 16th flagship fund at $24.3 billion, the largest PE fund closed in 2024 or 2025.

Private Wealth

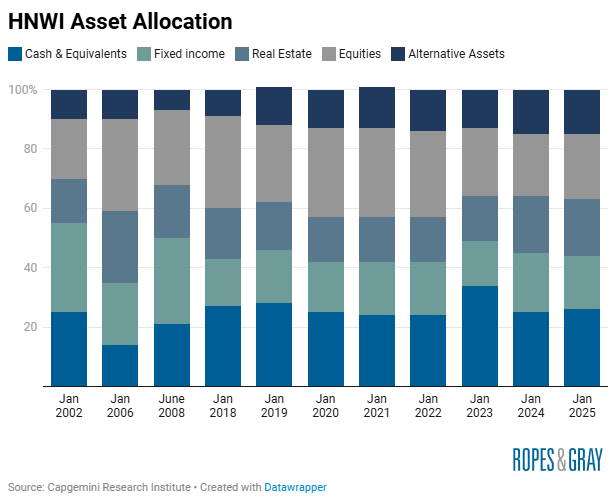

- Asset allocation: High net worth individuals (HNWI) have gradually increased their allocation to alternative assets over the last 20 years. As more wealth-focused offerings come to market, private equity has recently been gaining attention from private wealth investors.

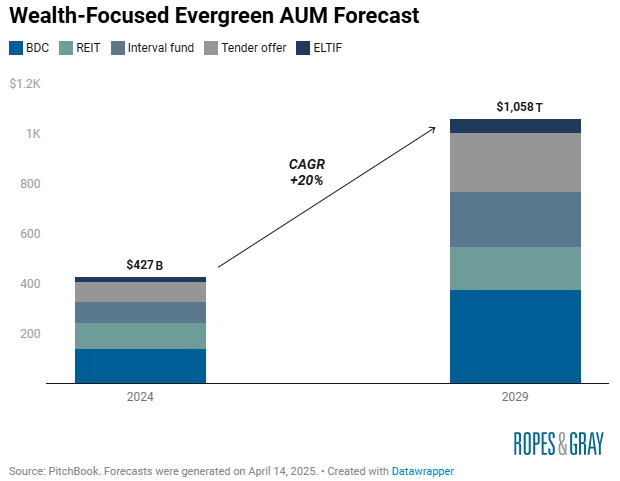

- Wealth-focused funds: PitchBook estimates wealth-focused evergreen funds have surpassed $400 billion in assets. Rapid growth is expected to continue, and assets could reach $1 trillion+ by 2029.

A Look Ahead

- Interest Rates: U.S. interest rate policy is in the spotlight with the White House pushing for lower rates and the Fed standing by its decision to hold out for increased clarity.

- Fed officials updated their projections to expect two rate cuts in 2025 following the June meeting. However, members of the Fed are split on the timing for rate cuts as opinions differ over the macroeconomic impact of current policies.

- The PE industry is waiting for lower rates to improve financing conditions and help to spur deal activity. According to a recent Preqin report, the potential upcoming rate cuts may lead to clearing in the market and mark the bottom of the current cycle.

- Expectations for dealmaking rebound: Some optimistic managers expect deal activity to rebound in H2 2025, while other managers look to 2026 and later.

- Despite a subdued transaction environment, investors have growing practice operating under heightened market volatility and continue to unlock opportunities.

- Long-term outlook: Private capital will be key to financing strategically important industries such as AI, energy, and infrastructure, leading to a favorable long-term outlook for private capital.

- With macro uncertainty rising and volatility likely to stay, these mega forces (AI adaption, energy transformation, and infrastructure investment), among others, may guide investment decisions and potentially drive returns.

- LMEs: In a PitchBook LCD U.S. Leveraged Finance Survey, 87% of respondents expect distressed liability management exercises to either maintain a similar pace or increase, up from 66% in Q1 2025.

- Fragmented global landscape: Current protectionist policies may create investment opportunities in onshoring initiatives.

- ECM activity: The 2nd half of Q2 saw a rebound in equity market sentiment. PE-backed IPOs are poised for an uptick as the exit channel opens.

- Over the last few days of June, three notable PE-backed companies filed for IPO: Accelerant (Altamont Capital), McGraw Hill (Platinum Equity), and NIQ Global Intelligence (Advent, KKR).