Last month, a startup’s Series A nearly fell apart when investors and founders realized their different calculation methods produced a $750,000 variance. The culprit was not deception or bad faith, but rather a complex interaction between pre-money and post-money instruments that neither side had fully modeled. When cap tables become unclear, it damages trust between founders and investors, potentially killing deals that would benefit everyone.

During a recent Zoom call, I watched both founders and their lead investor struggle to reconcile different understandings of how their various SAFEs and convertible notes would interact. Those “simple” agreements signed over the past three years had created a conversion puzzle that threatened to derail an otherwise promising investment.

For those unfamiliar with the term, SAFEs (Simple Agreements for Future Equity) are standardized documents created by Y Combinator that allow investors to provide capital in exchange for the right to receive equity when the company raises a future priced round. Unlike traditional equity investments, SAFEs do not immediately determine ownership percentages—that calculation happens later, which is where complexity often emerges.

This post focuses on Post-Money SAFEs with valuation caps, a common variant we see in practice. However, the complexity multiplies when companies mix different SAFE types (Discount-Only, MFN, or modified versions with custom terms), KISS agreements, and traditional convertible notes. Each instrument type has its own conversion mechanics, and their interactions can create exponentially more complex scenarios than what we explore here. The principles discussed apply broadly, but each cap table requires individual analysis.

This scenario plays out in my practice with increasing frequency. After three decades of advising both investors and founders, I have witnessed the remarkable evolution of startup financing: from the traditional preferred stock rounds of the 1990s, to the rise of convertible notes in the early 2000s, and now to the prevalence of SAFEs. For those new to startup financing: SAFEs and convertible notes are agreements where investors provide capital that later converts into equity, typically when the company raises a larger “priced round” like a Series A. The key difference between “Pre-Money” and “Post-Money” instruments lies in when they calculate the investor’s ownership: Pre-Money calculations look at the company’s value before including other convertible securities, while Post-Money ones factor in most other convertible securities first. This distinction can significantly impact all stakeholders’ ownership.

The democratization of startup financing has made standardized documents more accessible than ever, yet paradoxically, cap tables have become increasingly complex. Whether representing companies or investors, I have seen how poorly structured early instruments create problems for all stakeholders. This post examines one particularly thorny issue: the interaction between different convertible instruments and the often-overlooked impact of accruing interest on early notes.

The Math Matters: A Real-World Example

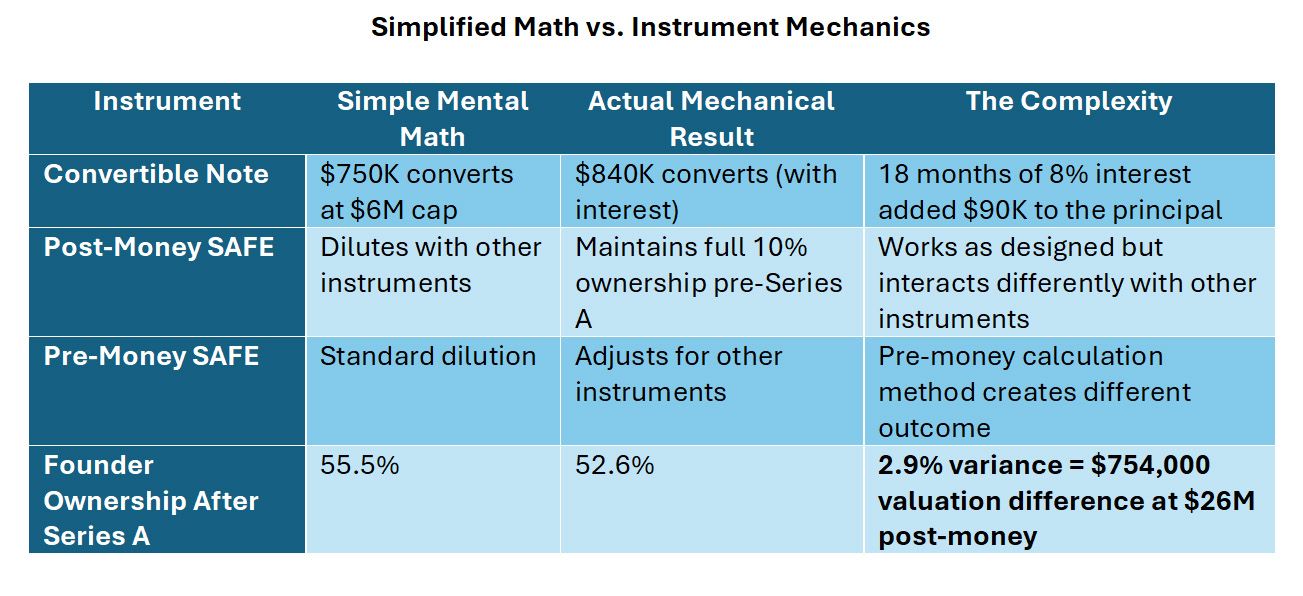

Consider a startup preparing for their Series A with the following convertible securities:

- A $500K Pre-Money SAFE with a $5M cap (from three years ago)

- A $1M Post-Money SAFE with a $10M cap (from two years ago)

- A $750K pre-money convertible note with a $6M cap and 8% interest (from 18 months ago)

The company was negotiating a $6M Series A at a $20M pre-money valuation.

The Post-Money SAFE functioned exactly as designed, maintaining the investor’s 10% ownership prior to the Series A. This is the intended feature of Y Combinator’s Post-Money SAFE: providing clarity on ownership percentage. This protection applies only until the priced round, at which point all converting securities dilute proportionally. However, when mixed with pre-money instruments, this creates a conversion sequence that many parties do not anticipate during initial negotiations.

Investors also suffer when these issues surface late. Deals fall apart, due diligence extends, and portfolio companies become distracted from growth rather than focusing on building value.

(For detailed calculations showing step-by-step math and ownership visualizations, see Annex A.)

Evolving Beyond Standard Templates

Y Combinator created the Post-Money SAFE to solve a real problem: Pre-Money SAFEs made it difficult for investors to understand exactly what percentage of a company they were buying. The Post-Money SAFE provides this clarity effectively. The complexity arises not from any single instrument, but from how different instrument types interact when they convert simultaneously.

While standardized forms serve an important role in reducing transaction costs and speeding up deals, these templates provide starting points for negotiation rather than immutable terms. When modifications are appropriate, they should align all stakeholders’ interests.

The Post-Money SAFE’s design creates an interesting dynamic: each Post-Money SAFE holder’s percentage is protected from dilution by subsequent convertible instruments issued before the priced round. This means that if a company raises multiple rounds of Post-Money SAFEs, the dilution from each new round falls entirely on common stockholders (typically founders and employees) and any pre-money instrument holders. Early Post-Money SAFE investors essentially receive anti-dilution protection that was not a feature of traditional convertible notes or Pre-Money SAFEs.

For example, if a company raises three rounds of Post-Money SAFEs over 18 months, each successive round dilutes the founders but not the earlier Post-Money SAFE holders. By the time of the priced round, founders may find their ownership significantly lower than they anticipated when they agreed to the first Post-Money SAFE. This concentration of dilution on common stockholders has not gone unnoticed in the market.

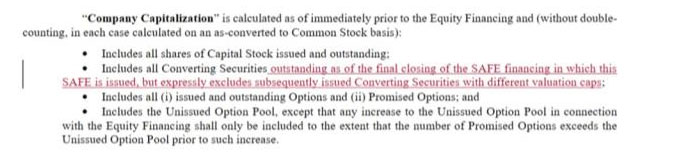

One modification that has gained traction in the market addresses the dilution concentration issue: adjust the “Company Capitalization” definition to include all Converting Securities outstanding as of the final closing of the SAFE financing round, while excluding Converting Securities issued in subsequent financing rounds. This approach, which I believe was first articulated by Silicon Hills Lawyer in their 2021 analysis of Post-Money SAFE mechanics (though others may have proposed similar solutions), aims to distribute dilution more evenly across stakeholders rather than concentrating it on common stockholders and later investors. The specific language modification (as proposed by Silicon Hills Lawyer and detailed in Annex B) requires precise changes to just a few words. Having seen variations of this fix implemented in actual transactions, sometimes with additional language to reinforce the concept, it appears to help create more balanced outcomes while preserving the Post-Money SAFE’s core benefit of ownership clarity, though the effectiveness can vary depending on the specific mix of instruments and other deal terms.

Red Flags: Common Sources of Conversion Complexity

Key indicators of conversion complexity include:

1. Template and Structure Issues

- Mixed templates or vintages on the same cap table. Pre- vs. post-money SAFEs, notes, side letters, or non-YC variants create reconciliation challenges. Key terms like Company Capitalization and conversion triggers often differ between templates—confirm definitions and conversion sequence before modeling.

- Side letters or bespoke clauses. MFN, pro-rata, or custom conversion triggers can override standard template terms and create unexpected interactions.

2. Time and Interest Accumulation

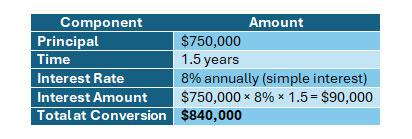

- Notes outstanding long enough for interest to be material. Even simple interest at 8% adds $90,000 to a $750K note after 18 months. Confirm whether interest compounds and model the actual conversion amount, not just principal.

3. Multiple Rounds and Caps

- Multiple convertible rounds or large aggregate pre-priced raises. Layering instruments over time (e.g., $3M+ across multiple SAFEs) increases cross-effects at conversion.

- Different valuation caps or discounts across instruments. Creates varying conversion prices—a $5M cap vs. $10M cap means 2x difference in shares received for the same investment.

4. Option Pool Complexity

- Option pool increases tied to the priced round. Post-money SAFEs exclude pool expansions from their denominator, pushing this dilution entirely onto common stockholders. Watch for Promised Options exceeding the existing pool.

5. Modeling Gaps

- No multi-scenario modeling across valuation ranges. If conversions are not modeled at multiple price points (both with and without pool increases), variations of millions in equity value can hide in the gaps.

Critical Questions for All Parties

- Do all stakeholders understand the exact order in which instruments will convert?

- Has anyone calculated the impact of accrued interest on all convertible notes?

- Do all parties share the same understanding of how post-money and pre-money instruments interact?

If the answer to any of these questions is “no,” the cap table likely contains complexities that necessitate comprehensive conversion analysis.

Beyond Standard SAFEs: When Complexity Compounds

While this analysis focuses on capped SAFEs, most cap tables we review contain additional wrinkles:

- Discount-Only SAFEs that interact unpredictably with capped instruments at different valuations.

- MFN (Most Favored Nation) SAFEs that automatically inherit better terms, creating cascading recalculations.

- Modified SAFEs with custom terms like participation rights, board seats, or non-standard conversion triggers.

- KISS agreements and other alternative instruments that follow entirely different conversion logic.

Each variation changes the math. A single MFN provision can trigger a complete recalculation of your cap table. Custom modifications often conflict with each other in ways that only surface during conversion. The modeling complexity grows geometrically, not linearly, with each instrument type added.

Strategic Considerations for Sustainable Deals

Given these layers of complexity, all parties should follow these key practices:

- Model Multiple Scenarios Together: Both companies and investors benefit from transparent conversion modeling at various valuations. What appears reasonable at one valuation may yield different results at another.

- Understand Instrument Interactions: Pre-Money and Post-Money instruments follow fundamentally different conversion mechanics. When combined on the same cap table, their interaction affects all stakeholders in ways that require careful analysis.

- Account for Time Value: Convertible notes accrue interest continuously. All parties should model how time affects ultimate conversion amounts.

- Maintain Alignment: Focus on creating sustainable incentive alignment. The startup ecosystem thrives on reputation and relationships. Structures that surprise either party can damage both.

Cap Table Management Platforms: Useful Tools with Limitations

Modern cap table management platforms like Carta have made it easier to track and visualize ownership. These platforms excel at modeling standard conversion scenarios but may not fully capture the nuanced interactions between mixed Pre-Money and Post-Money instruments, especially when dealing with bespoke terms or side letters.

Template libraries and automated document generators, while valuable for standardization, can oversimplify complex financing decisions. Users may select seemingly appropriate templates without fully understanding how different instruments will interact in their specific situation.

Additionally, these platforms require significant time investment to use properly. What looks like a simple interface often masks layers of complexity in how different financing instruments are modeled. Companies benefit from delegating this technical work to qualified team members or consultants, allowing leadership to focus on growth and investor relations.

When used properly, these platforms provide value: maintaining accurate ownership records, facilitating information sharing, and helping identify potential issues. While these platforms excel at standard scenarios, complex situations involving bespoke terms or mixed instrument types may require additional manual verification.

Looking Ahead

These strategic considerations become even more critical as the market evolves. Many companies now spend two years or more in the SAFE and convertible note stage, often completing multiple rounds before their first priced equity round. While software startups might close a few million in these early raises, capital-intensive sectors such as life sciences can raise many times that amount—making the complexity of mixed instruments a common challenge across industries. Multiple instruments with different terms over extended periods are becoming the norm, not the exception.

This evolution does not mean the ecosystem should avoid these instruments. SAFEs and convertible notes remain valuable tools that enable efficient early-stage fundraising. The key is ensuring all parties understand how their chosen instruments will interact at conversion.

Clear documentation and transparent modeling today prevent surprises that can damage relationships and destroy value tomorrow. In early-stage financing, the difference between smooth conversions and contentious negotiations often comes down to ensuring all stakeholders share the same understanding of their agreements.

The word “simple” in SAFE should not create complacency. These instruments deserve careful attention from all parties to ensure alignment and preserve the trust that makes great companies possible.

The Value of Experience

The complexity outlined above is why experienced counsel matters. A few hours of modeling and careful drafting today can prevent millions in disputed equity value tomorrow.

Many firms can provide standard templates. The value lies in understanding how different instruments interact, spotting issues before they compound, and knowing which modifications actually work in practice. This is particularly critical when mixing pre-money and post-money instruments, managing accrued interest, or navigating side letters that override standard terms.

Early structural decisions create lasting consequences. The right guidance helps both founders and investors achieve their goals while preserving the trust essential to long-term success.

Annex A: Detailed Cap Table Calculations

Starting Parameters and Key Assumptions

- 36 months ago: $500K Pre-Money SAFE @ $5M cap

Assumptions: standard pre-money mechanics; no discount; no special side letters

- 24 months ago: $1M Post-Money SAFE @ $10M cap

Assumptions: YC-style post-money mechanics; “Company Capitalization” excludes any future option-pool increase adopted for the priced round; no discount; no side letters

- 18 months ago: $750K Pre-Money Note @ $6M cap, 8% interest (non-compounding)

Assumptions: simple (non-compounding) interest; no discount; no MFN; no prepayment

- Now: $6M Series A @ $20M pre-money (i.e., $26M post-money)

Assumptions: no new option-pool increase; no pro-rata side letters; no other convertible instruments beyond those listed above

1. Convertible Note Interest Calculation

2. Simple Mental Math (What Parties Often Calculate Informally)

Many parties perform quick mental calculations without fully considering instrument mechanics:

Quick Ownership Estimates:

- Pre-Money SAFE: $500K ÷ $5M = 10%

- Post-Money SAFE: $1M ÷ $10M = 10%

- Convertible Note (principal only): $750K ÷ $6M = 12.5%

Informal Post-Series A Expectation: Assuming simple proportional dilution through all rounds:

- New Series A Investors: 23.1% ($6M ÷ $26M)

- Founders: ~55.5%

- Early investors: Proportionally sharing remaining ~21.4%

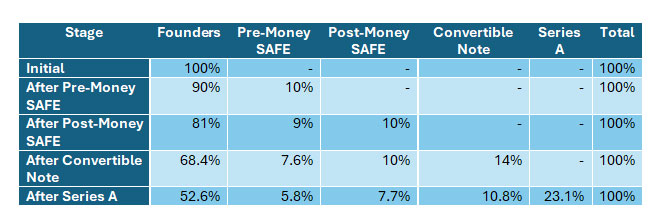

3. Actual Mechanical Calculation: Ownership Evolution

Ownership Waterfall Table

Detailed Step-by-Step Calculations:

Step 1: Pre-Money SAFE Conversion

- Initial allocation: $500K ÷ $5M = 10%

- Founders retain: 90%

- Pre-Money SAFE receives: 10%

Step 2: Post-Money SAFE Conversion

- Post-Money SAFE calculates ownership as: $1M ÷ $10M = 10%

- This 10% is protected from dilution by subsequent convertibles

- Existing holders dilute proportionally:

- Founders: 90% × 0.9 = 81%

- Pre-Money SAFE: 10% × 0.9 = 9%

- Post-Money SAFE: 10% (protected)

Step 3: Pre-Money Convertible Note Conversion

- Note converts at: $840K ÷ $6M = 14%

- Post-Money SAFE maintains 10% (per its terms)

- The 14% comes from the remaining 90%:

- Available for allocation: 76%

- Founders’ share: 76% × (81/90) = 68.4%

- Pre-Money SAFE’s share: 76% × (9/90) = 7.6%

Step 4: Series A Investment

- Series A: $6M at $20M pre-money = 23.1% ownership

- All existing holders dilute proportionally by 76.9%:

- Series A takes 23.1%

- All others multiply their holdings by 0.769

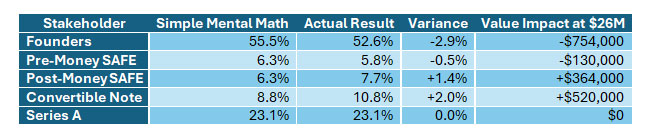

4. Variance Analysis

Comparison: Simple Mental Math vs. Actual Mechanics

5. Key Factors Creating Variance

1. Post-Money SAFE Mechanics: The instrument maintains its percentage through subsequent convertible securities (though not through the priced round), affecting how other instruments dilute.

2. Accrued Interest Impact: The $90,000 in accrued interest increased the Note’s conversion amount by 12%, amplifying its dilution effect.

3. Interaction Effects: The combination of post-money protection and accrued interest creates compound effects not immediately apparent in simple calculations.

Financial Impact: At the $26M post-money valuation, the 2.9% variance in founder ownership represents approximately $754,000 in value difference between calculation methods.

6. Observations for All Stakeholders

- Conversion mechanics matter: Different instrument types interact in complex ways that require careful modeling.

- Time affects value: Accrued interest on notes becomes material over extended periods.

- Transparency benefits everyone: Clear understanding of these mechanics helps all parties set appropriate expectations and avoid surprises that could damage relationships or kill deals.

- Align on an auditable model: Agree on assumptions and one shared, checkable conversion model so the math is not relitigated mid-deal.

Annex B: Post-Money SAFE Modification: Rebalancing Dilution Allocation

Note: This modification approach was proposed by Silicon Hills Lawyer in their 2021 analysis of Post-Money SAFE mechanics. Some practitioners implement variations or additional language to reinforce these concepts, and effectiveness may vary depending on the specific mix of instruments and other deal terms.

Purpose of Modification

The modification aims to distribute dilution more evenly across stakeholders rather than concentrating it entirely on common stockholders when subsequent SAFEs are issued. This helps prevent situations where founders bear disproportionate dilution from multiple rounds of Post-Money SAFEs.

Key Modification to Section 2

The primary change involves the definition of “Company Capitalization”:

Additional Required Change

You must delete the standard language on the first page that states: “This Safe is one of the forms available at http://ycombinator.com/documents and the Company and the Investor agree that neither one has modified the form, except to fill in blanks and bracketed terms.”

This deletion is necessary because you are modifying the standard form beyond simply filling in blanks.

Effect of Modification

This modification means that:

1. SAFEs issued in the same round will share dilution proportionally among themselves.

2. Subsequently issued SAFEs will have dilution capacity available rather than pushing all dilution onto common stockholders.

3. The allocation of dilution becomes more balanced across stakeholder groups

Note that this modification does not reduce the mathematical complexity of conversion calculations, it simply redistributes how dilution is allocated among different parties.

Implementation Considerations

- Legal Review Required: Any modification to standard documents should be reviewed by qualified legal counsel.

- Investor Communication: All parties should understand how the modification affects conversion calculations.

- Consistency: If using this modification, apply it consistently across all SAFEs in the same financing round.

- Documentation: Clearly document the modification in closing documents and cap table notes.

Alternative Approaches

Some practitioners implement additional or alternative modifications, including:

- Adding explicit language about pro-rata treatment within rounds.

- Creating side letters addressing specific conversion scenarios,

- Using entirely different instruments for complex situations.

The appropriate approach depends on the specific transaction dynamics and the mix of instruments on the cap table.